Executive Summary

GAIL (India) Limited’s third-quarter FY2026 results reveal a company at an inflection point. While the state-run natural gas giant announced a landmark 12% transmission tariff hike effective January 2026—a critical step toward restoring profitability—Q3 performance fell significantly short of market expectations, with net profit collapsing 59% year-on-year to ₹1,602.57 crore. The disconnect between near-term operational deterioration and medium-term catalysts creates a complex investment calculus for shareholders evaluating the stock’s intrinsic value and recovery timeline.

The quarter represents the third consecutive profit decline and demonstrates that GAIL’s core business faces structural headwinds beyond cyclical commodity price fluctuations. Revenue stagnation (-2.5% year-on-year), margin compression across gas marketing and petrochemicals, and elevated cost inflation have collectively eroded shareholder returns despite the company’s dominant 65% market share in natural gas transmission. For a company trading at 11.46x earnings with a 4.48% dividend yield, Q3 results force investors to reassess the sustainability of GAIL’s cash returns and the timeline to margin stabilization.

This report provides institutional-grade analysis of GAIL’s Q3 FY26 performance, dissects segment-level deterioration, evaluates the tariff hike’s earnings accretion trajectory, and assesses execution risks that could derail the recovery narrative. Critically, the analysis separates signal from noise—distinguishing the one-time exceptional income items that distorted year-on-year comparisons from the underlying operational challenges that demand strategic remediation.

Financial Performance: Beyond the Headlines

GAIL Quarterly Financial Performance: Declining Trend Across Key Metrics

GAIL’s consolidated net profit declined 58% year-on-year to ₹1,729.13 crore in Q3 FY26, though adjusted metrics provide crucial context for interpreting underlying business health. The headline profit collapse masks a more nuanced operational picture: Q3 FY25 benefited from ₹2,440 crore in exceptional income, primarily from asset disposals, which artificially inflated prior-year comparisons. Stripping these one-time items, adjusted profit shows a 38% decline on a nine-month basis, reflecting genuine operational margin pressure.

Revenue Performance and Segment Dynamics

Standalone revenue from operations declined modestly by 2.5% year-on-year to ₹34,075.81 crore, a concerning signal given that consolidated revenues actually exceeded market estimates of ₹36,830 crore by approximately ₹1,500 crore. This apparent contradiction reveals weakness in the company’s international trading operations and LPG/liquid hydrocarbons segments—traditionally higher-margin businesses. The natural gas transmission segment, GAIL’s operational anchor, generated ₹2,760.81 crore in revenue with stable segment profitability of ₹1,376.09 crore, demonstrating the transmission business’s resilience despite volume headwinds.

The natural gas marketing segment tells a different story. Revenue of ₹30,605.41 crore (+1.2% year-on-year) masks a 70% collapse in segment profit to ₹853.18 crore from ₹2,880.98 crore in Q3 FY24. This deterioration reflects the fundamental challenge facing GAIL’s marketing operations: higher LNG procurement costs, driven by Henry Hub-linked contracts priced at $12.80/mmBtu for 2026, have compressed spreads across city gas distributor customers and industrial buyers whose willingness to pay remains anchored to conventional gas pricing at $6.55/mmBtu. With marketing revenues representing 90% of GAIL’s top line, this margin compression carries outsized impact on consolidated profitability.

Petrochemicals reported losses of ₹482.64 crore in Q3 FY26, a ₹487 crore swing from minimal profits in Q3 FY24. The segment continues to suffer from soft product markets and operational constraints, despite management guidance targeting capacity expansions to 1,250 KTA of PTA (purified terephthalic acid) and 500 KTA of polypropylene by FY27. Current losses suggest the segment remains unprofitable at prevailing market prices, creating a drag on consolidated returns.

Margin Compression: The Structural Profitability Challenge

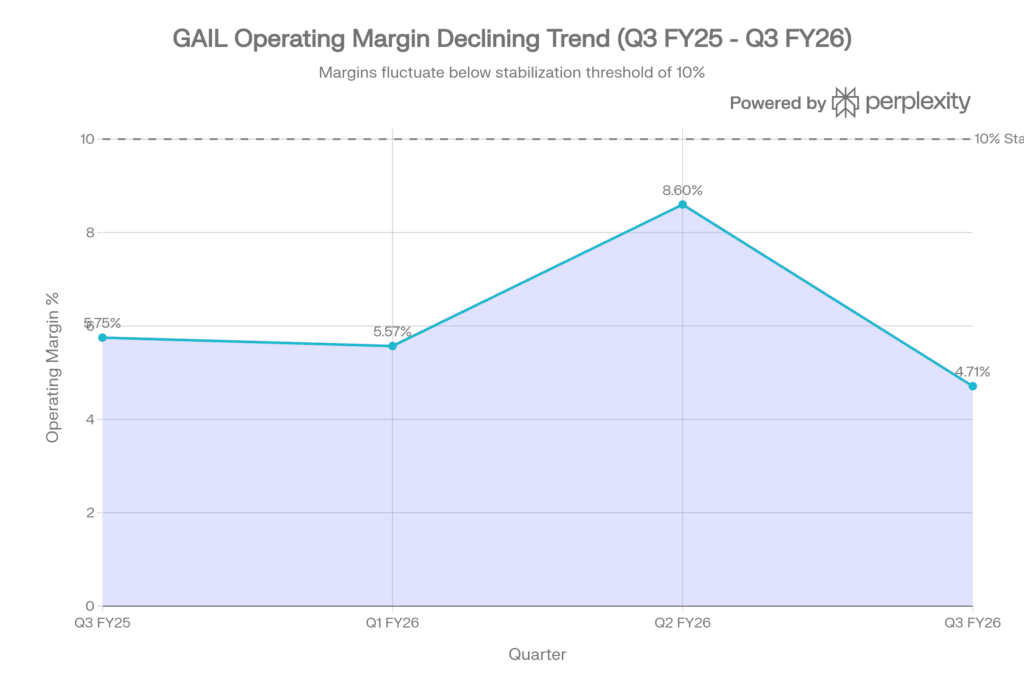

GAIL Operating Margin Compression: Sequential Quarterly Decline

GAIL’s net profit margin contracted to 4.71% in Q3 FY26 from 5.75% in Q3 FY25, continuing a troubling six-quarter erosion pattern that has yet to stabilize. More critically, the operating margin (excluding other income) fell to 8.32%, marking the lowest quarterly performance in seven quarters and indicating core business deterioration independent of financing costs or tax impacts. This metric matters because it isolates operational execution from capital structure decisions—and the deterioration is unmistakable.

The margin compression stems from two sources: (1) revenue headwinds from declining transmission volumes and LNG-driven marketing margin compression, and (2) cost inflation. Depreciation charges increased 26.89% year-on-year to ₹1,191.94 crores despite flat revenue, reflecting GAIL’s capital-intensive infrastructure model where new pipelines deployed in prior years now cycle into depreciation expense. Interest costs rose 49.90% year-on-year to ₹253.78 crore, driven by elevated debt levels and rising interest rates, though the debt-to-equity ratio remains manageable at 0.25x.

The earnings-per-share decline of 58.5% to ₹2.44 (from ₹5.88 in Q3 FY24) translates directly to shareholder value erosion. Despite GAIL maintaining a dividend payout ratio of approximately 40%, the combination of flat earnings growth and elevated capital intensity creates a precarious equation: management must either reduce capital expenditure (risking long-term competitive positioning), maintain high debt levels (increasing financial risk), or accept dividend cuts (pressuring share valuation). Current guidance of ₹4,000-4,500 crore in natural gas marketing margins for FY26 suggests management expects sequential improvement in Q4, yet three quarters into the year, the company has already captured only ₹2,221 crore, requiring an improbable ₹1,800-2,300 crore in the final quarter.

Nine-Month Performance: Revenue Growth Masks Profitability Headwinds

For the nine months ended December 31, 2025, GAIL posted standalone revenue of ₹1,03,899.50 crore, representing modest 2.3% growth versus ₹1,01,580.11 crore in the comparable period last year. This revenue resilience creates an optical advantage—the company can credibly claim demand recovery in certain segments—but profit deterioration of 38.4% year-on-year to ₹5,706.13 crore reveals the profit-revenue disconnect.

| Financial Metric | 9M FY26 | 9M FY25 | Change | % Growth |

|---|---|---|---|---|

| Revenue from Operations | ₹1,03,899.50 Cr | ₹1,01,580.11 Cr | +₹2,319.39 Cr | +2.3% |

| Profit Before Tax | ₹7,386.60 Cr | ₹12,123.49 Cr | -₹4,736.89 Cr | -39.1% |

| Net Profit After Tax | ₹5,706.13 Cr | ₹9,263.29 Cr | -₹3,557.16 Cr | -38.4% |

| Operating Profit Margin | Not directly disclosed | Est. 12%+ | Est. decline to 7-8% | Severe compression |

| Debt-to-Equity Ratio | 0.25x | 0.23x | +0.02x | Deteriorating |

| Interest Service Coverage Ratio | 11.45x | Strong historical levels | Remains adequate | Stable |

The nine-month results underscore a critical insight: GAIL’s top line remains hostage to commodity cycles and demand elasticity, while its cost structure has become increasingly rigid. Fixed depreciation and maintenance expenses have risen in absolute terms alongside working capital requirements, leaving operational leverage compressed and earnings volatility elevated.

Segment Analysis: Transmission Resilience, Marketing Weakness, Petrochemicals Losses

GAIL’s three-pronged business model—transmission, marketing, and petrochemicals—exhibits divergent trajectories that illuminate where the company’s strategic positioning requires reinforcement.

Natural Gas Transmission: The Profit Anchor

With segment profit of ₹1,376.09 crore on revenue of ₹2,760.81 crore, transmission achieves a 50% operating margin—the company’s healthiest business by far. Transmission volumes of 122 MMSCMD in H1 FY26, while down 4% from the historical peak of 127 MMSCMD in FY25, demonstrate the segment’s resilience in a challenging demand environment. Management guidance projects transmission volumes reaching 133-134 MMSCMD by FY27, supported by pipeline completion projects including the Sanas- Adoption-Parli-Loni (SAPL) and Mangalore-Nashik-Jharkhand (MNJPL) pipelines.

The 12% tariff hike approved by the Petroleum and Natural Gas Regulatory Board (PNGRB) effective January 1, 2026—raising the integrated pipeline tariff from ₹58.61 to ₹65.69 per million British thermal units (mmBtu)—represents ₹1,200 crore in incremental annual revenue. Analysts project this tariff hike will boost FY27 EBITDA and profit-after-tax by 7-8%, translating to approximately ₹350-400 crore in incremental quarterly profit run-rate from FY27 onwards. However, critically, the one-year implementation delay—GAIL requested January 2025 but received January 2026—means the company forfeits ₹1,200 crore in FY26 revenue opportunities. This regulatory timing creates a meaningful earnings headwind in FY26 that will not fully reverse until H1 FY27 comparisons.

Natural Gas Marketing: Margin Compression and LNG Price Risk

The marketing segment recorded ₹30,605.41 crore in revenue with segment profit of just ₹853.18 crore, implying a 2.79% operating margin versus the historically comfortable 4.5-5%+ range. This represents a 70% year-on-year decline in absolute profit, driven by a perfect storm: declining domestic gas allocations, elevated LNG import costs under Henry Hub-linked contracts, and customer price resistance.

India’s natural gas demand has stagnated at approximately 190-192 mmscmd through August 2025, down 1% year-on-year, with domestic production declining and LNG imports constrained by elevated spot prices. The crucial dynamic: GAIL’s Henry Hub-linked LNG import contracts, averaging $12.80/mmBtu delivered for 2026, exceed conventional gas prices ($6.55/mmBtu) by over 95%. City gas distributors and industrial customers—GAIL’s primary marketing customers—face margin compression and demand elasticity constraints at these cost levels. While GAIL maintains marketing margin guidance of ₹4,000-4,500 crore for FY26 at the profit-before-tax level, the company has captured only ₹2,221 crore through nine months, creating a significant execution risk. The implied guidance would require the marketing segment to earn ₹1,800-2,300 crore in Q4 FY26—approximately 81-104% higher than Q3 levels—an unlikely outcome given current demand and pricing dynamics.

Encouragingly, overseas sales have tripled to 13.58 MMSCMD in H1 FY26 from 4.11 MMSCMD in H1 FY25, signaling management’s success in diverting higher-cost LNG to export markets and protecting domestic customers from absorbing full commodity price pressures. This strategic rebalancing may prevent further marketing margin deterioration but unlikely to restore prior-year profit levels in the near term.

Petrochemicals: Structural Losses and Capacity Expansion Risk

The petrochemicals segment posted an ₹482.64 crore operating loss in Q3 FY26, a ₹487 crore deterioration from minimal profitability in Q3 FY24. The loss-making trajectory reflects chronically soft polypropylene and polyester markets in India, oversupply from competing producers, and operational challenges at GAIL’s existing plants.

Management has positioned petrochemicals as a growth engine, with commissioning of three plants targeted: 1,250 KTA of PTA at GAIL Mangalore Petrochemicals Limited (GMPL), 500 KTA at Usar, and 60 KTA at Pata, all expected to come online by late 2025 to early 2026. However, expanding capacity into chronically unprofitable petrochemical segments carries execution risk. If these plants commence at low operating rates or face prolonged ramp-up periods—not uncommon for petrochemical facilities—the depreciation tax will amplify bottom-line losses. Conversely, if industry margins recover faster than the company’s peers, incremental capacity could improve divisional profitability. Current losses argue for caution: petrochemicals contributed approximately -3% to divisional profitability in Q3 FY26, and without dramatic market recovery or demonstrated operational excellence, capacity expansion could deepen losses before driving returns.

Catalysts and Recovery Narrative: The Tariff Hike as Cornerstone

GAIL’s investment thesis hinges critically on the transmission tariff hike materializing into shareholder value. The comprehensive analysis reveals the tariff hike mechanism and its constraints:

Tariff Hike Mechanics and Expected Impact

The PNGRB-approved 12% tariff increase, while representing a “win” for GAIL, fell materially short of the company’s 33% request. The shortfall reflects regulatory conservatism: PNGRB granted only interim relief on a subset of tariff components, deferring comprehensive review parameters (including operational expenditure adjustments, capital expenditure recognition, transmission loss calculations, and revenue-sharing arrangements) to a next full review scheduled for April 2028.

The 12% increase comprises two elements: (1) ₹5.16/mmBtu System Use Gas (SUG) increase due to the Indian government’s withdrawal of domestic gas subsidies for pipeline operations, forcing GAIL to procure market-priced gas at $10-10.50/mmBtu versus prior subsidized rates of $3.61/mmBtu, and (2) ₹1.92/mmBtu adjustment for lower volume divisor based on revised capacity estimates. This composition matters: the SUG increase is largely a pass-through of input cost inflation rather than true margin expansion. True tariff-based profit recovery depends on transmission volume growth and operational leverage on the incremental ₹1.92/mmBtu capacity adjustment.

Analysts project the tariff hike will contribute 7-8% to FY27 EBITDA and PAT growth, translating to approximately ₹300-400 crore in incremental quarterly earnings run-rate. However, this assumes volumes reach the 133-134 MMSCMD guidance for FY27, a prerequisite that remains contingent on successful execution of pipeline expansion projects and industrial sector demand normalization.

Volume Growth Trajectory and Execution Risk

GAIL management projects transmission volumes of 133-134 MMSCMD in FY27, representing 8-10 MMSCMD growth from current levels around 124 MMSCMD. This growth would require: (1) successful commissioning and ramp-up of SAPL and MNJPL pipelines, (2) normalization of industrial demand following commodity cycle lows, and (3) recovery in power sector gas demand. Current H1 FY26 volumes of 122 MMSCMD, though down 4% year-on-year, suggest the base case for volume recovery faces headwinds.

Critically, the tariff hike’s FY27 benefit occurs with one full quarter already in FY26 (January-March 2026), meaning Q4 FY26 will capture only three months of tariff benefit. Full-run-rate impact begins only in Q1 FY27, creating a phased earnings accretion timeline that differs from market expectations. Investors should model Q4 FY26 profit contribution from the tariff hike at approximately ₹75-100 crore (representing three months of annualized ₹1,200 crore revenue benefit, net of operating leverage), not the full quarterly impact.

Gas Demand Recovery and Market Structure Risks

India’s natural gas demand environment remains challenged. Total demand of approximately 190 mmscmd in August 2025, down 1.2% year-on-year, reflects both cyclical weakness and structural headwinds. Domestic gas production continues declining, forcing incremental demand to be met through LNG imports priced at elevated levels. Unless spot LNG prices ease materially or Henry Hub-linked pricing normalizes (both uncertain in 2026), customer price resistance will constrain volume growth even as infrastructure capacity expands.

GAIL Chairman Sandeep Kumar Gupta has expressed optimism about emerging demand drivers—data centers, steel, cement, and petrochemicals—but acknowledged that taxation remains a constraint. Current 14% GST on compressed natural gas (CNG) compression costs suppresses demand elasticity relative to alternative fuels. Government policy changes could unlock this trapped demand, though legislative implementation risk remains high.

Capital Structure and Dividend Sustainability

GAIL declared an interim dividend of ₹5.00 per equity share for FY2026, representing a 50% payout ratio on a face value of ₹10. With record date of February 5, 2026, the dividend translates to total payout of ₹3,287.55 crore. Current dividend yield of 4.48% significantly exceeds both the market average and most gas utility peers, making GAIL an attractive income play for yield-focused investors.

However, dividend sustainability warrants scrutiny. The interim dividend is predicated on normalized earnings assumptions that current Q3 results call into question. Maintaining ₹5 per share annually—totaling ₹3,287.55 crore—requires net profit of approximately ₹8,200-8,500 crore annualized (at current market-implied payout ratios). Current nine-month profit of ₹5,706.13 crore annualizes to only ₹7,608 crore, creating a ₹600-900 crore shortfall. Q4 FY26 must deliver ₹1,500+ crore in profit to achieve prior guidance—approximately 50% higher than Q3 levels despite seasonal factors and absent the benefit of full-quarter tariff hike impact.

GAIL’s debt-to-equity ratio of 0.25x remains conservative, and the interest service coverage ratio of 11.45x provides adequate debt servicing buffer. Long-term debt has declined to ₹10,781.04 crore from ₹12,806.02 crores in the prior year, indicating disciplined capital allocation. However, the company maintains capital expenditure guidance of ₹8,000+ crore annually, with allocation shifting toward city gas distribution (11% vs. 6% historically) at the expense of transmission capacity development. This capital reallocation signals management’s acknowledgment that transmission growth will decelerate post-pipeline completion, necessitating downstream distribution investments to sustain returns.

Valuation and Investment Metrics: Reasonably Priced Amid Uncertainty

At January 30, 2026, GAIL traded at ₹167.29 per share, implying a P/E multiple of 11.46x on trailing twelve-month consolidated earnings. This valuation sits modestly above the company’s historical five-year average of 8.86x but below the March 2023 peak of 12.32x, positioning the stock in the lower quartile of valuations for capital-intensive infrastructure companies.

| Valuation Metric | Current | Historical Average | Peer Median | Assessment |

|---|---|---|---|---|

| P/E Ratio | 11.46x | 8.86x | 15-16x (Integrated Utilities) | Fair value |

| Price-to-Book | 1.24x | 1.10x | 1.5-2.0x | Discount territory |

| EV/EBITDA | 8.3x | 7.5x | 8-9x | In-line |

| Dividend Yield | 4.48% | Historical 3.5-4% | 2.6% (Gas utilities) | Above average |

| PEG Ratio (2% growth) | 5.73x | Historical 4-5x | N/A | Elevated |

The valuation framework reveals that GAIL commands a modest discount to history and peers, justified by current earnings headwinds and uncertainty regarding tariff benefit realization. An analyst price target of ₹220 per share (implying 31% upside from January 30 levels) assumes successful execution of tariff hike and volume recovery catalysts. At ₹220, the implied P/E would be approximately 14.3x on FY27E earnings of ₹15.4, in line with improved profit trajectory.

Dividend yield of 4.48% provides an equity risk premium cushion: even if earnings remain flat to slightly declining in FY26 and FY27, the dividend yield protects downside and provides attractive income for yield-focused investors. However, growth investors expecting earnings expansion beyond tariff hike impacts face limited upside without demonstration of marketing segment margin recovery and petrochemicals profitability inflection.

Risk Factors: Headwinds That Could Derail Recovery

Alongside catalysts, material risks threaten GAIL’s earnings recovery and dividend sustainability:

Contingent Liabilities and Regulatory Exposure

GAIL carries contingent liabilities totaling ₹2,889 crore related to a Central Excise demand regarding Naphtha classification, with accumulated interest of ₹3,737 crore as of December 31, 2025. While management asserts the company maintains strong legal opinions supporting its position and has appealed to the Supreme Court, a potential adverse ruling could result in ₹6.6+ crore outflow, materially impacting shareholder equity and credit metrics. The company also contests PNGRB tariff appeals and maintains outstanding receivables of ₹915.68 crore from Nagarjuna Fertilizers and Chemicals Limited under government subsidy arrangements, creating additional balance sheet vulnerabilities.

LNG Price Volatility and Margin Pressure Persistence

The near-term margin pressure stemming from elevated Henry Hub-linked LNG import costs carries tail risk. If spot LNG prices remain elevated through 2026 and Henry Hub futures fail to revert to historical $4-5/mmBtu norms, GAIL’s marketing customers may further reduce volumes or accelerate demand destruction through fuel switching. While GAIL has demonstrated export redirection capability (overseas sales tripled), this strategy cannot indefinitely absorb high-cost LNG without pressuring consolidated profitability.

Transmission Volume Growth Uncertainty

The 8-10 MMSCMD volume growth guidance for FY27 assumes successful commissioning of SAPL and MNJPL pipelines by scheduled dates and industrial demand normalization. Construction delays, permitting challenges, or demand shortfalls could compress volume growth to 4-6 MMSCMD, materially eroding the tariff hike’s earnings accretion. Pipeline projects in India frequently experience delays due to right-of-way challenges, environmental clearances, and execution constraints.

Petrochemicals Capacity Ramp-Up Execution

Expansion into 1,250 KTA of PTA and 500 KTA of polypropylene capacity introduces operational risk. If ramp-up timelines extend or market conditions remain soft, the depreciation tax from newly deployed capital could deepen segment losses. Historical experience across the Indian petrochemical industry suggests new capacity faces 12-24 month ramp-up periods, during which fixed cost absorption is suboptimal.

Forward-Looking Analysis: Path to Recovery

GAIL’s FY26 and FY27 earnings trajectory depends critically on sequence of events unfolding as management projects:

Base Case Scenario (50% Probability)

- Q4 FY26 profit recovery to ₹1,800-1,900 crore, driven by seasonal demand strength and initial tariff hike benefit

- FY26 full-year PAT of ₹7,300-7,500 crore (vs. current nine-month ₹5,706 crore), requiring ₹1,600-1,800 crore Q4

- FY27 tariff hike benefits materialize as projected, with transmission volumes reaching 133-134 MMSCMD

- Marketing segment margins recover to 4-4.5% range as overseas LNG diversion continues

- FY27 PAT grows 12-15% to ₹8,200-8,600 crore

- Dividend maintained at ₹5-6 per share; stock appreciation to ₹180-200 range

Bull Case (25% Probability)

- Tariff hike provides stronger-than-expected profit lift (₹1,500+ crore annually vs. ₹1,200 crore)

- LNG prices ease in 2H 2026, restoring marketing margins to 4.5-5% range

- Transmission volumes exceed guidance at 135-140 MMSCMD

- Petrochemicals capacity ramps successfully, achieving breakeven by late FY27

- FY27 PAT grows 20%+ to ₹8,800+crore

- Dividend grows to ₹6-7 per share; stock reaches ₹220-250

Bear Case (25% Probability)

- Marketing segment margins remain compressed at 2.5-3% due to persistent LNG price elevation

- Transmission volume growth disappoints, reaching only 128-130 MMSCMD vs. 133-134 MMSCMD guidance

- Petrochemicals capacity ramp-up extends, losses widen to ₹600+ crore annually

- Contingent Central Excise liability materializes, requiring provision

- FY27 PAT flat to slightly down at ₹5,400-5,600 crore

- Dividend reduced to ₹4 per share to preserve cash; stock retreats to ₹130-140

Conclusion: Income Investment With Tariff-Dependent Recovery

GAIL Q3 FY26 results signal a company navigating a critical transition from cyclical margin compression toward tariff-driven earnings recovery. The 59% profit decline year-on-year reflects genuine operational headwinds—demand stagnation, LNG cost inflation, and working capital pressures—not mere accounting artifacts. However, the 12% transmission tariff hike, while modest relative to GAIL’s 33% request, establishes a foundation for earnings stabilization in FY27.

For yield investors seeking 4.5%+ dividend income with modest capital appreciation, GAIL offers reasonable value at 11.46x earnings and 4.48% dividend yield. The dividend appears sustainable on a base case earnings trajectory, and downside risk is cushioned by the strong income stream. For growth investors, the calculus is less favorable: earnings momentum remains negative, petrochemicals risk is material, and the tariff hike provides only partial profit recovery. Execution of volume growth guidance and cost management will determine whether recovery translates to a multi-year earnings expansion or reverts to stagnation.

Near-term catalysts focus on Q4 FY26 earnings delivery—particularly the critical question of whether the company achieves ₹1,600-1,800 crore profit in the final quarter to reach prior guidance. Market sentiment remains cautiously optimistic, with analyst price targets of ₹220 suggesting 31% upside from current levels. However, tariff realization and volume execution risk justify a wait-and-see posture until Q4 results and FY27 guidance provide concrete evidence of recovery materialization.