In the dynamic landscape of the Open Credit Enablement network OCEN 4.0 will do Escrow based Loan Recovery or Loan collections, lenders venturing into the realm of new short-tenure small-ticket products, targeted at untapped borrower segments, must prioritize efficient loan collections. The ability to collect payments promptly and seamlessly not only ensures consistent cash flow but also fosters the sustained growth and viability of their lending enterprise. However, for those lacking the requisite experience, comprehension, and resources to execute effective collections, the prospect of serving these innovative products may seem daunting and may not yield optimal outcomes.

Evolving Lending Dynamics: The Crucial Role of Specialized Roles

As a strategic response to these challenges, OCEN 4.0 introduces a range of specialized roles within the lending ecosystem, augmenting the traditional roles of lenders and loan agents. These specialized roles encompass KYC partners, derived data partners, disbursement partners, and collections partners. This strategic distribution of responsibilities serves to alleviate the burden on lenders, empowering them to concentrate on their core lending functions. This approach further permits lenders to establish collaborative relationships with various partners along the lending value-chain, thereby enhancing their capacity to effectively offer the new products.

Optimizing Collections through Strategic Partnerships

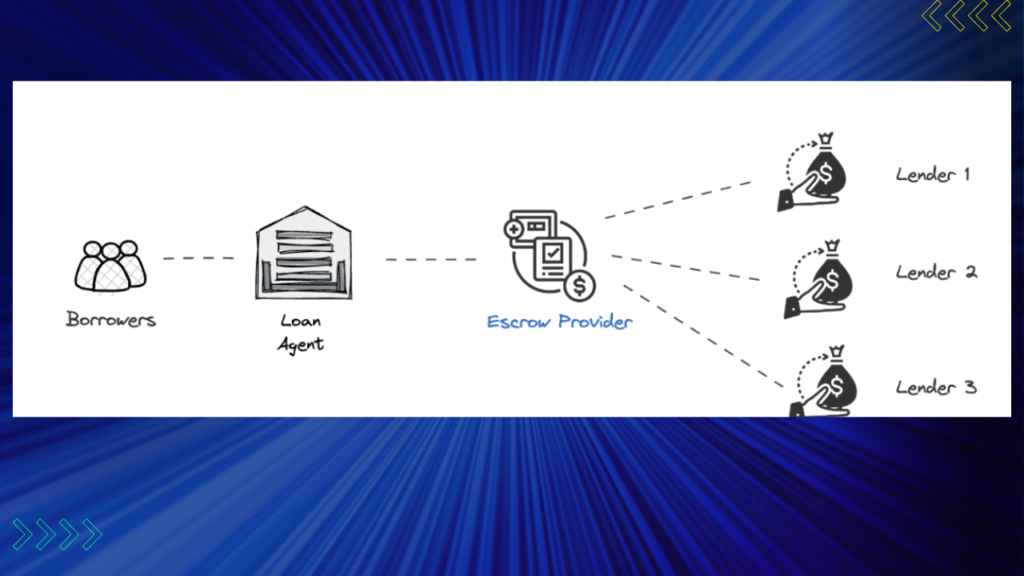

OCEN 4.0’s operational philosophy centers around empowering “local partners with remote lenders.” This paradigm shift facilitates service providers with existing customer bases to assume the role of loan agents, extending credit products to their clientele, who in turn act as borrowers. The product delivery is orchestrated by a network of participants, encompassing lenders, KYC partners, disbursement partners, collections partners, and others.

This model often positions loan agents as the primary source of income for borrowers, underscoring their critical role in the collections process. In scenarios where loan agents serve as income sources for borrowers, OCEN 4.0 leverages an escrow-based repayment system. This innovative approach mitigates collections-related risks for lenders and instills a high degree of confidence in the efficiency of the collections network.

Escrow-Based Repayments: Enhancing Collections Control

Consider the case of PO-based financing, exemplified by GeM Sahay. In this model, a supplier (borrower) secures a loan based on an approved Purchase Order (PO). Upon the completion of goods or services delivery, GeM disburses the funds, channeling them into an escrow account. Within this framework, an escrow rule-engine calculates the lender’s share, facilitating payouts that allocate a portion to the lender and the remaining balance to the supplier.

A Closer Look at Escrow-Based Repayments in OCEN 4.0

In OCEN 4.0’s auction-based model, loan agents collaborate with Escrow-as-a-Service providers (EAASPs). Unlike the traditional approach, where individual lenders engage with EAASPs, this model ensures a single transparent rule-engine manages fund disbursements for all borrowers within the network. Consequently, lenders gain access to a collections-ready network, streamlining their participation.

Here, EAASP represents both the Escrow-as-a-Service provider and a Trustee, combining their roles. The trustee, supported by SEBI, undertakes the responsibility of executing instructions on behalf of the lender within the escrow system.

Streamlined Flow: The Escrow-Based Repayment Process

Within the OCEN 4.0 network, a typical escrow-based flow unfolds as follows:

- Inclusion of EAASP/Trustee: The loan agent integrates the EAASP/trustee as a participant in the product network, alongside lenders and other stakeholders. When a potential borrower secures a loan, the EAASP provides a virtual account (VA) where the loan agent deposits funds, bypassing the borrower’s conventional bank account.

- Funds Management: The funds within the VA are allocated for loan payouts, ensuring streamlined repayment processes.

- Timely Notifications and Updates: Upon disbursal of a new loan, the lender notifies the loan agent, who subsequently updates the EAASP’s escrow rule-engine to reflect the specifics of that borrower’s arrangement. This entails creating a new entry or updating an existing one if pending payouts are involved.

- Payment Monitoring: As the loan agent deposits funds into the VA, the EAASP monitors ongoing repayments and collaborates with the lender to confirm due repayments.

- Efficient Fund Distribution: Leveraging the EAASP rule-engine, funds are distributed among the lender, borrower, loan agent, and EAASP (including applicable fees). Each transaction is meticulously recorded, and borrower loan balances are duly updated.

The Dynamics of Collections Control: Escrow-Based Flow Variability

The efficacy of collections control within the escrow-based flow of OCEN 4.0 hinges on a multitude of factors, giving rise to various possible scenarios. The adaptability of this system ensures its applicability across diverse borrower segments and lending contexts.

In conclusion, OCEN 4.0’s pioneering approach to specialized roles and escrow-based repayments introduces a paradigm shift in loan collection dynamics. Lenders embracing this innovative ecosystem stand to benefit from enhanced efficiency, reduced risk, and the confidence to venture into unexplored lending frontiers._

Scenario: Loan Repayment on the Payout Date

The ideal scenario, as demonstrated in the successful implementation at GeM Sahay, involves loan repayments coinciding with the payout date. This alignment streamlines the repayment process and minimizes complexities. Flexibility in loan tenure remains crucial to accommodating varying borrower needs while maintaining this synchronicity.

Scenario Multiple Loans Running and Payout Not Enough to Pay All Lenders (Payout Mapped to an Invoice/PO)

In situations where a borrower has multiple concurrent loans and the payout falls short of covering all lenders, a strategic approach is vital. Payouts should be directed to the lender associated with the specific invoice or Purchase Order (PO) that triggered the loan. This targeted disbursement ensures that the lender linked to the relevant transaction receives their due share, optimizing fund distribution.

Scenario: Multiple Loans Running and Payout Not Enough to Pay All Lenders (Payout NOT Mapped to an Invoice/PO)

Navigating scenarios where payouts are not directly mapped to specific invoices or POs requires a predefined and well-structured logic. This complexity demands careful consideration of how funds are split and which lenders are prioritized. Establishing clear guidelines for fund allocation in such cases is essential to uphold fairness and transparency.

Embracing Versatility for Optimal Collections Control

The efficacy of loan collections within the OCEN 4.0 ecosystem hinges on adaptable strategies that address various repayment scenarios. As OCEN 4.0 paves the way for innovative lending dynamics, the collaboration between lenders, loan agents, and specialized partners, alongside the careful orchestration of escrow-based repayments, creates a dynamic and efficient collections landscape.

In conclusion, the ability to navigate diverse repayment scenarios is a hallmark of successful lenders in the OCEN 4.0 era. By understanding and proactively addressing the complexities that can arise, lenders can optimize collections, foster borrower trust, and contribute to the sustainable growth of the lending ecosystem._