The Open Credit Enablement Network (OCEN) is revolutionizing the way credit is accessed and distributed. By leveraging modern technology and interoperable systems, 13 OCEN Use Cases aims to democratize credit and improve financial inclusion globally. This article explores the various use cases of OCEN and how they are transforming different sectors.

OCEN Use Case 1: Financial Inclusion

One of the key use cases of OCEN is its ability to promote financial inclusion. By leveraging OCEN, financial institutions and service providers can extend credit to underserved populations more efficiently. Traditional credit processes often involve lengthy paperwork and complex verification procedures, making it challenging for individuals with limited access to formal financial services. However, with OCEN, the credit application and approval processes can be streamlined, reducing barriers to credit for marginalized communities.

OCEN Use Case 2: Peer-to-Peer Lending

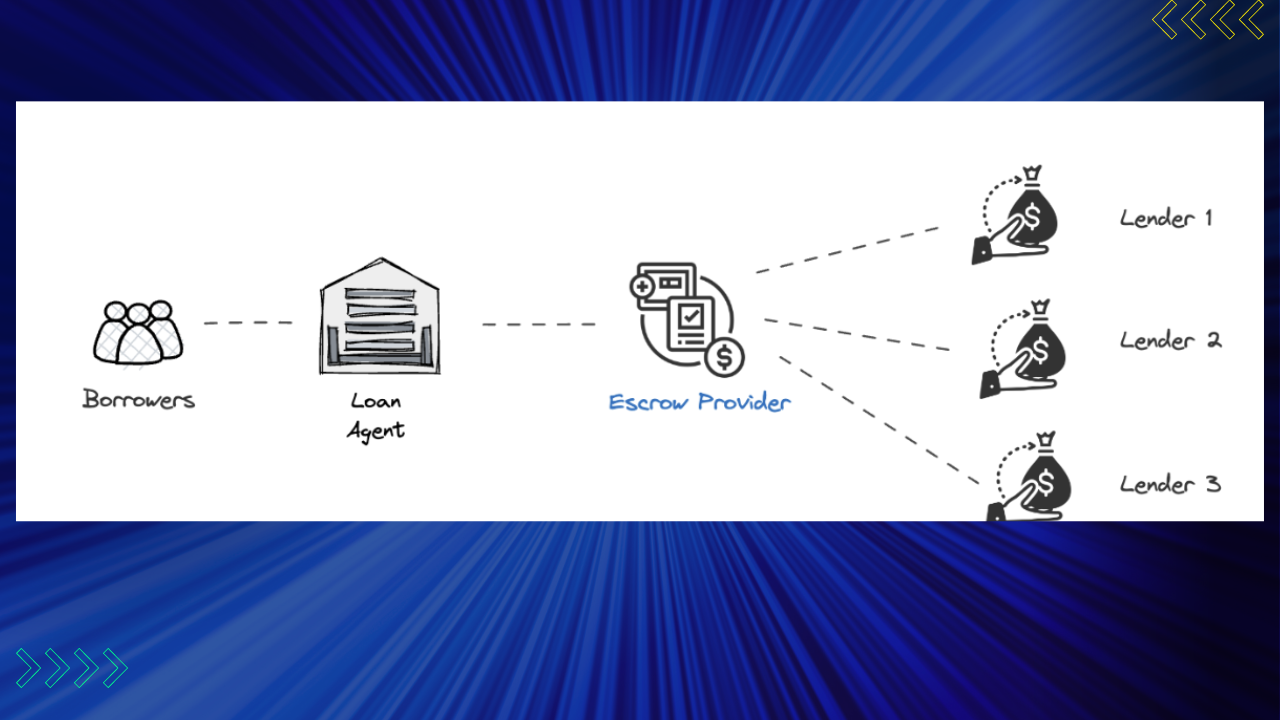

Another compelling use case of OCEN is its role in facilitating peer-to-peer lending. Traditionally, lending transactions have involved intermediaries such as banks or lending institutions. However, OCEN enables individuals to directly lend and borrow from each other without the need for intermediaries. This direct lending approach offers several benefits.

Firstly, it eliminates the need for intermediaries, resulting in lower costs for both lenders and borrowers. By cutting out middlemen, borrowers can access credit at more competitive interest rates, while lenders can earn higher returns on their investments. Additionally, OCEN enhances transparency in lending transactions, as all the relevant information is recorded on a decentralized network, providing a clear and trustworthy record of transactions.

OCEN Use Case 3: Microfinance

Microfinance plays a crucial role in providing access to financial services for small businesses and entrepreneurs in developing economies. OCEN can significantly enhance the efficiency and accessibility of microloans. By integrating OCEN into microfinance systems, the disbursement and repayment processes can be streamlined, reducing administrative burdens and transaction costs.

The use of OCEN in microfinance also enables financial institutions to leverage alternative data sources for credit assessments. In many cases, individuals and businesses lack formal credit histories, making it challenging for traditional credit scoring models to evaluate their creditworthiness. OCEN allows the inclusion of non-traditional data, such as transaction records and social network connections, enabling more accurate credit scoring and risk assessment for microloans.

OCEN Use Case 4: Cross-Border Remittances

Remittances from migrant workers to their families in their home countries are a vital source of income for many households. However, traditional cross-border remittance services often involve high fees and lengthy processing times. OCEN can revolutionize this space by enabling faster and more cost-effective remittance services.

Through OCEN, financial institutions and remittance providers can create interoperable networks that facilitate instant and low-cost transfers. Migrant workers can send money directly to their families’ accounts, bypassing multiple intermediaries and reducing transaction fees. This enhanced accessibility and affordability of cross-border remittances contribute to poverty reduction and economic empowerment for migrant communities.

OCEN Use Case 5: Supply Chain Financing

Supply chain financing is critical for maintaining the flow of goods and services in various industries. However, small and medium-sized enterprises (SMEs) often face challenges in accessing affordable credit to support their operations. OCEN can address these challenges by providing credit-enabled networks within supply chains.

By integrating OCEN into supply chain finance systems, businesses along the supply chain can access credit more efficiently. OCEN enables streamlined processes such as invoice factoring and trade finance, ensuring timely access to working capital. This, in turn, strengthens the overall resilience and efficiency of supply chains, benefiting businesses and driving economic growth.

OCEN Use Case 6: Decentralized Finance (DeFi)

Decentralized Finance, or DeFi, has emerged as an innovative and rapidly growing sector within the broader financial industry. OCEN can play a significant role in advancing the capabilities and interoperability of DeFi applications.

With OCEN, different DeFi platforms can seamlessly connect and share information, enabling the transfer of assets and data across various protocols. This interoperability unlocks new possibilities for DeFi, allowing users to access a broader range of financial services and applications. OCEN’s integration with DeFi also enhances the overall security, transparency, and efficiency of decentralized financial systems.

OCEN Use Case 7: Credit Scoring and Risk Assessment

Traditional credit scoring models heavily rely on limited data sources, such as credit histories and financial statements. This approach often excludes individuals and businesses with little or no formal credit records, hindering their access to credit. However, OCEN offers a solution by incorporating a wide range of data points for credit scoring and risk assessment.

By leveraging the data shared on the OCEN network, financial institutions can gather insights from various sources, such as transaction records, payment histories, and social connections. This comprehensive view allows for more accurate assessments of creditworthiness, enabling a broader population to access credit. OCEN’s inclusive credit scoring models promote financial inclusivity and provide opportunities for individuals and businesses that were previously underserved.

OCEN Use Case 8: Government Initiatives

Governments around the world are increasingly recognizing the potential of OCEN to enhance their financial inclusion initiatives and social welfare programs. By incorporating OCEN into government schemes, efficient and transparent credit distribution can be achieved.

OCEN enables governments to streamline the process of delivering financial aid, subsidies, and other social benefits to eligible individuals and businesses. By leveraging the network’s capabilities, governments can disburse funds directly to beneficiaries, reducing bureaucratic inefficiencies and eliminating middlemen. OCEN’s secure and auditable nature ensures transparency and accountability in the distribution of government-initiated credit programs, fostering social welfare and economic development.

OCEN Use Case 9: Small and Medium-sized Enterprises (SMEs)

Small and medium-sized enterprises (SMEs) form the backbone of many economies, but they often struggle to access the necessary funding to grow and expand their operations. OCEN presents a promising use case for supporting the growth of SMEs through credit enablement.

By leveraging OCEN, financial institutions and lenders can offer SMEs more accessible and tailored credit options. The streamlined credit processes and expanded data sources allow for quicker credit assessments, reducing the time SMEs need to wait for approvals. OCEN’s credit enablement empowers entrepreneurs, fosters innovation, and contributes to job creation and economic growth.

OCEN Use Case 10: Insurance and Underwriting

Insurance plays a crucial role in managing risk and providing financial protection. OCEN can revolutionize the insurance industry by enabling efficient underwriting processes and expanding insurance accessibility.

By integrating OCEN into insurance systems, underwriters can access a broader range of data points to assess risk. This includes information such as transaction records, credit history, and social connections. With a more comprehensive view of the insured party’s risk profile, insurers can offer more accurate and personalized coverage, potentially reducing premiums for individuals and businesses. OCEN’s integration with insurance and underwriting processes promotes efficiency, accuracy, and inclusivity within the insurance sector.

OCEN Use Case 11: Education Financing

Education is a fundamental pillar of personal and societal development, but the cost of education can be a significant barrier for many individuals. OCEN can play a vital role in making education more affordable and accessible through innovative financing options.

By utilizing OCEN-enabled credit, individuals can access affordable loans specifically designed for education-related expenses. This includes tuition fees, study materials, and other educational costs. OCEN’s efficient credit processes and inclusive credit scoring models ensure that deserving students can pursue their educational aspirations without excessive financial burdens. Education financing through OCEN promotes social mobility, empowers individuals, and contributes to the overall development of societies.

OCEN Use Case 12: Healthcare Financing

Access to quality healthcare is a fundamental right, but for many individuals, the cost of healthcare can be prohibitive. OCEN can facilitate healthcare financing and make healthcare services more affordable and accessible.

By integrating OCEN into healthcare financing systems, individuals can access credit options specifically tailored to cover medical expenses. This includes hospital bills, surgeries, medications, and other healthcare services. OCEN’s efficient credit processes and data integration allow for faster approval and disbursement of funds, ensuring timely access to healthcare.

Furthermore, OCEN enables the development of innovative healthcare financing models such as health insurance schemes and health savings accounts. By leveraging OCEN’s capabilities, insurers and healthcare providers can create more flexible and personalized coverage options, reducing the financial burden on individuals and improving overall healthcare outcomes.

OCEN Use Case 13: Real Estate Financing

Real estate investments, including home purchases and property development, often require substantial financial resources. OCEN can streamline real estate financing processes and make property ownership more attainable.

By integrating OCEN into real estate financing systems, potential homebuyers and property investors can access credit options that align with their needs. OCEN enables efficient mortgage lending, reducing the complexities and paperwork traditionally associated with property transactions. Additionally, OCEN facilitates transparent and secure property valuations and title verifications, minimizing the risks for both lenders and borrowers.

Real estate developers can also benefit from OCEN by accessing credit-enabled networks that streamline project financing. This promotes investment in infrastructure development, stimulates economic growth, and enhances the availability of affordable housing options.

Conclusion

The Open Credit Enablement Network (OCEN) holds tremendous potential to revolutionize various sectors and promote financial inclusion. From empowering underserved populations with access to credit to facilitating peer-to-peer lending and transforming traditional financial services, OCEN’s use cases are vast and diverse.

By leveraging OCEN’s capabilities, financial institutions, governments, and service providers can streamline processes, enhance transparency, and make financial services more affordable and accessible. The integration of OCEN into sectors such as microfinance, cross-border remittances, supply chain financing, and healthcare and education financing unlocks new opportunities for individuals, businesses, and economies at large.

As OCEN continues to evolve and gain traction, its impact on the global financial landscape is expected to be significant. The democratization of credit and the expansion of financial services can drive economic growth, reduce inequality, and improve the lives of millions worldwide.

How does OCEN ensure transparency in lending transactions?

OCEN records all relevant information on a decentralized network, providing a transparent and immutable record of lending transactions. This enhances trust and accountability among lenders and borrowers.

Can OCEN be integrated with existing financial systems?

Yes, OCEN is designed to be interoperable with various financial systems, making integration with existing infrastructure seamless and efficient.

How does OCEN benefit small businesses and entrepreneurs?

OCEN’s credit enablement capabilities provide SMEs and entrepreneurs with easier access to capital, supporting their growth and expansion efforts. This fosters entrepreneurship and contributes to economic development.