Discover how the Open Credit Enablement Network (OCEN) is transforming India’s financial ecosystem, its benefits, implementation challenges, and its potential to empower millions. Explore this comprehensive guide to OCEN and its impact on financial inclusion in India. Visit Prove’s blog for more insights: India’s Open Credit Enablement Network (OCEN).

Introduction

The financial landscape in India is undergoing a remarkable transformation with the introduction of the Open Credit Enablement Network (OCEN). As India strives for financial inclusion and digital empowerment, OCEN emerges as a game-changing initiative that has the potential to revolutionize the way credit is accessed and utilized. In this article, we will delve deep into the intricacies of OCEN, its benefits, challenges, and the impact it can have on the lives of millions of Indians.

Understanding the Open Credit Enablement Network (OCEN)

The Open Credit Enablement Network (OCEN) is a groundbreaking framework designed to facilitate the seamless flow of credit across various financial institutions in India. This initiative aims to connect lenders, borrowers, and digital platforms, enabling efficient and transparent access to credit for individuals and small businesses. By leveraging technology and standardized APIs (Application Programming Interfaces), OCEN aims to simplify and streamline the lending process, thereby empowering millions with financial inclusion.

The Key Components of OCEN

OCEN comprises three fundamental components that work in tandem to achieve its objectives:

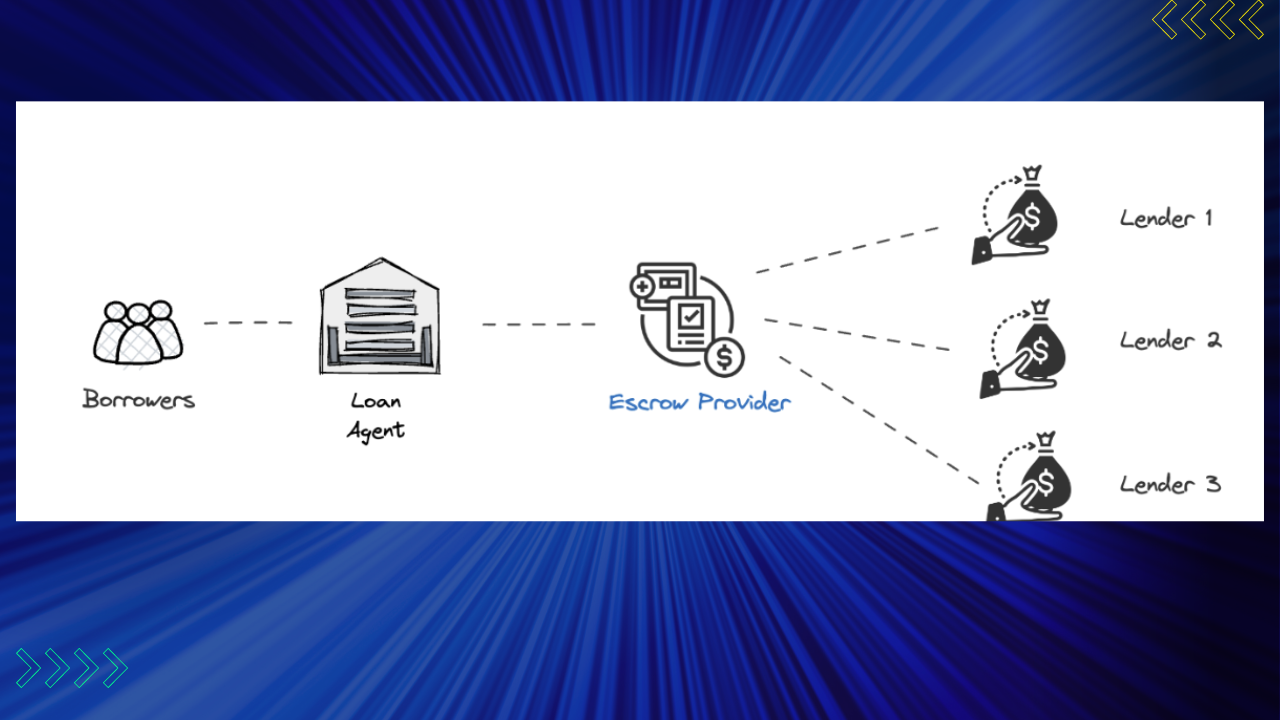

- Data Providers: These are organizations that possess data related to borrowers’ credit history, income, and financial behavior. They act as a critical source of information for lenders to assess the creditworthiness of potential borrowers.

- Digital Lenders: These entities leverage the OCEN framework to access credit-related data from Data Providers and use it to evaluate loan applications. Digital Lenders provide a seamless borrowing experience through digital platforms, simplifying and expediting the lending process.

- Digital Ecosystem Enablers: These are digital platforms and aggregators that enable the integration of Data Providers and Digital Lenders. They play a pivotal role in ensuring the smooth exchange of data and transactions between the two entities.

Implementing OCEN: Challenges and Opportunities

While OCEN presents immense potential, its implementation comes with its fair share of challenges and opportunities. Let’s explore some of the key factors that shape the success and effectiveness of OCEN in India.

Regulatory Framework and Data Privacy

One of the primary challenges in implementing OCEN is establishing a robust regulatory framework to ensure data privacy and security. Given the sensitive nature of financial information, it is crucial to create a system that safeguards borrower data while allowing seamless data exchange between lenders and data providers.

Integration and Standardization

The successful implementation of OCEN depends on the integration and standardization of APIs across various stakeholders. Establishing a common set of APIs ensures interoperability, streamlines data exchange, and reduces friction in the lending process.

Technology Infrastructure

Building a robust technology infrastructure that supports OCEN’s objectives is critical. This includes scalable and secure platforms, reliable data storage systems, and advanced analytics capabilities to process vast amounts of financial data in real-time.

Stakeholder Collaboration and Adoption

To maximize the potential of OCEN, collaboration among all stakeholders is essential. Governments, financial institutions, and technology providers need to work together to create an ecosystem that encourages adoption and fosters innovation.

Digital Literacy and Accessibility

While OCEN has the power to revolutionize lending, it is crucial to address the digital literacy gap and ensure accessibility for

all individuals, including those in remote areas or with limited internet connectivity. Promoting digital literacy and providing access to digital platforms are vital steps in enabling widespread adoption and benefiting the underserved populations.

The Impact of OCEN on Financial Inclusion

The Open Credit Enablement Network has the potential to drive significant impact on financial inclusion in India. Let’s explore some of the key ways OCEN can empower individuals and small businesses:

Access to Formal Credit

OCEN breaks down barriers and provides easier access to formal credit for individuals and small businesses that were previously excluded from traditional lending systems. By leveraging alternative data sources and digital platforms, OCEN enables lenders to assess creditworthiness more accurately, expanding the pool of eligible borrowers.

Reduced Dependence on Informal Sector

In India, the informal sector has long been a primary source of credit for individuals and small businesses. However, such informal arrangements often come with high interest rates and limited consumer protections. OCEN’s formal credit ecosystem offers an alternative, empowering borrowers to access affordable credit from regulated lenders, reducing their reliance on informal channels.

Enhanced Transparency and Accountability

OCEN introduces a transparent and accountable lending process by leveraging standardized data and APIs. This transparency reduces the information asymmetry between lenders and borrowers, enabling fairer credit decisions and reducing the chances of fraud or malpractice.

Accelerated Loan Disbursement

With OCEN, loan disbursal processes can be streamlined and expedited, leveraging digital platforms and automated workflows. This acceleration in loan disbursal not only benefits borrowers by providing timely access to funds but also enables lenders to efficiently manage their loan portfolios and improve liquidity.

Boost to Entrepreneurship and Small Businesses

Small businesses are the backbone of India’s economy, and access to credit plays a crucial role in their growth and sustainability. OCEN’s streamlined lending process and increased credit availability provide a significant boost to entrepreneurship and small businesses, enabling them to expand operations, invest in new opportunities, and create employment.

Conclusion

The Open Credit Enablement Network (OCEN) holds immense promise in transforming India’s financial landscape. By leveraging technology, standardizing APIs, and fostering collaboration among stakeholders, OCEN aims to bring about financial inclusion, expand access to credit, and empower individuals and small businesses across the country. With its potential to revolutionize lending processes, OCEN is a

How does OCEN address data privacy concerns?

OCEN prioritizes data privacy and security by establishing a robust regulatory framework and ensuring compliance with data protection laws. The framework includes measures to safeguard borrower data while facilitating secure data exchange between lenders and data providers.

Can OCEN benefit individuals with limited digital literacy?

Yes, OCEN presents an opportunity to bridge the digital divide by encouraging digital literacy initiatives and making digital platforms more accessible to individuals with limited digital skills.

What role do digital platforms play in OCEN?

Digital platforms act as enablers, facilitating the integration of data providers and digital lenders. They ensure seamless data exchange and transaction processing, enhancing the efficiency of the lending ecosystem.

Will OCEN replace traditional financial institutions?

OCEN does not aim to replace traditional financial institutions but rather complements their efforts by providing a more inclusive and efficient lending framework.

How can OCEN contribute to India's economic growth?

By expanding access to credit, especially for underserved populations and small businesses, OCEN has the potential to spur entrepreneurship, stimulate economic activity, and contribute to India’s overall economic growth.