Tata Motors’ first quarter of fiscal year 2026 revealed a company grappling with significant headwinds across all business segments while positioning itself for long-term strategic transformation. The automaker reported a 63% decline in consolidated net profit to ₹3,924 crore, down from ₹10,587 crore in the same period last year, primarily due to volume declines, margin compression, and severe tariff-related impacts on its premium Jaguar Land Rover (JLR) division.

Tata Motors Q1 FY26 Financial Performance: Revenue, Profit, and Margin Analysis

Financial Performance Overview

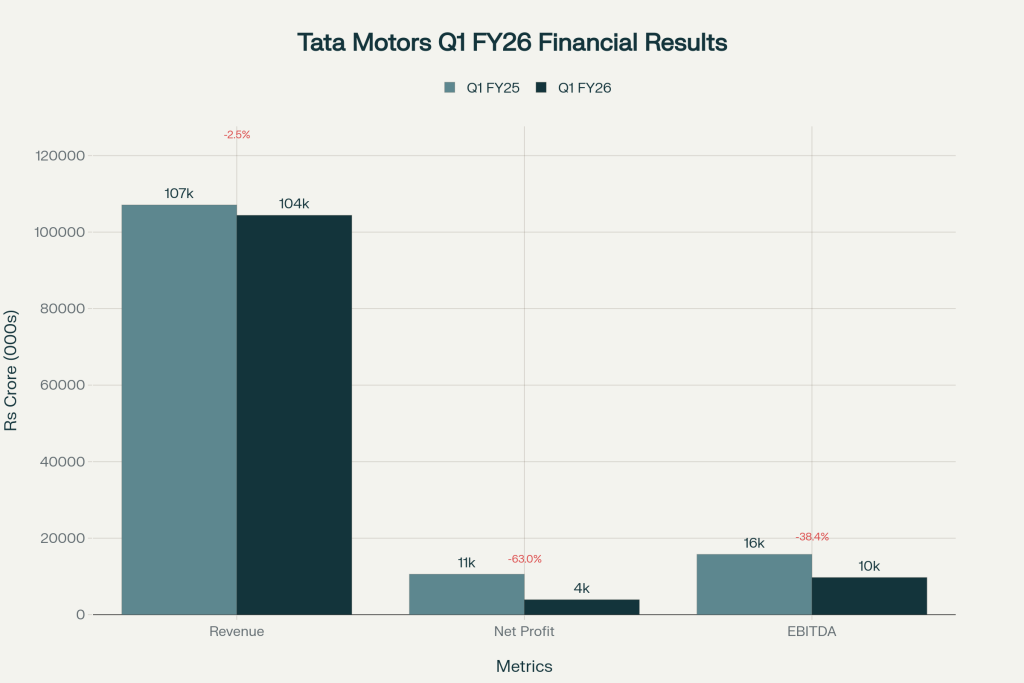

The quarter’s financial metrics paint a picture of a company under pressure from multiple fronts. Consolidated revenue declined 2.5% year-on-year to ₹1,04,407 crore, while EBITDA margins compressed significantly from 14.7% to 9.3%, representing a contraction of 540 basis points. The earnings before interest and tax (EBIT) margin fell to 4.3% from 8.0% in the previous year, highlighting the severity of operational challenges.

Earnings per share (EPS) plummeted by 66.3% to ₹10.66 from ₹31.63 in Q1 FY25, reflecting the substantial impact on shareholder returns. Despite these challenging numbers, the results were largely in line with analyst estimates, suggesting that the market had anticipated the difficult operating environment.

The company’s financial performance was significantly impacted by the absence of a one-time gain from discontinued operations that had boosted the previous year’s results by approximately ₹4,975 crore. This base effect, combined with operational challenges, contributed to the stark year-over-year comparison.

Jaguar Land Rover: Bearing the Brunt of Trade Tensions

JLR faced the most severe challenges during the quarter, with revenue declining 9.2% to £6.6 billion and EBIT margins contracting by 490 basis points to 4.0%. The luxury car division was hit hard by the implementation of 27.5% US trade tariffs on UK and EU-produced vehicles exported to the United States, resulting in an estimated impact of approximately £250 million during the quarter.

A luxury Range Rover Sport prominently displayed in a sleek, modern Land Rover showroom alongside other Land Rover models

The situation was compounded by the planned wind-down of legacy Jaguar models ahead of the brand’s transformation strategy, which reduced wholesale volumes by 10.7% year-on-year to 87,286 units. Despite these challenges, JLR maintained its position as a profitable entity, delivering its 11th successive profitable quarter.

Relief is on the horizon with the signing of the UK-US trade deal, which will reduce tariffs on UK-produced vehicles from 27.5% to 10%, effective from June 30, 2025. Additionally, the EU-US trade deal announced in July 2025 will further reduce tariffs on JLR’s EU-produced vehicles from 27.5% to 15%.

Indian Operations: Commercial and Passenger Vehicles Under Pressure

Commercial Vehicles Segment

The commercial vehicles division experienced a 4.7% decline in revenue to ₹17,009 crore, with wholesale volumes dropping 6% to 88,000 units. However, there were positive signs within this challenging environment, as EBITDA margins improved by 60 basis points to 12.2%, supported by better realizations and cost savings despite lower volumes.

Tata Motors launches India’s first hydrogen-powered heavy-duty truck as part of its commercial vehicle innovation initiative

Domestic volumes declined 9% year-on-year, reflecting broader market softness and delayed fleet replacement cycles. However, the segment showed resilience in certain areas, with exports growing 68% and segments like buses and vans demonstrating stability.

Passenger Vehicles Segment

The passenger vehicles business faced significant headwinds with revenue declining 8.2% to ₹10,877 crore and wholesale volumes dropping 10.1% to approximately 124,800 units. The segment’s EBIT margin turned negative at -2.8%, deteriorating by 310 basis points year-over-year.

The new Tata Nexon SUV showcased at a Tata Motors event with modern design highlights and branding

The electric vehicle segment remained a bright spot within the passenger vehicle portfolio, maintaining steady penetration at 13% with wholesale volumes of 16,200 units during the quarter. However, this represented a slight decline from the previous year, highlighting increasing competition in the EV space.

Market Context and Industry Dynamics

The challenging performance must be viewed within the broader context of the Indian automotive industry’s Q1 2025 dynamics. The passenger vehicle segment across the industry experienced volume pressures, with flat growth reflecting continued softness in demand. The industry witnessed highest-ever Q1 exports of 2.04 lakh units, registering 13.2% growth, indicating stronger international demand compared to domestic market conditions.

The shift towards utility vehicles continued, with UVs accounting for 66% of the passenger vehicle segment and posting 3.8% growth, while passenger cars degrew by 11.2%. This trend aligns with changing consumer preferences for safer, smarter, and more feature-rich vehicles.

Strategic Transformation: The Demerger Initiative

One of the most significant strategic developments is the upcoming demerger scheduled for October 2025. The final hearing for the demerger scheme was concluded by the National Company Law Tribunal on August 8, with the order reserved. This separation will create two distinct listed entities: one focused on commercial vehicles and another encompassing passenger vehicles, electric vehicles, and JLR.

The demerger strategy aims to unlock shareholder value by allowing each business segment to operate with greater focus and agility. The commercial vehicle entity will be able to capitalize on infrastructure growth and global opportunities, while the passenger vehicle entity can concentrate on electric mobility, autonomous vehicles, and connected car technologies.

Electric Vehicle Strategy and Future Roadmap

Tata Motors is doubling down on its electric vehicle leadership despite facing increased competition. The company has outlined ambitious plans to achieve 30% EV penetration in its portfolio by 2030. To support this goal, TATA.ev announced plans to more than double India’s charging infrastructure to 400,000 charge points by 2027.

Tata Power electric vehicle charging station powering a Tata Motors EV outdoors

The company is investing ₹18,000 crore in its EV division over the next six years and plans to launch 10 new EV models by FY26. The strategy includes developing native EV platforms capable of delivering over 500 km range and achieving price parity with internal combustion engine vehicles by 2030.

Management Outlook and Guidance

Despite the challenging Q1 performance, management remains cautiously optimistic about the second half of fiscal year 2026. PB Balaji, Group Chief Financial Officer, emphasized that the company delivered a profitable quarter despite stiff macro headwinds, supported by strong fundamentals.

Key management guidance includes:

- JLR EBIT margin guidance of 5-7% for FY26 remains unchanged despite Q1 challenges

- Focus on strong second-half performance leveraging festive demand and tariff clarity

- Commercial vehicle recovery expected driven by monsoon normalization, infrastructure activity, and easing interest rates

- Capex allocation of ₹30,000-35,000 crore for FY26-30 focused on passenger vehicles and electric vehicles

Market Response and Analyst Sentiment

The stock market reaction reflected the challenging operating environment, with Tata Motors shares declining 2.43% on the day of results announcement. The stock has been under pressure throughout 2025, declining approximately 16% year-to-date and trading significantly below its 52-week high.

Analyst recommendations remain mixed but generally positive for the long term, with 60% recommending “Buy,” 26.67% suggesting “Hold,” and 13.33% advising “Sell”. The average price target of ₹848 represents potential upside from current levels, though there’s significant variation in analyst expectations.

Risk Assessment and Challenges Ahead

Several key risks persist that could impact the company’s recovery trajectory:

- Continued geopolitical tensions affecting trade relationships and tariff structures

- Intensifying competition in the EV segment from both established and new players

- Demand volatility in key markets amid economic uncertainties

- Execution risks related to the demerger process and timeline

- Margin pressure from cost inflation and competitive pricing

Recovery Prospects and Strategic Positioning

Despite near-term challenges, Tata Motors is positioning itself for long-term success through several strategic initiatives:

The demerger will create more focused entities capable of responding quickly to market opportunities and challenges. The commercial vehicle business, with its strong market position and improving margins, will be better positioned to capitalize on India’s infrastructure growth.

JLR’s transformation strategy, including investment of £3.8 billion for next-generation electric vehicles, positions the brand for the luxury EV market. The resolution of tariff issues provides near-term relief, while the brand repositioning efforts should drive longer-term growth.

The electric vehicle strategy leverages One Tata synergies across Tata Power, Tata AutoComp, and other group companies to build a comprehensive e-mobility ecosystem. This integrated approach provides competitive advantages in charging infrastructure, battery technology, and customer experience.

Conclusion: Navigating Through Transition

Tata Motors’ Q1 FY26 results represent a challenging but not unexpected performance given the multiple headwinds facing the company. The 63% decline in net profit reflects the severity of operational challenges, particularly the impact of US trade tariffs on JLR and broader demand softness across segments.

However, the company’s strategic transformation through demerger, continued investment in electric vehicles, and focus on operational efficiency position it for potential recovery in the medium to long term. The management’s confidence in second-half performance improvement, supported by festive demand and tariff relief, provides reasons for cautious optimism.

Key success factors for recovery include successful demerger execution, effective new model launches, retention of EV market leadership, and JLR’s brand transformation success. While near-term challenges persist, Tata Motors’ diversified portfolio, strong brand equity, and strategic focus on future mobility solutions provide a foundation for eventual recovery and growth.

The company’s ability to navigate through this transitional period while maintaining profitability across segments demonstrates the underlying strength of its business fundamentals. As tariff clarity emerges and market conditions improve, Tata Motors appears well-positioned to capitalize on India’s growing automotive market and the global shift towards sustainable mobility.