PG Electroplast Ltd (PGEL) represents a compelling case study in India’s rapidly expanding Electronic Manufacturing Services (EMS) sector, yet recent quarterly results reveal both the promise and perils of operating in this dynamic industry. The company’s Q1 FY26 results demonstrated a mixed performance with revenue growth of 13.9% year-over-year but a concerning 20% decline in net profit, accompanied by significant cuts to full-year guidance that sent shares tumbling over 20% on August 8, 2025. This comprehensive analysis examines PGEL’s fundamental strengths and weaknesses, positioning the investment opportunity within the broader context of India’s manufacturing transformation and the China+1 supply chain diversification trend.

Financial Performance Analysis: Growth Momentum Meets Margin Pressure

Revenue Growth Trajectory and Seasonality Challenges

PG Electroplast’s revenue performance in Q1 FY26 showcased both the company’s underlying growth potential and vulnerability to seasonal and weather-related disruptions. Consolidated revenues reached ₹1,503.85 crores, representing a solid 13.9% year-over-year increase from ₹1,320.68 crores in Q1 FY25. However, this growth came against the backdrop of early monsoon arrivals that significantly impacted the crucial summer air conditioning season, dampening what should have been peak demand period for room air conditioners (RACs).

PG Electroplast Revenue Growth Trajectory showing strong historical growth with moderated FY26 outlook

The product business, which has emerged as PGEL’s primary growth driver, contributed 77.1% of overall revenues and demonstrated resilience with 16.7% year-over-year growth. Within this segment, the company’s strategic positioning became evident: RACs grew 15.1% despite weather challenges, washing machines surged 36.1%, while coolers declined marginally by 3.9%. This diversification across appliance categories provides some insulation against single-product dependencies, though the RAC segment’s dominance means weather patterns remain a critical factor in quarterly performance.

The company’s five-year revenue trajectory reveals remarkable transformation, growing from ₹639 crores in FY20 to ₹4,870 crores in FY25 – a compound annual growth rate of approximately 44%. This exponential growth reflects both organic capacity expansion and the broader structural shift toward outsourcing by original equipment manufacturers (OEMs) in India’s consumer durables market.

![PG Electroplast Ltd (PGEL) represents a compelling case study in India's rapidly expanding Electronic Manufacturing Services (EMS) sector, yet recent quarterly results reveal both the promise and perils of operating in this dynamic industry. The company's Q1 FY26 results demonstrated a mixed performance with revenue growth of 13.9% year-over-year but a concerning 20% decline in net profit, accompanied by significant cuts to full-year guidance that sent shares tumbling over 20% on August 8, 2025. This comprehensive analysis examines PGEL's fundamental strengths and weaknesses, positioning the investment opportunity within the broader context of India's manufacturing transformation and the China+1 supply chain diversification trend.[1][2][3]

Financial Performance Analysis: Growth Momentum Meets Margin Pressure

Revenue Growth Trajectory and Seasonality Challenges

PG Electroplast's revenue performance in Q1 FY26 showcased both the company's underlying growth potential and vulnerability to seasonal and weather-related disruptions. Consolidated revenues reached ₹1,503.85 crores, representing a solid 13.9% year-over-year increase from ₹1,320.68 crores in Q1 FY25. However, this growth came against the backdrop of early monsoon arrivals that significantly impacted the crucial summer air conditioning season, dampening what should have been peak demand period for room air conditioners (RACs).[1]](https://www.tgnns.com/wp-content/uploads/2025/08/image-3.png)

Profitability Metrics and Margin Analysis

The most concerning aspect of Q1 FY26 results was the deterioration in profitability metrics, which revealed underlying operational challenges despite top-line growth. Net profit declined 19.98% to ₹66.98 crores compared to ₹83.70 crores in the previous year, while operating profit margins compressed to 8.06% from 9.89%. This margin compression occurred despite the company’s scale advantages and suggests pricing pressures from OEM customers or inefficiencies in cost management.

EBITDA performance provided a mixed picture, with absolute EBITDA growing marginally by 3.6% to ₹139.42 crores, but EBITDA margins declining due to the revenue base expansion. The company’s gross margins have historically remained stable around 20%, indicating that the margin pressure is primarily occurring at the operational level through higher employee costs, manufacturing expenses, or administrative overheads.

Working capital management emerged as a relative strength, with the cash conversion cycle improving to approximately 68 days in recent periods, supported by payables of 80-100 days that help offset higher inventory and receivables cycles. This working capital efficiency becomes crucial given the seasonal nature of the air conditioning business and the need to build inventory ahead of peak summer demand.

Earnings Quality and Cash Flow Analysis

PG Electroplast’s cash flow profile reveals both the capital-intensive nature of the EMS business and management’s focus on growth investment. Operating cash flows turned negative at -₹76.59 crores in FY25, primarily due to working capital investments required to support rapid revenue scaling. This negative operating cash flow, while concerning from a short-term liquidity perspective, reflects the natural consequence of aggressive growth rather than underlying business deterioration.

The company’s free cash flow remained negative due to substantial capital expenditures of ₹488.2 crores in FY25, invested in new manufacturing facilities and capacity expansion. This capital intensity is characteristic of manufacturing businesses scaling rapidly, and the key metric for investors is whether these investments generate adequate returns over time.

Interest coverage remained healthy at 5.1 times, indicating comfortable debt servicing capability despite the company’s expansion phase. The strong interest coverage provides financial flexibility and suggests that current debt levels are well within management’s capability to service even during periods of operational stress.

Valuation Analysis: Premium Pricing Amid Growth Expectations

Price-to-Earnings and Peer Comparison

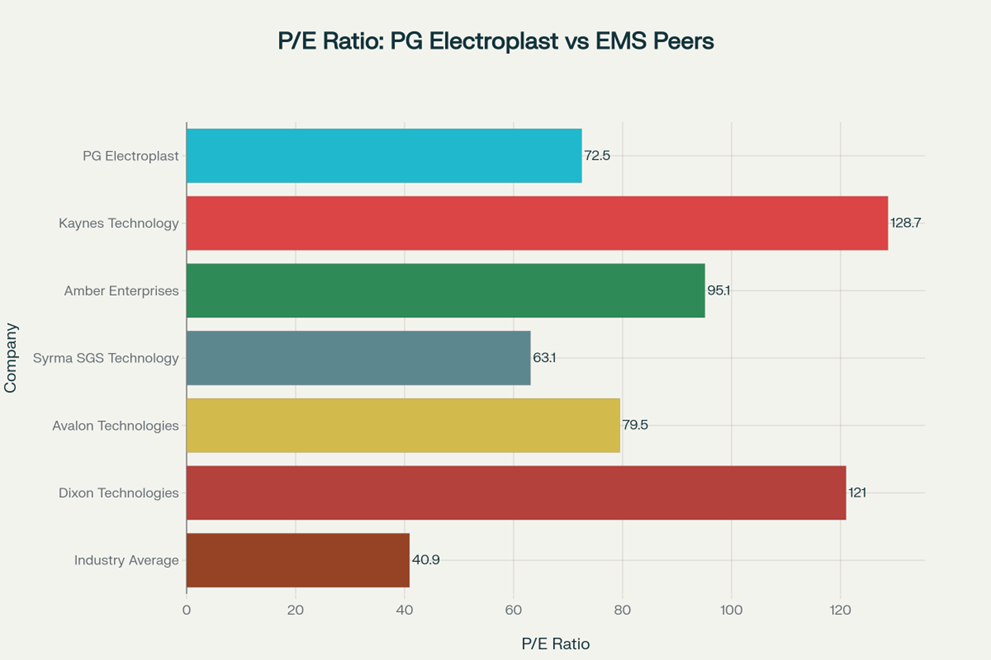

PG Electroplast’s current valuation reflects the market’s high growth expectations for the EMS sector, with the stock trading at a P/E ratio of 72.5 times based on trailing twelve-month earnings. This valuation premium becomes more nuanced when compared to EMS industry peers, where PGEL actually trades at a relative discount to several high-growth competitors.

P/E Ratio Comparison of PG Electroplast with EMS Industry Peers

The peer comparison reveals that PGEL’s 72.5x P/E ratio positions it favorably against premium EMS players like Kaynes Technology (128.7x) and Dixon Technologies (121x), while commanding a premium to Syrma SGS Technology (63.1x). This relative positioning suggests the market views PGEL as a high-quality growth story within the EMS space, though still below the valuations accorded to the sector’s most premium names.

Compared to the broader Indian electronics industry average P/E of 40.9x, PGEL trades at a significant premium that must be justified by superior growth prospects and execution capability. The company’s five-year revenue CAGR of 44% and expanding market share in key segments like air conditioners provide some fundamental support for this valuation premium.

Book Value and Asset Efficiency Metrics

PGEL’s price-to-book ratio of 20.1x appears elevated, reflecting both the asset-light nature of the EMS model and the company’s strong return generation capability. The high P/B ratio must be evaluated in context of the company’s impressive return on equity of 15% and return on capital employed of 25.2%, which justify premium valuations for efficient capital allocators.

The company’s fixed asset turnover ratio of 5.10x demonstrates efficient utilization of manufacturing assets, a critical metric in capital-intensive industries. This efficiency metric suggests that PGEL’s management has successfully scaled operations without proportionate increases in fixed asset investments, contributing to the strong return metrics.

Enterprise value-to-EBITDA of 39x and enterprise value-to-revenue of 4.1x further confirm the premium valuation, which appears justified only if the company can sustain high growth rates and improve profitability over time. The recent guidance cuts raise questions about the sustainability of growth expectations embedded in current valuations.

Dividend Policy and Shareholder Returns

PGEL maintains a conservative dividend policy with a current yield of just 0.03%, reflecting management’s focus on reinvesting cash flows into growth opportunities rather than returning capital to shareholders. The company declared a dividend of ₹0.25 per share for FY25, representing a minimal payout ratio that preserves capital for expansion investments.

This capital allocation approach aligns with the growth phase characteristics of the EMS industry, where companies must invest heavily in new facilities and capabilities to capture market share. Investors seeking dividend income would likely find more attractive opportunities elsewhere, while growth-oriented investors may appreciate the reinvestment strategy if it generates adequate returns.

Growth Potential and Competitive Positioning

Industry Tailwinds and Market Opportunity

The Indian EMS sector presents compelling structural growth drivers that benefit companies like PG Electroplast positioned at the intersection of multiple favorable trends. India’s electronics manufacturing is projected to reach ₹27.7 lakh crores by FY28, representing a robust 27% CAGR from FY23 levels. This growth trajectory is supported by increasing domestic consumption, global supply chain diversification, and government policy support through schemes like Production Linked Incentives (PLI).

Air conditioners lined up on an assembly line in a clean manufacturing facility with workers in the background

The consumer durables market, PGEL’s primary focus area, benefits from low penetration rates across key categories like air conditioners and washing machines, urbanization trends, and rising disposable incomes among India’s expanding middle class. Room air conditioner penetration remains below 10% in many Indian markets, compared to over 80% in developed economies, suggesting enormous runway for growth as affordability improves and climate patterns drive adoption.

China+1 strategies adopted by global OEMs create additional opportunities for Indian EMS providers capable of delivering quality, scale, and cost competitiveness. PG Electroplast’s established relationships with over 70+ Indian and global brands position it well to capture this supply chain diversification trend, particularly in consumer durables where the company has developed specialized capabilities.

Competitive Advantages and Market Position

PGEL has established several competitive moats that differentiate it within the fragmented EMS landscape. The company’s evolution from contract manufacturing to Original Design Manufacturing (ODM) represents a strategic shift toward higher-value services that improve customer stickiness and pricing power. ODM capabilities require significant technical expertise and customer relationships, creating barriers to entry for competitors.

The company’s manufacturing footprint across 11 facilities in Greater Noida, Ahmednagar, Bhiwadi, and Roorkee provides geographic diversification and proximity to key customers. This distributed manufacturing model reduces logistics costs and enhances service levels, while providing operational flexibility to allocate production based on demand patterns and cost optimization.

Backward integration capabilities across plastic molding, sheet metal components, PCB assemblies, and specialized air conditioning components enable PGEL to offer comprehensive solutions while capturing additional value-added steps in the manufacturing process. This vertical integration reduces dependence on external suppliers and provides better control over quality, costs, and delivery schedules.

Innovation and R&D Capabilities

PG Electroplast’s investment in design and engineering capabilities reflects the strategic importance of moving up the value chain in EMS services. The company’s focus on developing new platforms for room air conditioners and washing machines demonstrates technical competency that enhances customer relationships and pricing power.

The transition toward more complex product categories like refrigerators and potential entry into electric vehicle components represents natural extensions of PGEL’s core manufacturing competencies. These diversification efforts, while requiring significant capital investment, provide opportunities to reduce dependence on seasonal products like air conditioners and tap into faster-growing market segments.

However, the company’s R&D investments remain modest relative to technology-focused peers, suggesting limited capability for breakthrough innovations that could fundamentally alter competitive positioning. PGEL’s innovation strategy appears focused on incremental improvements and manufacturing process optimization rather than disruptive product development.

Risk Analysis and Operational Challenges

Market and Operational Risk Factors

The most immediate risk facing PG Electroplast stems from the seasonal and weather-dependent nature of its core air conditioning business, which contributed 75.2% of Q1 FY26 revenues. Early monsoon patterns in 2025 demonstrated how weather variations can significantly impact quarterly performance, as reduced summer heat decreased air conditioner demand during typically peak months.

Intense competition within the EMS sector poses ongoing pressures on pricing power and margins, as evidenced by the Q1 FY26 margin compression despite revenue growth. The entry of global players and expansion of existing competitors creates a challenging environment where cost efficiency becomes increasingly critical for maintaining market share.

Working capital requirements remain elevated due to the seasonal nature of demand patterns and the need to build inventory ahead of peak selling seasons. The company’s gross current assets averaged 150-190 days in recent periods, requiring substantial working capital financing that could strain cash flows during periods of rapid growth.

Raw material price volatility, particularly for commodities like steel, aluminum, and electronic components, creates margin pressure that may be difficult to pass through to OEM customers who maintain significant bargaining power. The company’s limited pricing power in commodity-like manufacturing services makes it vulnerable to input cost inflation.

Financial and Liquidity Risk Assessment

PG Electroplast’s financial risk profile appears manageable despite recent performance challenges, with a conservative debt-to-equity ratio of 0.11x that provides significant financial flexibility. The company’s low leverage creates capacity for additional borrowing to fund growth investments, though management must balance growth aspirations with financial prudence.

Interest coverage of 5.1x provides comfortable debt servicing capability, while cash balances of ₹812 crores offer substantial liquidity cushion for operations and investment requirements. This strong balance sheet position becomes particularly valuable during challenging operating periods or economic downturns that could pressure cash flows.

The company’s dependence on external financing for growth initiatives creates exposure to interest rate fluctuations and credit market conditions. Rising interest rates could increase financing costs for both PGEL and its customers, potentially impacting demand for big-ticket appliances that often require consumer financing.

Bank limit utilization averaged 62% over recent periods, indicating moderate reliance on credit facilities while maintaining unused capacity for operational flexibility. The availability of unutilized credit lines provides working capital support during seasonal peaks or unexpected business challenges.

Regulatory and Policy Risk Considerations

Government policy changes related to import duties, environmental regulations, or energy efficiency standards could significantly impact PG Electroplast’s operations and cost structure. The company benefits from current PLI schemes that provide production incentives, but policy changes could alter these favorable conditions.

Environmental regulations around refrigerant usage in air conditioners and energy efficiency requirements create both challenges and opportunities for EMS providers. Companies capable of adapting to new technical standards may gain competitive advantages, while those unable to meet evolving requirements face market share risks.

Labor regulations and wage inflation in key manufacturing states like Uttar Pradesh and Maharashtra could increase operational costs, particularly given the labor-intensive nature of appliance assembly. The company’s geographic diversification provides some mitigation, but systemic labor cost increases would pressure margins.

Trade policy changes affecting component imports or finished product exports could alter the competitive dynamics within the EMS sector. The company’s reliance on imported components for certain products creates vulnerability to tariff changes or supply chain disruptions.

Recent Developments and Management Outlook

Q1 FY26 Results and Guidance Revision

The most significant recent development was management’s substantial revision of FY26 financial guidance, which sparked the sharp share price decline in August 2025. Revenue guidance was reduced from ₹6,345 crores to ₹5,700-5,800 crores, representing a cut from 30% expected growth to 17-19% growth. Similarly, net profit guidance was revised down from ₹405 crores to ₹300-310 crores, reducing expected profit growth from 39% to just 3-7%.

This guidance revision reflects both the immediate impact of weather-related demand challenges and management’s more conservative outlook on recovery prospects for the remainder of FY26. The company indicated limited confidence in recovering lost Q1 growth during subsequent quarters, suggesting structural rather than temporary demand challenges.

Management commentary emphasized continued long-term growth prospects while acknowledging near-term headwinds from early monsoon patterns and inventory buildup across the consumer durables industry. The measured tone reflected realistic assessment of operating conditions while maintaining commitment to capacity expansion plans.

Capital Expenditure Plans and Facility Expansion

Despite near-term challenges, PG Electroplast continues aggressive capacity expansion with ₹700-750 crores of planned capital expenditure for FY26. This substantial investment program includes new facilities for plastic components and coolers in Rajasthan, a campus in Greater Noida for washing machines, refrigerator manufacturing in South India, and expanded AC capacity in West India.

The company’s commitment to doubling gross block to ₹22 billion over the next two years demonstrates confidence in long-term demand prospects despite current challenges. This expansion strategy positions PGEL to capture market share gains as the EMS sector continues consolidating around scale players with comprehensive capabilities.

Revenue contributions from new capacity are expected to commence in Q2-Q3 FY27, creating a lag between capital investment and financial returns that could pressure near-term cash flows and returns. Investors must evaluate whether this investment timing aligns with demand recovery expectations and competitive positioning objectives.

Investment Thesis and Strategic Outlook

Bullish Investment Case

PG Electroplast presents a compelling long-term growth story anchored in India’s structural transformation toward domestic manufacturing and the global shift in electronics supply chains away from China-centric models. The company’s established market position in high-growth consumer durables categories, combined with proven execution capabilities in scaling operations, provides a foundation for sustained value creation.

The EMS sector’s expected 33% CAGR through FY27 creates a favorable operating environment for well-positioned players like PGEL that have developed comprehensive manufacturing capabilities and customer relationships. The company’s diversification across multiple appliance categories and geographic markets provides some protection against single-product or regional risks.

Management’s focus on capital efficiency metrics like return on capital employed (25.2%) and asset turnover ratios (5.1x) demonstrates financial discipline that should support long-term value creation even during periods of rapid expansion. The company’s conservative balance sheet provides financial flexibility to navigate challenging periods while investing for growth.

PG Electroplast’s progression toward Original Design Manufacturing (ODM) services represents a strategic evolution that should improve profitability and customer relationships over time. ODM capabilities create higher switching costs for customers and enable better pricing power compared to pure contract manufacturing services.

Bearish Investment Considerations

The significant revision in FY26 guidance raises questions about management’s forecasting capabilities and the predictability of the business model during transitional periods. The magnitude of the guidance cut suggests either inadequate initial planning or structural challenges that may persist beyond the current fiscal year.

Intense competition within the EMS sector creates ongoing margin pressures that may limit pricing power despite scale advantages. The commoditization risk in contract manufacturing services could prevent PGEL from capturing the full value of its growth investments, particularly if customers maintain strong bargaining power.

Seasonal demand patterns and weather dependency in the core air conditioning business create quarterly volatility that may not appeal to investors seeking predictable returns. The concentration risk in cyclical consumer durables limits diversification benefits compared to technology-focused EMS providers.

Working capital intensity and negative cash flow generation during growth phases create financial risks if economic conditions deteriorate or access to external financing becomes constrained. The company’s dependence on continuous capital investment to maintain competitive position limits financial flexibility during challenging periods.

Valuation Assessment and Price Targets

Current valuations appear stretched relative to near-term earnings prospects, with the 72.5x P/E ratio requiring sustained high growth rates and margin expansion to justify investor returns. The recent guidance cuts suggest these growth expectations may be optimistic given current operating realities.

Analyst consensus price targets average ₹1,035 with a range of ₹756-1,250, implying potential upside of 40-78% from current levels around ₹589. However, these targets were likely set before the recent guidance revisions and may require adjustment based on updated growth expectations.

A fair value estimate based on peer multiples and growth prospects suggests a target P/E range of 45-60x, which would imply share prices of ₹450-600 based on revised FY26 earnings expectations. This valuation range reflects both the premium quality of PGEL’s market position and the realistic growth constraints revealed in recent quarters.

Conclusion and Investment Recommendation

PG Electroplast Ltd represents a high-quality participant in India’s transformative EMS sector growth story, yet current valuations and recent operational challenges require careful consideration by potential investors. The company’s strong market positions in consumer durables, conservative balance sheet, and experienced management team provide a solid foundation for long-term value creation within the structural growth themes of domestic manufacturing and supply chain diversification.

However, the significant guidance cuts in Q1 FY26 and margin pressures demonstrate the near-term challenges facing the business as it navigates intense competition, seasonal demand patterns, and execution risks associated with rapid capacity expansion. Current valuations appear optimistic relative to revised growth expectations, suggesting limited upside potential until the company demonstrates improved operational performance and more predictable earnings generation.

For long-term investors with high risk tolerance, PG Electroplast offers exposure to compelling secular trends in Indian manufacturing with the potential for significant returns if management successfully executes its expansion strategy and margin improvement initiatives. However, the stock appears more suitable for experienced investors capable of tolerating quarterly volatility and valuation fluctuations rather than conservative income-focused portfolios.

The investment recommendation is HOLD for existing shareholders with a positive long-term outlook on Indian EMS sector growth, while new investors should consider waiting for more attractive entry points below ₹500 or evidence of improved operational execution before initiating positions. The company’s fundamental strengths warrant continued monitoring, but current risk-reward dynamics favor patience over aggressive accumulation.