In the rapidly evolving world of banking and finance, technology plays a crucial role in transforming traditional practices and enhancing customer experiences. One such innovation that has gained significant momentum is the Open Credit Enablement Network (OCEN). 10 Banking Use Cases of OCEN, This revolutionary network empowers banks to collaborate, streamline processes, and provide a wide range of services to customers seamlessly. In this article, we will explore the empowering banking use cases of the Open Credit Enablement Network and how it is reshaping the financial landscape.

Empowering Banking: Open Credit Enablement Network Use Cases

The Open Credit Enablement Network (OCEN) is redefining the banking sector by enabling collaboration between financial institutions, fintech companies, and other stakeholders. It offers a wide array of use cases that empower banks to leverage technology, enhance customer experiences, and drive innovation. Let’s delve into some of the prominent use cases of the OCEN:

1. Seamless Loan Origination and Approval

With the OCEN, banks can digitize and automate the loan origination and approval processes, making it faster and more convenient for customers. By integrating various data sources and leveraging AI algorithms, banks can assess creditworthiness accurately and provide instant loan approvals. This streamlines the entire process, eliminating cumbersome paperwork and reducing turnaround time.

2. Collaborative Credit Scoring

The OCEN allows banks to collaborate and share credit data securely. By pooling data from various financial institutions, banks can enhance credit scoring models and make more informed lending decisions. This collaborative credit scoring approach helps in expanding credit access to underserved segments, fostering financial inclusion, and mitigating risks associated with lending.

3. Real-time Fund Transfers

Through the OCEN, banks can facilitate real-time fund transfers, enabling customers to send and receive money instantly. Whether it’s peer-to-peer transactions, bill payments, or merchant payments, the network ensures seamless and secure transfers, enhancing customer convenience and eliminating delays associated with traditional payment systems.

4. Open APIs for Innovation

The OCEN provides a standardized set of open APIs that allow banks and fintech companies to innovate and create new financial products and services. By leveraging these APIs, developers can build applications that integrate with the banking ecosystem effortlessly. This fosters a collaborative environment, drives innovation, and leads to the creation of a vibrant banking ecosystem.

5. Enhanced Customer Experience

The OCEN focuses on improving the overall customer experience by offering personalized services and tailored financial solutions. By leveraging customer data and advanced analytics, banks can understand individual preferences, anticipate needs, and offer customized products and services. This customer-centric approach strengthens customer loyalty and satisfaction.

6. Secure and Efficient Data Sharing

Data security is of paramount importance in the banking industry. The OCEN ensures secure data sharing among authorized parties through advanced encryption and access control mechanisms. This promotes trust and enables seamless collaboration while adhering to stringent data privacy regulations.

7. Financial Inclusion and Access to Credit

One of the key goals of the OCEN is to promote financial inclusion by extending access to credit for underserved segments of the population. By leveraging alternative data sources, such as utility bill payments, mobile wallet transactions, and social media data, banks can assess creditworthiness beyond traditional metrics. This opens up avenues for individuals with limited credit history to access formal credit facilities.

8. Streamlined Know Your Customer (KYC) Processes

The OCEN simplifies and streamlines the Know Your Customer (KYC) processes for banks. Through standardized APIs, banks can access and verify customer information from various sources, reducing duplication and enhancing efficiency. This saves time for both customers and banks, making the onboarding process smoother and more user-friendly.

9. Fraud Detection and Prevention

Fraud is a persistent concern in the banking industry, and the OCEN provides tools and capabilities to detect and prevent fraudulent activities. By leveraging advanced analytics, machine learning, and data from multiple sources, banks can identify suspicious patterns and potentially fraudulent transactions in real-time. This proactive approach helps in safeguarding customer assets and maintaining the integrity of the financial system.

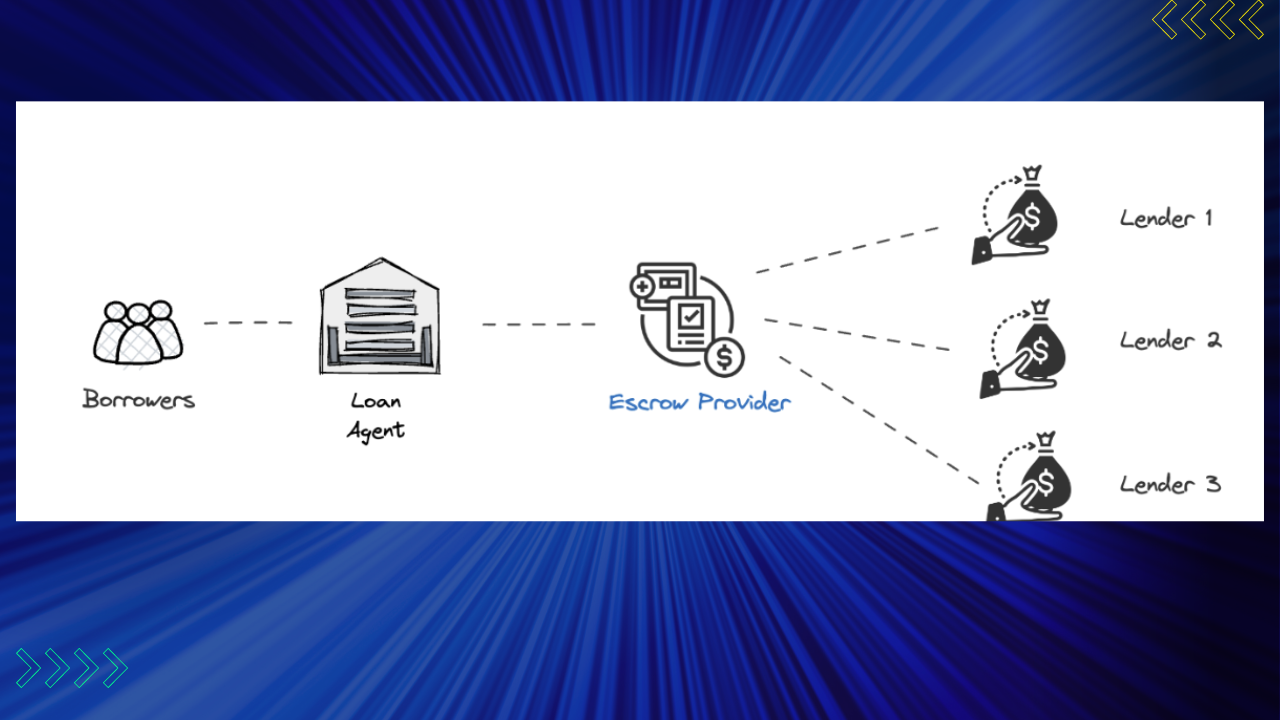

10. Open Credit Marketplaces

The OCEN enables the creation of open credit marketplaces where borrowers and lenders can connect directly. By leveraging the network’s infrastructure and standardized APIs, fintech companies and lenders can offer competitive loan products to borrowers, expanding credit options and fostering a more inclusive lending environment. This facilitates efficient matchmaking, and transparent pricing, and reduces the dependence on traditional intermediaries.

Conclusion

The Open Credit Enablement Network (OCEN) is transforming the banking industry by empowering financial institutions to collaborate, streamline processes, and provide innovative services. The network’s use cases, ranging from seamless loan origination to enhanced customer experiences, demonstrate its potential to reshape the financial landscape. By leveraging the OCEN, banks can drive financial inclusion, foster innovation, and deliver superior services to customers. As the banking industry embraces this open and collaborative ecosystem, the future of empowering banking through the Open Credit Enablement Network looks promising.