In the world of lending, the historical focus has been mainly on higher-ticket and longer-tenure loans. OCEN Lending with Small Ticket Short Tenure Loans, The conventional loan processing approach encompassed a plethora of manual checks, validations, verifications, and operational procedures, which significantly impacted the cost of originating each loan. This situation naturally inclined lenders towards higher ticket and longer tenure loans, as these choices justified portfolio profitability.

Embracing Change: Small Ticket and Short Tenure Loans

Conversely, small ticket and short tenure loans faced challenges due to their higher origination costs. Consequently, lenders refrained from actively developing such portfolios. In cases where they did opt for this approach, they often imposed exorbitant interest rates and fees on borrowers to balance the portfolio’s profitability equation.

Nano-entrepreneurs typically require credit ranging from INR 5,000 to 1,00,000 to address various business needs. Such credit is often sought for inventory replenishment, managing cash flow tied up in receivables, business expansion, and procuring machinery or equipment. The demand for credit in these scenarios is often sudden and urgent, necessitating capital infusion within a mere day or two. The scarcity of formal credit sources for this audience is rooted in the complexities of underwriting such loans and the disproportionately high operational costs associated with servicing these small loan amounts.

Innovating through OCEN 4.0 for Short-Term Lending

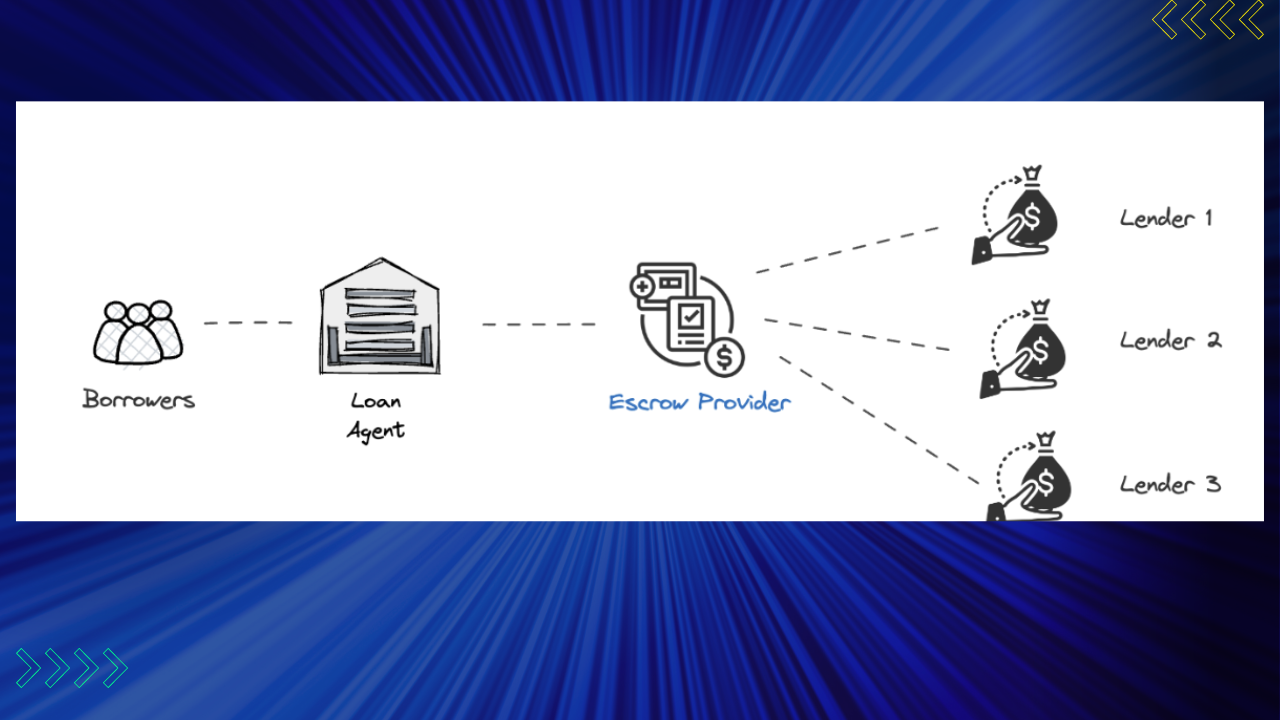

OCEN 4.0 emerges as a solution to this challenge, benefiting all stakeholders in the lending ecosystem—Borrower agents, Lenders, Loan agents, and most importantly, end-borrowers. This innovative approach leverages digital public infrastructure to minimize the costs associated with processing small ticket short tenure loans on a large scale. Let’s examine a comparison between a traditional long-tenure loan (36 months) and a sachet loan (3 months) to illustrate the concept:

Traditional Business Loan

- Loan Amount: 10,00,000

- Tenure (months): 36

- Processing Cost per loan: 100

- %age of Loan ticket size: 0.01%

Sachet Loans (Small Ticket / Short Tenure)

- Loan Amount: 25,000

- Tenure (months): 3

- Processing Cost per loan: 100

- %age of Loan ticket size: 0.40%

While the per loan processing cost for small ticket short tenure loans is significantly higher as a percentage of the loan ticket size, this challenge is effectively addressed when operating at scale.

Enhancing Revenue with Small Ticket Loans

Examining revenue potential further reinforces the viability of small ticket loans. Let’s explore another comparison:

Traditional Business Loan

- Loan Amount: 10,00,000

- Tenure (months): 36

- Net Interest Margin: 5%

- Processing Fees: 2%

- Net Interest Income: 78,952

- Fee Income: 20,000

- Total Revenue per Loan: 98,952

- Portfolio Size: 10,00,00,000

- No of Loans: 100

- Portfolio Revenue of Loans: 98,95,200

- No of Loan cycles in 3 years: 1

- Net Total Revenue: 98,95,200

Sachet Loans (Small Ticket / Short Tenure)

- Loan Amount: 50,000

- Tenure (months): 3

- Net Interest Margin: 5%

- Processing Fees: 1%

- Net Interest Income: 417

- Fee Income: 500

- Total Revenue per Loan: 917

- Portfolio Size: 10,00,00,000

- No of Loans: 2000

- Portfolio Revenue of Loans: 18,34,000

- No of Loan cycles in 3 years: 12

- Net Total Revenue: 2,20,08,000

This analysis demonstrates that a lender can realize up to 2.2x higher revenue from a portfolio exposure of 10 Cr by providing small ticket short tenure loans to a larger group of borrowers. However, the obstacle of higher operational costs per loan presents a challenge to achieving such returns for a small ticket loan portfolio.

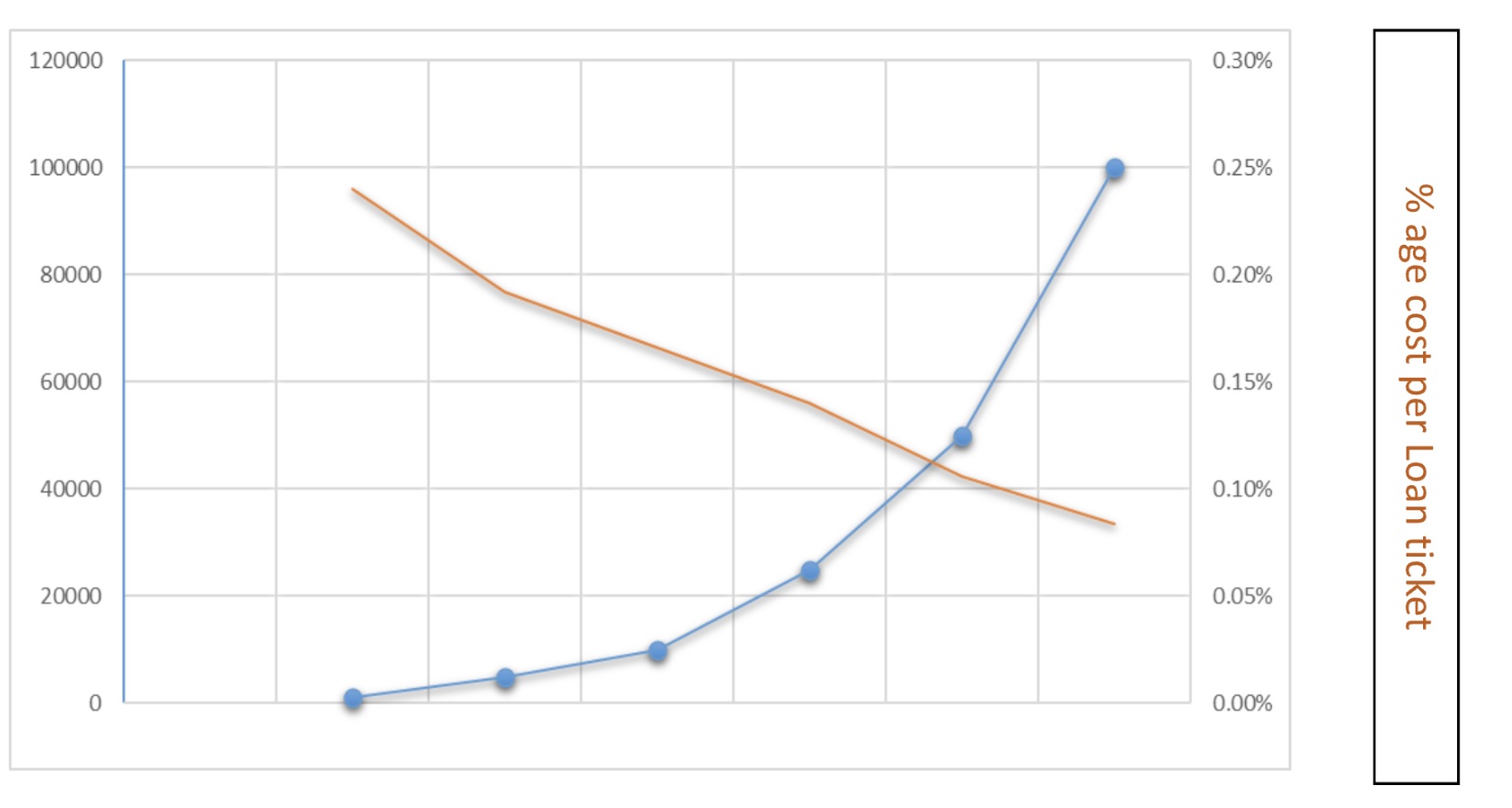

Overcoming Operational Costs for Scale

Processing small ticket loans digitally incurs operational costs that range between Rs. 50 to 100, depending on various participant services involved in the approval process. These costs have been decreasing over the past few years and are expected to continue declining as services become more efficient and standardized. As the scale increases, the per transaction cost across services naturally diminishes, as illustrated by the trendline chart.

Even when considering higher operational costs per loan, profitability for a small to mid-sized portfolio of 2000-20000 loans surpasses that of a big ticket loan portfolio. Returns of 2.1-2.20x can be achieved.

Unleashing Potential: Scaling Up for Profits

Interestingly, the operational costs decrease significantly at a larger scale, especially beyond 1,00,000+ loans, resulting in substantially higher profitability. This opens up a significant opportunity for lenders to establish lucrative loan portfolios.

Advantages Beyond Revenue

Small ticket short tenure loans earmarked for revenue-generating businesses have proven to exhibit superior performance in terms of timely repayment. The loan proceeds empower small business borrowers to boost their operations, leading to better repayment behavior. Due to the short tenure of these loans (up to 3 months) and amortizing principal recovery, the portfolio’s delinquency rates are anticipated to be lower. Unlike large ticket loans, the granularity of these loans minimizes the impact of any defaults, safeguarding the portfolio’s performance.

Furthermore, these loans offer better predictability owing to their short repayment tenures, aiding in building credit profiles for repeat lending. When tailored underwriting aligns with industry requirements, it mitigates delinquency risks and enhances profitability on a larger scale. This creates a unique opportunity to onboard new-to-credit MSME borrowers and offer diverse financial products and services.

The reusability of the same loan amount across multiple loan cycles empowers lenders to refine their underwriting and innovate on products tailored to borrowers’ specific needs. This positive feedback loop amplifies benefits for all participants, fostering a thriving lending ecosystem.