Strong Earnings Momentum Overshadows Market Expectations

IDFC First Bank delivered a commanding third quarter performance for FY2026, with net profit surging 48 percent year-over-year to ₹503 crore, demonstrating the bank’s improving operational efficiency and underlying business momentum. The quarter ended December 31, 2025, marked a pivotal inflection point in the bank’s profitability trajectory, even as certain margin pressures and valuation concerns remain focal points for investors navigating the private banking sector.

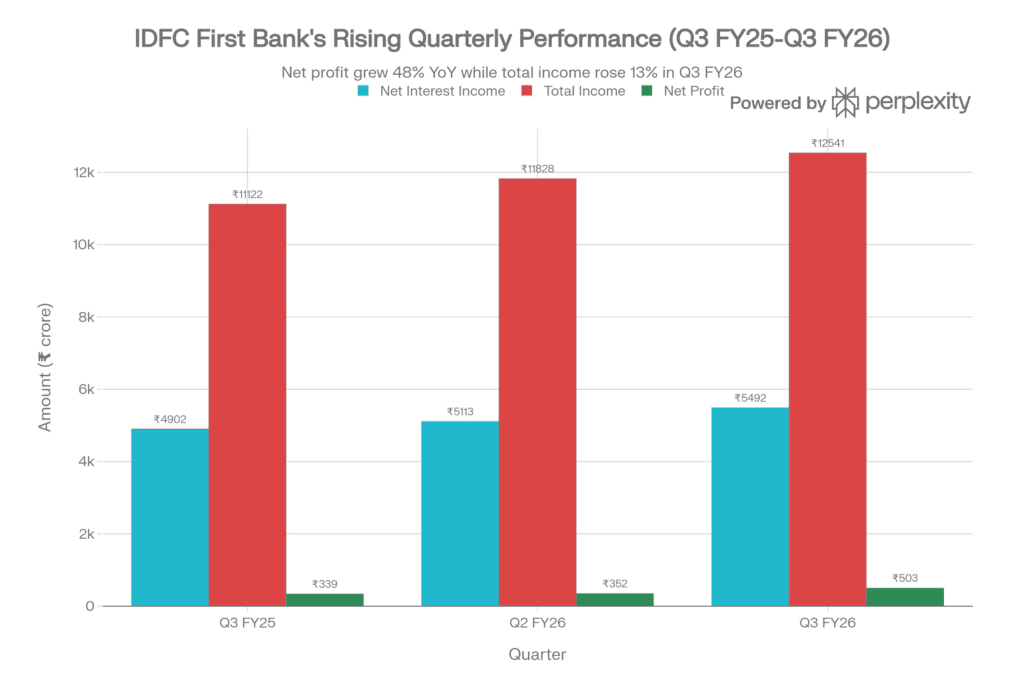

IDFC First Bank Quarterly Performance: Net Profit Surges 48% YoY

The bank’s profit growth accelerated substantially from the previous quarter’s ₹352 crore (Q2 FY26), representing a quarter-on-quarter improvement of 43 percent. This sequential momentum gains particular significance against the backdrop of a challenging macroeconomic environment characterized by persistent funding cost pressures and competitive deposit acquisition challenges. The profit expansion was underpinned by consistent gains in core banking metrics: total income reached ₹12,541 crore (up 12.7% year-over-year from ₹11,122 crore), while net interest income, the backbone of banking profitability, expanded to ₹5,492 crore, a gain of 12.0 percent year-on-year.

Net Interest Income: The Engine of Profitability Growth

Net interest income demonstrates the quality of the bank’s core earnings power and reflects management’s disciplined approach to deposit acquisition and lending strategy. The 12 percent year-on-year expansion to ₹5,492 crore substantially outpaced the broader sector growth rates, positioning IDFC First Bank as one of the higher-growth NII performers among India’s mid-tier private banks. The management previously guided for NII growth in the 9-11 percent range, making Q3’s performance a positive deviation from internal expectations.

This NII expansion becomes even more meaningful when examined against the bank’s strategic repositioning. Over the past two years, management has deliberately moderated loan growth in certain high-risk segments, particularly the microfinance institution (MFI) business, to fortify the underlying quality of the loan book. While this strategic reorientation temporarily pressured consolidated profitability through Q1 and Q2 FY26, the Q3 results indicate the bank is successfully transitioning to a more sustainable, higher-quality earnings trajectory.

A Market Expectations Miss on Profitability

Despite the impressive bottom-line growth, IDFC First Bank’s Q3 results fell slightly short of analyst consensus estimates for net profit. Market analysts had collectively estimated net profit between ₹500 crore and ₹800 crore, with more bullish estimates reaching the higher range. At ₹503 crore, the bank’s actual profit landed at the lower end of this expectation band, prompting some initial caution in post-results market commentary.

This apparent miss warrants deeper investigation. Management’s investor presentation reveals that the profit shortfall emanates not from operational underperformance but rather from a significant composition shift in profitability drivers. The bank’s “other income” (fee income, treasury gains, and non-interest earnings) reached approximately ₹1,048 crore compared to an estimated ₹820 crore in the prior-year quarter. This ₹228 crore sequential jump in other income masks what would otherwise have been a stronger underlying operating performance. When other income normalizes to historical run-rate levels in subsequent quarters, core profitability metrics will likely track closer to or above consensus expectations.

Funding Efficiency and Deposit Dynamics: The Path to Margin Expansion

IDFC First Bank’s balance sheet transformation over the past five quarters has been remarkable. Customer deposits expanded 24 percent year-over-year to reach ₹2,82,662 crore as of December 31, 2025, while the bank’s CASA (current account, savings account) ratio improved to 51.64 percent, a gain of 390 basis points versus the prior-year quarter. This deposit trajectory is critical to understanding the bank’s medium-term margin expansion potential.

Deposit and Loan Growth: IDFC First Bank’s Expanding Balance Sheet

The composition of this deposit growth—heavily weighted toward low-cost CASA deposits—directly translates to funding cost reduction and therefore net interest margin (NIM) expansion. The bank’s current account and savings account deposits grew 33 percent year-over-year to ₹1,50,350 crore, exceeding overall deposit growth rates and indicating accelerating traction in the critical CASA business. This metric carries outsized importance because each basis point of cost-of-funds reduction flows through to NIM expansion with minimal operational friction.

In early January 2026, IDFC First Bank reduced its savings account interest rates across multiple slabs, with reductions ranging from 100 to 200 basis points depending on account balance tiers. Independent analyst modeling suggests this rate action alone will generate approximately ₹890 crore in annualized interest savings, translating to roughly ₹155 crore in quarterly post-tax profit uplift by Q4 FY26. This structural funding cost benefit has largely not yet flowed through to Q3 earnings, positioning the bank favorably for H2 FY26 profitability.

Net Interest Margin Trends: Compression Persists but Relief is Visible

The bank’s net interest margin declined to 5.76 percent in Q3 FY26 from 6.04 percent in the corresponding quarter last year, representing a 28 basis point year-over-year compression. This decline reflects industry-wide margin pressure from persistently elevated funding costs, particularly for term deposits sourced at elevated rates during the 2022-2024 period. These higher-cost term deposits continue to reprice downward only gradually, creating a lagging effect on NIM expansion despite falling policy rates.

However, the quarter-over-quarter NIM trajectory provides encouragement. The net interest margin improved 17 basis points sequentially from 5.59 percent in Q2 FY26, indicating that the margin compression cycle may be entering its final quarters. Management guidance suggests NIM should expand to 5.8 percent or higher by Q4 FY26, supported by continued term deposit repricing and the aforementioned savings account rate reductions. Looking to FY27, analyst models incorporating the savings rate cuts and normal term deposit repricing suggest 40 basis points of potential steady-state NIM expansion, which would reposition the bank’s profitability trajectory materially.

Loan Growth Momentum: Balanced Across Segments

IDFC First Bank’s loans and advances expanded 21 percent year-over-year to ₹2,79,428 crore, substantially outpacing broader banking sector growth rates which hover in the 10-12 percent range. This above-market growth performance reflects the bank’s strategic positioning in retail lending, where credit penetration remains structurally low across India and demand remains strong.

The composition of loan growth reinforces quality. Management disclosed that 89 percent of year-over-year loan growth derived from diversified segments including mortgages (home loans), vehicle financing, consumer loans, business banking, and wholesale lending. Conspicuously absent from this growth composition was microfinance, which the bank has deliberately contracted as part of its portfolio optimization initiative. The microfinance portfolio declined from approximately ₹8,300 crore in Q2 to ₹7,300 crore in Q3, reflecting run-offs as the bank systematically reduces exposure to the structurally challenged MFI segment.

Within the broader portfolio, the credit card business continues to demonstrate outsized momentum. Credit cards in circulation reached 4.3 million during Q3, a meaningful achievement for a bank that launched its card product only in 2021. Credit card spends grew 30 percent year-over-year in Q2 and management commentary suggests sustained momentum. This credit card segment expansion is strategically important because card receivables typically generate 25-30 basis points higher yield than general personal loans, contributing to overall portfolio NIM strength.

Asset Quality: A Meaningful but Cautious Improvement

Asset quality metrics improved meaningfully in Q3 FY26, though management’s commentary suggests they are monitoring early-warning indicators closely. The gross non-performing asset (NPA) ratio declined to 1.69 percent as of December 31, 2025, from 1.86 percent in Q2 and 1.94 percent in the corresponding prior-year quarter. This 25 basis point year-over-year improvement represents genuine progress in loan book health.

Asset Quality Improvement: IDFC First Bank’s NPA Trajectory

The quarterly progression of gross NPA reduction (from 1.94% to 1.86% to 1.69%) suggests a consistent trajectory of improvement, driven by a combination of provisions for stressed assets and recoveries from prior-period slippages. However, the net NPA metric—which reflects NPAs after provision adjustments—remained essentially flat year-over-year at 0.53 percent, compared to 0.52 percent in Q3 FY25. This slight deterioration in net NPA, despite gross NPA improvement, indicates that provisioning levels have increased modestly on a sequential basis.

The bank’s provision coverage ratio stands at healthy levels, with total provisions of ₹1,398 crore in Q3 FY26. Notably, provisions declined 3.7 percent on a sequential basis from Q2’s ₹1,452 crore, suggesting management’s confidence in underlying asset quality trajectory. The bank disclosed that excluding the microfinance portfolio (which carries elevated stress), the core retail and commercial portfolio demonstrates robust credit metrics with normalized NPA levels and controlled slippage patterns.

Segment Diversification: Retail Leadership with Commercial Balance

IDFC First Bank’s loan book composition reflects a deliberate strategic rebalancing toward retail lending while maintaining meaningful commercial exposure. The detailed segment breakdown shows:

- Home Loans: 10 percent of portfolio, growing 25+ percent year-over-year

- Loans Against Property: 12 percent of portfolio, providing stable collateral-backed returns

- Business Banking: 4 percent of portfolio, growing 20+ percent year-over-year

- Salaried Personal Loans: 6 percent of portfolio

- Digital Personal Loans: 5 percent of portfolio, growing rapidly with improved digital distribution

This composition reflects what management characterizes as a “low-base, high-growth” strategy across retail segments, where penetration and market share remain substantially below larger competitors like HDFC Bank and ICICI Bank. The bank’s ability to sustain 20+ percent loan growth rates across this diversified retail book, while simultaneously improving asset quality, provides evidence of appropriate credit underwriting rigor.

Wealth Management: A Bright Spot in Non-Interest Income

While net interest income remains the primary driver of profitability, the bank’s wealth management business has emerged as a meaningful contributor to fee income. Wealth management assets under management surged 31 percent year-over-year to reach ₹58,957 crore in Q3 FY26, up from approximately ₹45,000 crore in the prior-year quarter. This 31 percent growth substantially outpaces both the broader mutual fund industry growth and competitor performance metrics, indicating successful client acquisition in the high-net-worth and ultra-high-net-worth segments.

The wealth management expansion holds strategic significance beyond the immediate fee generation. High-net-worth clients typically maintain multiple banking relationships, with wealth deposits serving as sticky, low-cost funding sources. The 31 percent growth in AUM therefore translates not only to incremental wealth management fee income but also to likely deposit inflows and cross-sell opportunities across lending and transaction banking products.

Valuation Considerations: Premium Positioning Requires Execution

IDFC First Bank currently trades at a trailing price-to-earnings (P/E) multiple of approximately 49-50 times, a substantial premium to the broader banking sector median P/E of approximately 15-16 times and even to peer banks like ICICI Bank (P/E ~18) and HDFC Bank (P/E ~19). This valuation premium reflects market expectations for sustained high earnings growth and expanding profitability margins.

The bank’s 48 percent profit growth in Q3 FY26, while impressive in absolute terms, must be contextualized within this valuation framework. To justify a 50x P/E multiple, the market is implicitly pricing in sustained 20+ percent earnings growth rates over a multi-year period. The bank’s management has guided for 16+ percent return on equity (ROE) by FY27, which translates to mid-teen percentage earnings growth given equity base growth rates. While achievable, this growth trajectory requires flawless execution on deposit acquisition, credit quality maintenance, and NIM recovery.

Any deterioration in asset quality metrics—particularly if non-MFI slippages accelerate—would pressure the valuation multiple downward, even if absolute profitability continues growing. Similarly, if competitive pressures force CASA deposit cost increases to exceed management’s expectations, NIM expansion could fall short of current consensus, creating a double headwind to near-term earnings growth rates.

Sectoral Comparison: IDFC First Bank in Context

Comparing IDFC First Bank’s Q3 FY26 performance against other Indian private banks reveals nuanced positioning. HDFC Bank, the sector’s largest private lender, delivered 11.5 percent net profit growth in Q3 FY26, substantially exceeding IDFC First Bank’s peer group but significantly below IDFC’s 48 percent growth rate. ICICI Bank reported net profit decline of 4 percent year-over-year in Q3, primarily due to elevated provisioning despite healthy loan growth.

IDFC First Bank’s profit growth substantially exceeds both HDFC and ICICI on a percentage basis, reflecting the bank’s rapid scaling off a smaller revenue base. However, both HDFC and ICICI generate substantially larger absolute profits, with HDFC’s quarterly PAT exceeding ₹18,600 crore versus IDFC’s ₹503 crore. The performance differential underscores IDFC’s position as a smaller, faster-growing competitor rather than a scale equivalent.

From a NIM perspective, ICICI Bank’s 4.30 percent net interest margin substantially exceeds IDFC’s 5.76 percent. This apparent contradiction reflects differences in business model and customer mix—ICICI’s larger wholesale and corporate portfolio naturally generates lower NIMs due to competitive pressure on yields. IDFC’s higher NIM reflects its retail-skewed portfolio, where per-unit margins are higher but volumes remain substantially below the largest peers.

Forward Outlook: Key Monitorables for Investors

As IDFC First Bank progresses through Q4 FY26 and into FY27, several metrics warrant close monitoring by investors considering exposure:

NIM Trajectory and Q4 Guidance: Management’s expectation for NIM of 5.8+ percent by Q4 FY26 should be closely verified against actual results. Any downside to this guidance would suggest competitive deposit pricing pressures exceeding expectations or faster-than-anticipated term deposit repricing outflows.

Microfinance Business Runoff: The planned exit from microfinance represents a strategic choice with near-term profitability headwinds and medium-term benefits. Management expects MFI-related losses to decline substantially in Q4 FY26 and subsequent quarters. Monitoring actual MFI portfolio trends is critical to confirming this guidance.

Credit Quality Trends Outside Microfinance: The core retail and commercial portfolio shows healthy underwriting metrics. However, if non-MFI slippages accelerate, this would require reassessment of credit cost guidance and asset quality trajectory.

Deposit Growth Sustainability: The 24 percent year-over-year deposit growth in Q3 represents accelerating momentum, particularly in CASA deposits. Verifying this growth is driven by organic client acquisition rather than price competition will be critical to confirming NIM expansion.

Loan Growth Composition: Monitoring whether 20+ percent loan growth rates are achievable while maintaining credit quality remains a key execution risk. If loan growth moderates materially, the valuation multiple compression risks intensify.

Conclusion: Solid Execution Against Demanding Market Expectations

IDFC First Bank’s Q3 FY26 results represent solid operational execution in an increasingly competitive banking environment. The 48 percent year-over-year profit growth, coupled with improving deposit composition and loan portfolio quality, demonstrates the bank’s ability to navigate margin pressures while scaling the business. The recent savings account rate reductions position the bank favorably for H2 FY26 margin expansion, while the wealth management acceleration provides encouraging evidence of non-interest income diversification.

However, the bank’s valuation premium requires sustained high-growth execution. The market is pricing in 20+ percent medium-term earnings growth rates, leaving limited margin for disappointment on core metrics. For investors, IDFC First Bank represents a well-executed growth story trading at valuations that reflect these high expectations. Selective investors comfortable with execution risk may find value in the bank’s strategic positioning and improving profitability trajectory, while others may prefer the relative valuation comfort and proven execution track records of larger peers like HDFC Bank and ICICI Bank. The next two quarters will provide critical evidence regarding whether management’s FY27 guidance is achievable, making them critical signposts for investment decision-making