OCEN Framework and Loan Service Provider LSP, LSPs, fueled by the passion of volunteers, are at the forefront of addressing the challenges of financial inclusion. iSpirit, a prominent institution in this domain, firmly believes that lasting social change requires a long-term approach spanning two to three decades. While universities and research labs often play the role of long-term anchors in other societies, iSpirit has taken up this responsibility by leveraging technology and human capital to drive transformative change.

Unlocking the Potential: Democratizing Credit

iSpirit’s primary focus lies in the democratization of credit, a critical aspect of financial inclusion. Recognizing the complexity of this problem, they advocate for a dual approach: the development of robust public platforms and the fostering of private innovation. The belief is that by creating a solid foundation of public infrastructure, the stage is set for private innovators to build novel credit products and solutions that cater to diverse needs.

The Role of LSPs in the New Credit Ecosystem

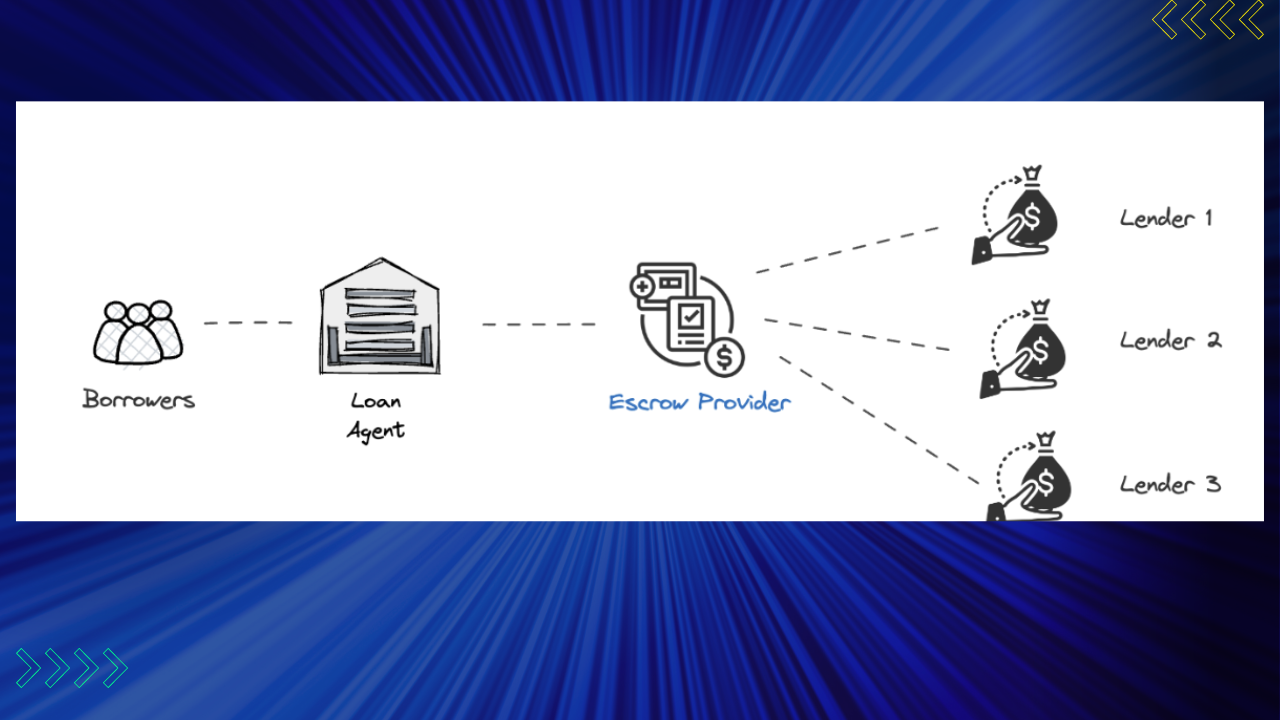

The new credit ecosystem envisages a cohesive collaboration between lenders, LSPs, and Micro, Small, and Medium Enterprises (MSMEs). LSPs act as intermediaries, facilitating the connection between lenders and MSMEs, thereby enabling access to credit for underserved businesses. This symbiotic relationship empowers entrepreneurs, spurring economic growth and creating new avenues for prosperity.

Exploring Opportunities for Private Innovators

Within this evolving landscape, private innovators hold the key to unleashing the full potential of financial inclusion. By leveraging the public infrastructure provided by LSPs, entrepreneurs can devise groundbreaking credit products and services. This opens up exciting avenues for existing players and new challengers to enter the market, each with a unique perspective and value proposition.

Addressing Queries and Expanding Knowledge

In our continuous endeavor to foster knowledge exchange, we appreciate the valuable queries shared by our audience. We aim to address these queries cohesively, both in subsequent sessions and through various channels, ensuring that all concerns are met comprehensively. By embracing a collaborative approach, we can collectively pave the way for a robust credit ecosystem that supports the aspirations of individuals and businesses alike.

The emergence of LSPs in the financial inclusion landscape brings renewed hope for millions of individuals and businesses seeking access to credit. Through the efforts of organizations like iSpirit and the dedication of volunteers, we can witness the gradual transformation of society. By fostering collaboration between public infrastructure and private innovation, we can unlock the true potential of credit democratization and create an inclusive financial ecosystem that propels economic growth. As we embark on this journey, let us embrace the opportunities and work towards a future where financial inclusion is no longer a distant dream but a tangible reality.

Checklist for an Entity to Become OCEN Loan Service Provider

To become a loan service provider, there are several vital points that an entity needs to consider. Let’s go through each of these points in detail:

- Engage with Open Resources: The entity must engage with the published open resources, such as the APIs provided. These resources are available on our website, “gedol.org,” and other channels. We encourage interested entities to explore these resources, provide feedback, and raise any queries they may have.

- Self-Assessment of Credit Products: After familiarizing themselves with the available data, the loan service provider (LSP) should conduct a self-assessment to determine the credit products they want to offer to their customers. This assessment should be done in collaboration with lenders, mapping the borrower personas to identify suitable product types.

- Access to API Sandboxes: Once the prospective LSPs have completed their self-assessment, further details regarding API sandboxes will be shared with them. These sandboxes allow LSPs to experiment and design different product experiences for their customers, offering a variety of loan products.

- Light Certification: After implementing the APIs, a light certification process facilitated by a trusted panel agency, such as Credo, ensures a seamless integration and uniform borrower experience across different LSPs. This certification covers aspects like security and ensures a delightful experience for borrowers consuming various offerings through the APIs.

- Go-Live Facilitation: The go-live process, where the LSP starts operating as a loan service provider, will be facilitated by Credo in collaboration with open-certified lenders. Further details about this process will be shared on our website and in upcoming sessions.

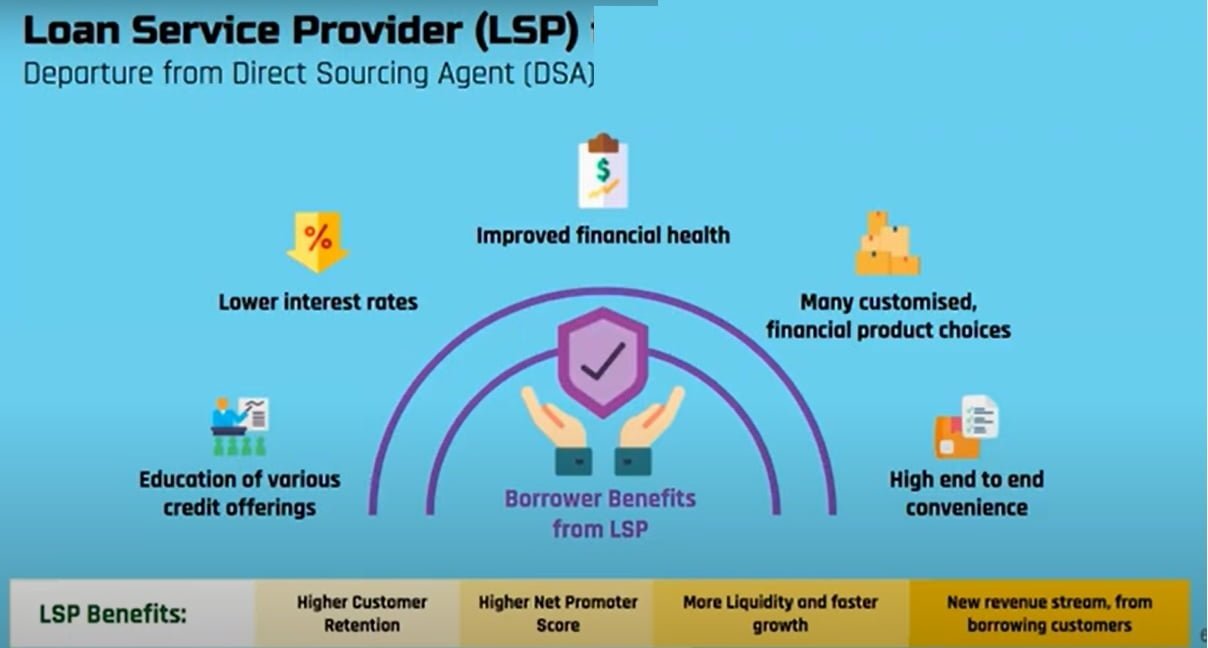

In summary, becoming a loan service provider involves collaboration among various capital providers, including lenders, rating agencies, underwriting modelers, data providers, and technology partners. LSPs play a vital role in bridging the gap between borrowers and lenders, leveraging public infrastructure to bring cash-flow lending to life. While our focus has primarily been on cash flow lending for MSMEs, we will also discuss cash flow lending for consumers in future sessions.

4 loan products that should be digitally distributed. Once wet signatures and physical signings are added, the costs escalate, making it impractical for small, standardized loan products. The key is to identify the end use of the loan and ensure that the funds are utilized for business purposes. Repayment should be facilitated by locking incoming cash flows, which can significantly reduce non-performing assets (NPAs) in the portfolio. While it may not eliminate all stress, it helps mitigate the risk associated with loan defaults. This hypothesis applies specifically to type four loans, making it easier for lenders, NBFCs, and fintech companies to create and distribute these credit products at scale.

To achieve this, we need new thinking and frameworks to develop innovative financial products and offerings. It’s essential to embrace cash flow-based lending for the Bharat market. Credol serves as a valuable source of information and collaboration for cash flow-based lending and is a collective effort involving various players in the lending ecosystem. We would like to share a broad checklist for entities aspiring to become loan service providers. We encourage interested parties to engage with the open resources, APIs, and business-related content published.