The Reserve Bank of India (RBI) has once again taken significant action against non-banking finance companies (NBFCs) involved in the microfinance sector, proving that some players in the industry have failed to learn from past mistakes. This time, the central bank’s move, announced on Friday, echoes the events of the 2010 Andhra Pradesh microfinance crisis, with certain well-known names being penalized for similar infractions. The proactive regulatory measures highlight the ongoing challenges in maintaining ethical lending practices within the microfinance industry.

A Recurring Issue: The Microfinance Crisis Revisited

In 2010, the microfinance industry faced a major crisis in Andhra Pradesh, largely due to exorbitant interest rates and aggressive debt recovery practices. Despite the lessons from that period, some Microfinance Institutions (MFIs) continue to fall short in adhering to regulatory guidelines. The RBI has been consistent in giving ample warnings and sufficient time for these institutions to rectify their policies, especially those related to high-interest rates. However, the latest round of penalties against NBFC-MFIs shows that certain players failed to act responsibly.

Manappuram Finance Shares Drop: The Fallout of RBI’s Action

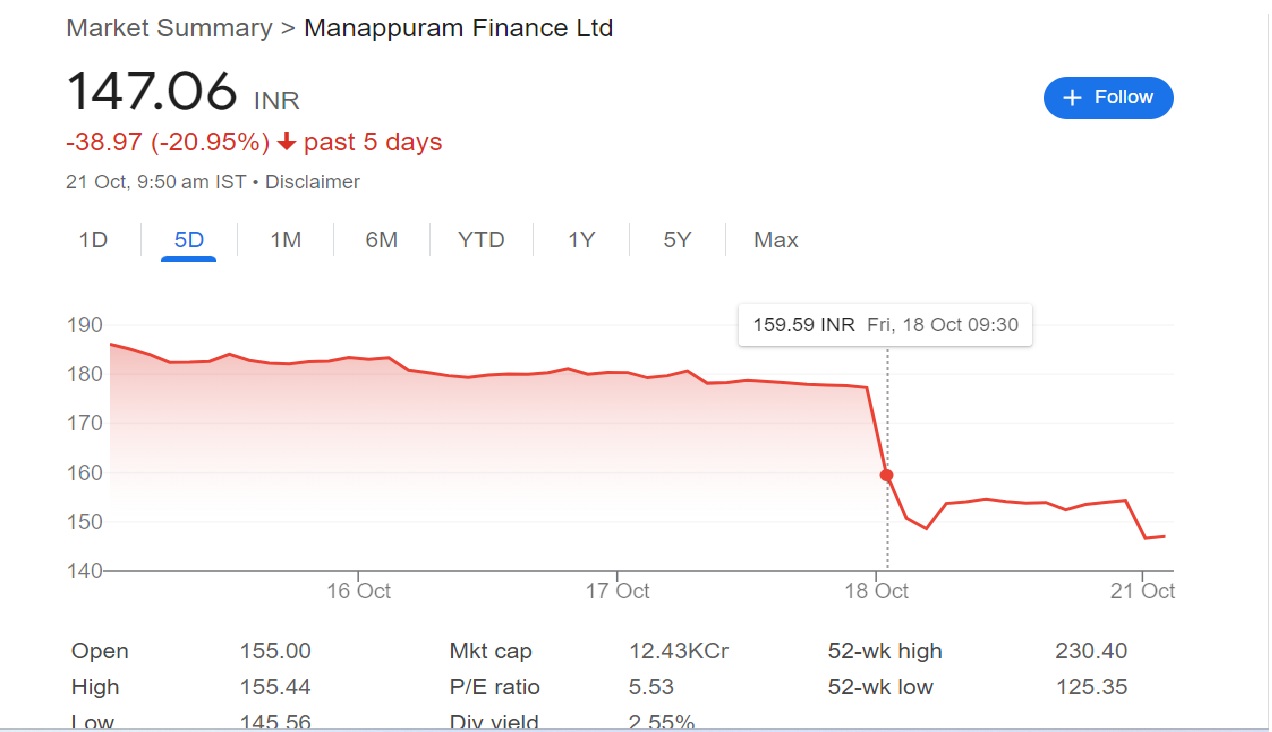

The impact of the RBI’s decision was immediately felt in the market, with shares of Manappuram Finance plummeting by nearly 17%. Manappuram Finance’s subsidiary, Asirvad Micro Finance, was ordered to halt all loan sanctioning and disbursement operations, effective October 21. This ban came in light of supervisory concerns regarding Asirvad’s lending practices. The RBI’s concerns were primarily focused on the pricing strategies employed by Asirvad, particularly the excessively high weighted average lending rate and the wide interest spread over its cost of funds. These issues were deemed non-compliant with RBI regulations and the Fair Practices Code.

The Extent of the Ban: How It Affects Manappuram Finance

Asirvad Micro Finance is a significant part of Manappuram Finance’s business portfolio. As of June 30, 2024, Asirvad’s assets under management (AUM) stood at ₹12,300 crore, including ₹1,200 crore from gold loan portfolios. Not only does Asirvad contribute 27% to the consolidated AUM of Manappuram Finance, but it also plays a vital role in the company’s overall profitability. The ban impacts 515 gold loan branches managed by Asirvad, further deepening the operational challenges for the company.

Manappuram Finance’s shares fell sharply, hitting a low of ₹147.50 on the Bombay Stock Exchange (BSE) following the RBI’s decision. Asirvad’s contribution to Manappuram’s consolidated profits has been significant, accounting for 21% of the profit after tax (PAT) in FY24 and 15% in FY23. The overall net worth of Asirvad stands at ₹2,250 crore, while Manappuram’s standalone net worth was ₹10,700 crore as of June 30.

Supervisory Concerns: What Triggered the Ban?

The RBI’s stringent action against Asirvad was a result of its failure to comply with key regulatory frameworks. The central bank had raised red flags over the company’s pricing methods, particularly the high-interest rates charged to borrowers. The weighted average lending rate was found to be too high, and the interest spread over the cost of funds was deemed unjustifiable. These issues violate both the RBI’s regulations and the Fair Practices Code, which are designed to ensure that borrowers are not subjected to exploitative lending terms.

In addition to Asirvad, other NBFCs, including Arohan Financial Services, DMI Finance, and Navi Finserv, also faced similar bans from the RBI. These actions serve as a clear signal from the central bank that it will not tolerate non-compliance with its lending guidelines, particularly in sectors like microfinance that serve vulnerable and low-income populations.

Asirvad’s Response: A Commitment to Corrective Action

In response to the RBI’s decision, the board of Asirvad Micro Finance has expressed its commitment to complying with the regulatory directives. The company has assured its stakeholders that it will undertake a thorough review of its governance structure, risk management practices, and regulatory compliance systems. Additionally, Asirvad’s board has promised to implement corrective measures within a set timeframe, aimed at addressing the supervisory concerns raised by the RBI.

This proactive approach from Asirvad is essential not only to restore its lending operations but also to regain the trust of the market and its customers. The company has vowed to closely monitor its practices and ensure they align with the central bank’s guidelines moving forward.

What’s Next for the Microfinance Sector?

The recent action by the RBI against multiple NBFC-MFIs raises important questions about the sustainability of the current lending models in the microfinance sector. With rising scrutiny from the central bank, MFIs will need to place a greater emphasis on ethical lending practices, transparent pricing, and adherence to regulatory frameworks. Failure to do so could result in more stringent penalties and potentially long-term damage to their reputations and financial standing.

Moreover, the market volatility experienced by companies like Manappuram Finance highlights the risks associated with non-compliance. Investors are likely to be wary of companies that do not adhere to the RBI’s strict guidelines, leading to reduced stock values and investor confidence.

Conclusion: The Need for Responsible Lending Practices

The RBI’s decisive action against erring NBFCs in the microfinance sector serves as a stark reminder that past mistakes should not be repeated. The 2010 microfinance crisis was a wake-up call for the industry, but it seems some players have not fully absorbed the lessons. Moving forward, it is imperative for MFIs to adopt responsible lending practices that prioritize the well-being of their borrowers while ensuring regulatory compliance.

By enforcing stricter regulations and taking swift action against non-compliance, the RBI is safeguarding the integrity of the financial system and protecting the interests of vulnerable borrowers. For the microfinance industry, this is a clear call to evolve and adapt to a more ethical and sustainable way of operating.