Open Credit Enablement Network (OCEN), a digital infrastructure initiative by the government of India aimed at democratizing the small-ticket credit market. This aligns with the government’s focus on financial inclusion. In simple terms, Open Credit Enablement Network Market Potential facilitates the provision of small loans to small businesses through a collaborative network. This network consists of front-end apps engaged in digital commerce with extensive outreach and lenders with the capacity to disburse loans but lacking sufficient reach.

By leveraging OCEN, lenders can now reduce their effort and customer acquisition costs, which previously hindered them from serving businesses with low-ticket cash flow requirements. Could you explain the purpose behind OCEN and the projected timeline for its rollout

The purpose behind OCEN and Projected timeline for its rollout

Let’s address the problem that OCEN aims to solve. Manual loan processing incurs costs due to the involvement of personnel. By transitioning to digital processes, these costs can be reduced significantly. Furthermore, digital operations allow loans to be processed remotely, reaching areas where lenders may not have a physical presence. This accessibility empowers underserved individuals to access small-ticket loans, which would otherwise be challenging. The underlying motive behind OCEN is to build it as a public digital good, minimizing friction and costs associated with private sector alternatives. Ultimately, this makes small loans more affordable for consumers.

Regarding the rollout, we have followed a similar approach to other public digital goods, such as UPI (Unified Payments Interface). For example, the government built the BHIM app on the UPI infrastructure to demonstrate the possibilities of seamless, frictionless money transfers using just a phone number and a debit card PIN. Once the infrastructure was established, reference implementations were created to showcase its usage. In the initial phase of OCEN, we have developed a pilot program in collaboration with the Government e-Marketplace. This platform enables government organizations to procure goods from small traders, such as micro, small, and medium enterprises (MSMEs) with annual turnovers ranging from 10 to 15 lakhs.

More prosperous than even salaried individuals, we have achieved a significant milestone. MSMES face a common challenge when they secure purchase orders—they often buy with cash but sell on credit. Consequently, a liquidity gap arises, and this is where credit can provide a solution. Recognizing this, we decided to step in and offer loans to address the issue.

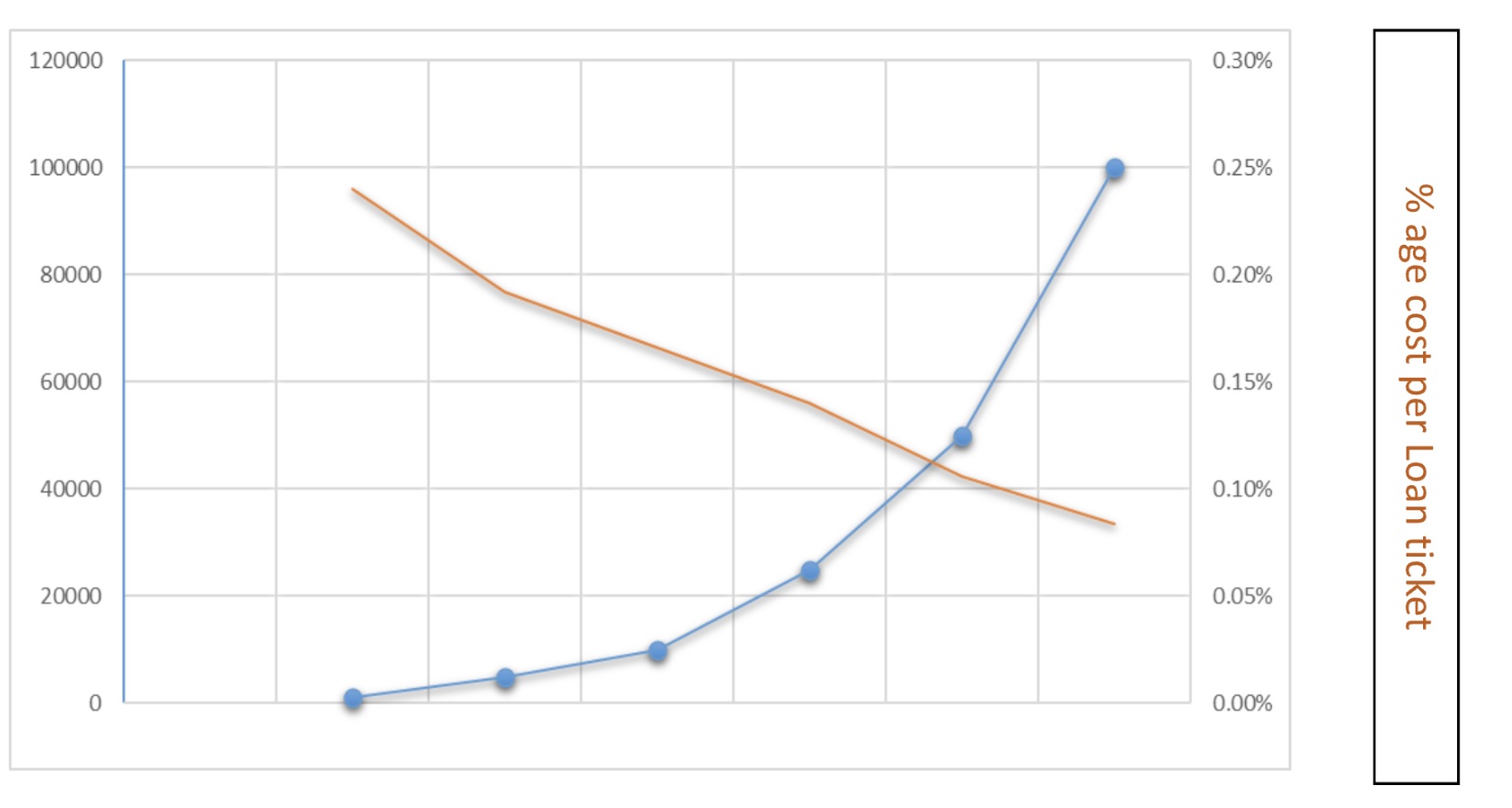

Although the scale of our endeavor makes it a challenging journey, we have successfully launched our loan services. To date, we have provided over three and a half thousand loans, amounting to a total of 13.8 crores. What makes us particularly proud is that our loans start as small as 160 rupees, while the largest loan reaches up to 10 lakhs. Our average loan size is 40,000, catering to a segment that would otherwise be overlooked by traditional lenders. This diverse range, from 160 rupees to 10 lakhs, demonstrates the broad scope of our coverage.

One crucial observation is that our efforts align with the vision of On DC, which aims to foster collaboration between lenders and apps. It emphasizes the importance of various participants coming together to establish a robust network. Now, Kotak Mantra Bank, being one of the largest banks in the country, has been an early adopter of our platform.

Open Credit Enablement Network Market Potential

Often, many people try to join a party when it’s already crowded. However, we recognized the opportunity to participate early and gain a deep understanding of how this evolving network operates. When venturing into a new business, comprehending its underlying dynamics becomes crucial. Unlike traditional businesses that relied on balance sheets or financials, the credit decision model in this context is distinct. It revolves around the data derived from invoices supplied by small businesses or sole proprietors on the government marketplace.

In many ways, this still represents a relatively smaller and unique credit landscape, characterized by lower ticket sizes and shorter tenures. Thus, we seized the chance to become one of the first banks to lend on an open platform. This allowed us to explore new business rules and establish real-time credit approval parameters, enabling the seamless disbursement of loans directly on the platform. Our initial rollout on the open platform has been successful in accomplishing all these objectives.

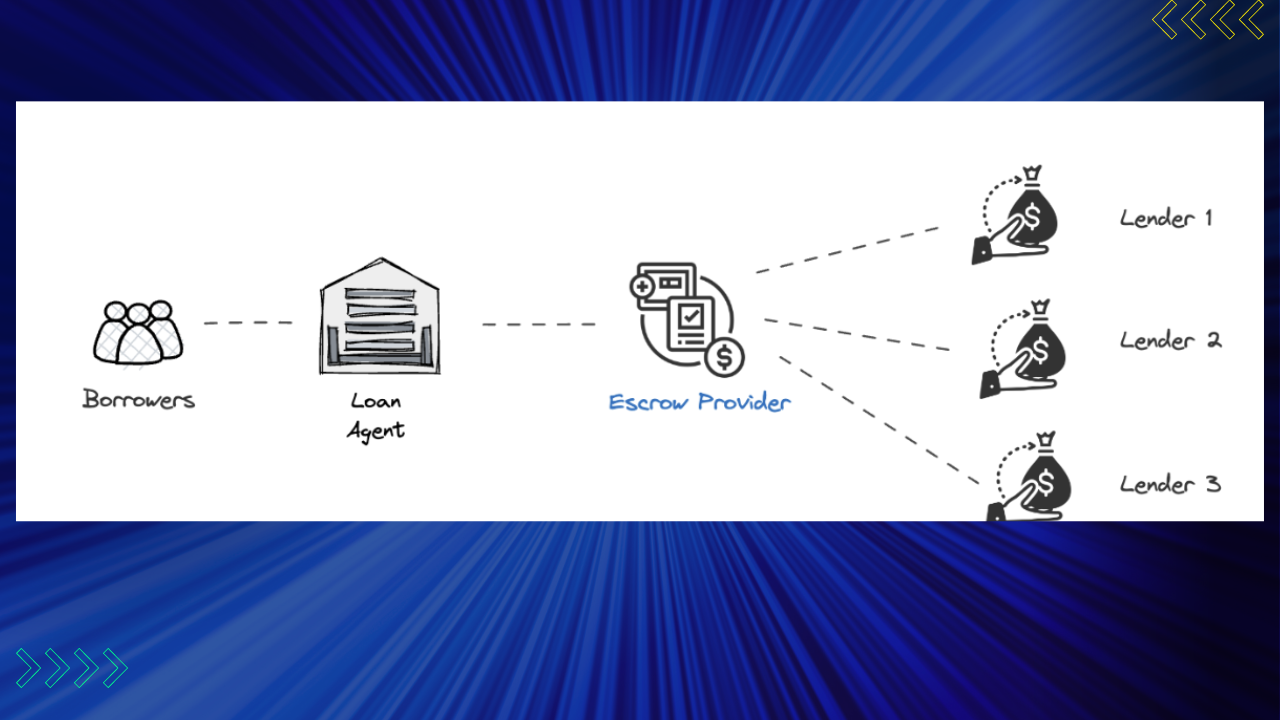

You can access GST invoice data, bank statement data, and credit bureau data through the account aggregator, which was launched in September last year. These four sets of data, all in digital format, can be instantly utilized to assess creditworthiness. Based on this evaluation, an offer is generated, including the interest rate and loan amount, which is then presented to the user for selection. Subsequently, the user proceeds with the Know Your Customer (KYC) process, which can be conveniently completed using Aadhaar and registration certificates.

After providing the dispersal account and signing the agreement, which can also be done using Aadhaar, the loan is disbursed within minutes. This streamlined process ensures that the money is deposited into the user’s account within 10 minutes, a significant improvement compared to the usual timeframe of a few days to two weeks for SMEs seeking loans of similar size. This rapid disbursement is a remarkable leapfrog in the industry.

The objective now is to scale this process and increase the number of transactions facilitated through the network. However, when it comes to assessing creditworthiness, banks traditionally emphasize asset quality, which takes time. Overcoming this challenge, our approach focuses on cash flow analysis based on the platform’s data. Through a government marketplace, small sellers can upload their invoices and borrow against them, leveraging the expected payments from buyers or suppliers within a defined period. We have implemented a set of rules that will continue to be refined, aiming to lower thresholds and enhance accessibility over time.

Initially, we offered this service exclusively to existing bank customers who had already undergone KYC procedures. However, in the coming weeks, we plan to extend it to non-customers as well. This means we will be able to onboard new customers in real-time while simultaneously making credit decisions about them. By compressing these processes, we are building a novel business model that combines real-time credit assessment and customer onboarding seamlessly.

It is crucial to ensure the successful onboarding of multiple lenders onto the platform. Kotak Mahindra Bank is already onboard, along with seven other lenders. The front-end apps play a vital role in showcasing the enthusiasm and support for this initiative. The onboarding process is progressing well, and we are witnessing a high level of enthusiasm among various players to join the network.

We are proceeding cautiously with great deliberation regarding the subject matter. When undertaking a project of this magnitude, it is crucial to ensure precision and accuracy. Our focus extends far beyond a single quarter; instead, we are envisioning a span of 15 years. Presently, there are two aspects at hand. Firstly, there is a significant level of interest on the front end, although we have only integrated Gem at this point. Additionally, we are in the process of developing a second application called SID B GST PSI, specifically designed for invoice financing.

We have already garnered interest for various use cases, such as receipt financing for milk, agricultural trade financing, and even purchasing buffaloes for dairy farming. These are cases that previously would not have received financial backing. However, it is important to note that these cases differ from lender onboarding, which involves adhering to KYC guidelines mandated by the RBI. The onboarding process is distinct, and a decision regarding onboarding and the front-end applications will be made within the next four to five months, once we are adequately prepared.

OCEN onboarding and KYC process in detail.

Our primary focus has been on the onboarding process through digital commerce applications. This aspect holds great significance since lenders are ready to disburse funds. The level of interest in these digital applications is substantial, with over 70 companies expressing their intent to go live. Although I cannot disclose the names of these companies, they include prominent players in the industry. Pay

ment apps, e-commerce sites, and platforms catering to cooperatives managing dairy sales and processing are just a few examples. The range of use cases is extensive, covering various sectors. The intriguing aspect is understanding what drives their interest and what they hope to achieve. This presents a more intricate response.

Currently, the RBI’s digital lending guidelines state that lenders are charged when they onboard lending service providers. However, this model results in inflation of lending costs for end users. While this approach may continue, we are contemplating engaging with the RBI to explore an alternative model.

Currently, the lender’s agent charges the borrower, following the SEBI’s model for mutual funds, where both models can be followed based on the consumer’s preference. The aim is to provide choice for the consumer. The front-end app’s revenue generation can stem from the lender or the borrower, although charging the borrower is presently not allowed by the guidelines.

However, this is subject to change and formal establishment. Regardless of the model, deeper considerations must be made regarding commissions for lead generation and business partners. It would be wise to consult Deepak regarding this collaboration, the potential impact on cost of acquisition, and the viability of a volume-driven approach.

OCEN will Redefine the Lending Ecosystem

The lending ecosystem is akin to the existing payment ecosystem. Just as payment solutions are integrated at the point of checkout, enabling credit availability and facilitating payments in retail and online environments, we are witnessing a similar shift on the merchandise supply side. Suppliers now have the ability to access credit for their transactions, and this transformation will revolutionize lending practices. There are two prominent factors driving this transformation in the short term.

Firstly, GST invoice-based financing has the potential for significant adoption due to the large volume of monthly transactions in the country. As we establish the necessary infrastructure, more consumers will come on board. Secondly, numerous e-commerce companies and B2B suppliers have started incorporating cash flow-based lending within their ecosystems. As lenders become more comfortable with this lending model, they are extending it beyond the confines of the current system. The market will ultimately determine the appropriate value and associated price for these services. Some ecosystem players, including loan service providers, may offer financing as part of their embedded value proposition

There is a need for stronger relationship-building with vendor partners in order to generate more revenue. How can we utilize this line of credit to facilitate additional transactions and business activities? Currently, its potential is not fully realized. Allow me to provide you with some anecdotal evidence. We used to engage with gem sellers, guiding them through our app to identify any obstacles they encountered. As they started using the app, some of them inquired about our future plans. The credit availability is limited to a specific segment, resulting in a scarcity of credit for these sellers. Our aim is to unlock credit opportunities for them. Now, let’s address the question of why front-end apps perform this function.

OCEN in e-commerce company

By providing liquidity to businesses, we can enhance the overall gross merchandise value on our platform. This aligns with our intentions for gem as well. Additionally, this approach leads to higher valuations for these companies. Credit has always been a crucial driver of any developed economy. However, we have noticed that while our top 100 million corporations are served, the remaining billion are neglected. Therefore, our focus is on building solutions for the billion, without diverting attention to the top 100 million customers. It is a challenging journey with numerous obstacles, but we are committed to facilitating credit access. Once borrowers establish their creditworthiness and successfully repay their initial small loans, they can gain access to larger loans, which further stimulates business growth. Ultimately, we hope that this will contribute to the country’s economic development.

Credit Culture to develop and penetrate the underserved market

We believe that many individuals today need a way to establish their credibility. Traditionally, creditworthiness was determined solely through credit bureaus. However, our platform offers a different dimension, allowing borrowers to demonstrate their credibility by borrowing for a short-term, defined purpose, with clear visibility on what they are borrowing against and how they will repay it. In my view, the foundation for building a comprehensive ecosystem lies in real-time underwriting, easy collection processes, and complete transaction transparency. Once these building blocks are established, customers with a good credit history will be ready to access larger and longer-term credit options.