![Trump's 50% Tariff Bomb Rocks Indian Markets: BSE, CDSL Share Analysis and Strategic Outlook The Indian financial markets face unprecedented volatility as US President Donald Trump's escalated tariff regime reaches a punitive 50% on Indian goods, triggering widespread concerns about economic growth, export competitiveness, and market stability. This comprehensive analysis examines the multifaceted impact on India's stock exchanges, with particular focus on BSE Limited and Central Depository Services Limited (CDSL), while also evaluating the competitive dynamics following NSDL's recent market debut. Market Carnage: The Immediate Impact of Trump's Tariff Escalation Indian benchmark indices experienced significant pressure on August 7, 2025, as investors grappled with the implications of Trump's tariff announcement. The BSE Sensex fell 387 points (0.48%) to 80,156, while the Nifty 50 declined 119 points (0.49%) to 24,454. This market reaction reflects deep-seated concerns about the potential economic ramifications of what analysts are calling an effective "trade embargo" on Indian exports.[1][2][3] Sector-wise vulnerability to Trump's 50% tariffs showing textiles and gems & jewelry as the most exposed industries The tariff escalation represents a dramatic shift in US-India trade relations, with the cumulative 50% duty rate now exceeding levies on Chinese goods by 20 percentage points. This punitive measure, ostensibly targeting India's continued purchases of Russian crude oil, threatens to fundamentally alter the competitive landscape for Indian exporters across multiple sectors.[4][5] Morgan Stanley's analysis reveals the stark reality facing the Indian economy. Under the most severe scenario, where all goods face the full 50% tariff, India could experience a direct GDP impact of 0.6% and an indirect impact of 0.6%, culminating in a total economic drag of 1.2%. Even under a more moderate scenario targeting only non-exempt goods, the cumulative impact could reach 0.8% of GDP growth.[6][7] Sector-Specific Vulnerabilities and Market Disruptions The tariff impact varies dramatically across sectors, with export-dependent industries bearing the brunt of the policy shift. Textiles emerge as the most vulnerable sector, with approximately 63% of total exports destined for US markets potentially facing the full tariff burden. The gems and jewelry industry, accounting for 33% of exports to the US, faces similar challenges, while leather goods, chemicals, and auto components also confront significant headwinds.[8][3][9] Foreign Institutional Investor (FII) selling has intensified the market pressure, with net outflows reaching ₹4,999 crore on August 6 alone. Month-to-date FII selling has accelerated to ₹10,954 crore, reflecting international investors' concerns about tariff-related earnings impacts. This capital flight compounds domestic market stress and creates additional pressure on export-oriented companies.[10][11][12] BSE Limited: Navigating Turbulence with Strategic Leadership Changes Despite the broader market turmoil, BSE Limited demonstrates operational resilience, though its share price reflects the prevailing uncertainty. Trading at ₹2,387 with a modest 0.13% decline, BSE's relative stability amid the market downturn underscores its position as a critical market infrastructure provider largely insulated from direct export exposure.[13][14] The Bombay Stock Exchange building in Mumbai displaying real-time stock ticker and financial news visuals. Strategic Appointment Strengthens Cybersecurity Leadership BSE announced a significant leadership addition with the appointment of Shri Fal Ghancha as Joint Chief Information Security Officer, effective October 1, 2025. This strategic hire reflects BSE's commitment to strengthening its technological infrastructure and cybersecurity capabilities during a period of heightened market volatility.[15] Ghancha brings extensive expertise in technology and cybersecurity leadership, with a robust track record across asset management, insurance, and industrial sectors. His qualifications include certification as a Certified Chief Information Security Officer (CCISO), Certified Ethical Hacker, and expertise in regulatory compliance frameworks including SEBI and ISO 27001 standards. This appointment positions BSE to better manage technological risks and enhance its operational resilience.[15] Financial comparison between BSE Limited and NSDL showing BSE's superior scale and profitability metrics Financial Performance and Market Position BSE's financial metrics demonstrate the exchange's robust performance despite challenging market conditions. With a market capitalization of ₹97,410 crore and revenue of ₹3,212 crore in FY25, BSE significantly outperforms newer market entrants in terms of scale and profitability. The company's Return on Equity (ROE) of 36% reflects efficient capital utilization, though investors should note the elevated P/E ratio of 73.13, indicating premium valuations.[13][14] The company's dividend policy remains conservative, with a yield of 0.25%, reflecting management's focus on reinvestment for growth rather than immediate shareholder returns. This strategy appears prudent given the current market uncertainties and the need for continued technological investments.[13] CDSL vs NSDL: The Battle for Depository Dominance Intensifies The recent listing of National Securities Depository Limited (NSDL) on August 6, 2025, has introduced a new competitive dynamic in India's concentrated depository services market. NSDL's debut at ₹880 per share, representing a 10% premium over its ₹800 issue price, signals investor confidence in the depository services sector despite broader market headwinds.[16][17][18] Market Share Dynamics and Competitive Positioning CDSL maintains a commanding position in retail investor accounts, managing 15.3 crore demat accounts compared to NSDL's 3.95 crore. This four-fold advantage reflects CDSL's successful penetration of the retail trading boom, particularly through partnerships with fintech brokers and discount trading platforms.[19][20][21] However, NSDL demonstrates strength in institutional custody services, managing ₹464 lakh crore in assets under custody compared to CDSL's ₹71 lakh crore. This institutional focus provides NSDL with higher-value, stickier revenue streams, though with lower overall profitability margins compared to CDSL's retail-focused model.[21][19] Financial Performance Comparison CDSL consistently outperforms NSDL in dividend payouts, demonstrating stronger shareholder returns over the past five years CDSL's financial superiority becomes apparent when examining profitability metrics. With a net profit margin of 48.6% compared to NSDL's 22.35%, CDSL demonstrates superior operational efficiency. This margin advantage reflects the scalability of CDSL's retail-focused business model, where high-volume, low-value transactions generate substantial cumulative profits.[19][20] Revenue growth patterns also favor CDSL, with a three-year compound annual growth rate of 39.5% compared to NSDL's 17.9%. This growth differential reflects the explosive expansion in retail trading activity post-COVID, which disproportionately benefited CDSL's business model.[19] Dividend Track Record Analysis CDSL's dividend history showcases consistent shareholder value creation, with progressive increases from ₹9 per share (90%) in 2021 to ₹22 per share (220%) in 2024. This trajectory reflects not only strong cash generation but also management confidence in sustained business growth.[22][19] Conversely, NSDL's dividend history appears more modest, with payments of ₹1 per share in both 2023 and 2024, rising to ₹2 per share in 2025. While NSDL's dividend policy may evolve post-listing, the current disparity highlights CDSL's superior cash generation capabilities and more aggressive shareholder return policies.[18] Economic Implications and Growth Forecasts Morgan Stanley's Revised Growth Projections Despite the tariff headwinds, Morgan Stanley maintains a cautiously optimistic outlook for India's medium-term growth trajectory. The investment bank has modestly upgraded India's growth forecast to 6.2% for FY26 and 6.5% for FY27, reflecting confidence in domestic demand resilience and policy support measures.[23][6][24] The upgrade, primarily attributed to easing US-China trade tensions and improved external demand prospects, suggests that India's growth story extends beyond bilateral trade relationships. Morgan Stanley emphasizes that domestic demand will remain the primary growth engine, supported by government policy initiatives including monetary easing and capital expenditure-focused fiscal policy.[6][24] Crude Oil Price Dynamics and Energy Security The tariff dispute has broader implications for India's energy security, given Trump's explicit targeting of Russian oil imports. Crude oil prices have shown volatility, with Brent crude trading around $67-68 per barrel. India's dependence on oil imports (approximately 85% of consumption) makes the country particularly vulnerable to supply disruptions or price volatility resulting from geopolitical tensions.[25][26][27] The potential for supply chain rerouting and increased energy costs could create inflationary pressures, complicating the Reserve Bank of India's monetary policy decisions. Any significant disruption to Russian oil supplies could impact India's current account balance and currency stability. Sector-Wise Impact Assessment and Investment Implications Most Vulnerable Sectors Export-dependent industries face the most immediate challenges from the tariff escalation. Textiles, gems and jewelry, leather goods, and marine products – sectors with significant US market exposure – are likely to experience margin compression and potential market share losses. Companies in these sectors may need to rapidly diversify their export markets or recalibrate their cost structures to maintain competitiveness.[3][9] Chemical companies face particular challenges, with organic chemicals exports attracting an additional 54% duty under the new tariff structure. This burden extends beyond direct exporters to companies in the broader chemical value chain, potentially affecting input costs across multiple industries.[9] Resilient Domestic-Focused Sectors Conversely, domestically-focused sectors appear relatively insulated from direct tariff impacts. Banking and financial services, including BSE and CDSL, derive revenues primarily from domestic market activities. Similarly, sectors such as cement, consumer goods, healthcare, real estate, and telecommunications should maintain their growth trajectories, supported by India's robust domestic consumption patterns.[28] Information technology services and pharmaceuticals currently enjoy exemptions from the additional tariffs, providing some relief for these critical export sectors. However, investors should monitor potential policy changes that could extend tariff coverage to these industries.[4][5] Strategic Recommendations and Risk Management Portfolio Diversification Strategies Given the heightened uncertainty surrounding trade policy, investors should consider rebalancing portfolios toward domestic consumption themes. Financial services companies, including exchanges like BSE and depository services like CDSL, offer exposure to India's growing capital market participation without direct export vulnerability. The infrastructure and market structure companies benefit from India's long-term financialization trends, regardless of short-term trade disruptions. CDSL's dominant position in retail demat services positions it to benefit from continued retail investor growth, while BSE's exchange infrastructure remains essential to market functioning. Long-Term Growth Catalysts Despite near-term challenges, India's structural growth drivers remain intact. The continued expansion of retail investor participation, digital financial services adoption, and corporate governance improvements should support sustained growth in market infrastructure companies. The recent NSDL listing creates additional investment options in the depository space, though investors should carefully evaluate the competitive dynamics and growth trajectories of both CDSL and NSDL. CDSL's superior profitability metrics and dividend track record may appeal to income-focused investors, while NSDL's institutional client base offers potential stability and growth in high-value custody services. Conclusion: Navigating Uncertainty with Strategic Focus Trump's 50% tariff escalation represents a significant challenge for India's export-dependent economy, with potential GDP impacts ranging from 0.8% to 1.2% depending on the final policy implementation. The immediate market reaction reflects investor concerns about earnings impacts and competitive positioning across multiple sectors.[6][7] However, companies with strong domestic market positions, including BSE Limited and CDSL, demonstrate resilience amid the broader market turbulence. BSE's strategic leadership appointments and CDSL's superior financial performance metrics suggest these market infrastructure companies remain well-positioned for long-term growth, regardless of](https://www.tgnns.com/wp-content/uploads/2025/08/Trumps-50-Tariff-Effect-BSE-CDSL-Share-Analysis-and-Strategic-Outlook.png)

The Indian financial markets face unprecedented volatility as US President Donald Trump’s escalated tariff regime reaches a punitive 50% on Indian goods, triggering widespread concerns about economic growth, export competitiveness, and market stability. This comprehensive analysis examines the multifaceted impact on India’s stock exchanges, with particular focus on BSE Limited and Central Depository Services Limited (CDSL), while also evaluating the competitive dynamics following NSDL’s recent market debut.

Market Carnage: The Immediate Impact of Trump’s Tariff Escalation

Indian benchmark indices experienced significant pressure on August 7, 2025, as investors grappled with the implications of Trump’s tariff announcement. The BSE Sensex fell 387 points (0.48%) to 80,156, while the Nifty 50 declined 119 points (0.49%) to 24,454. This market reaction reflects deep-seated concerns about the potential economic ramifications of what analysts are calling an effective “trade embargo” on Indian exports.

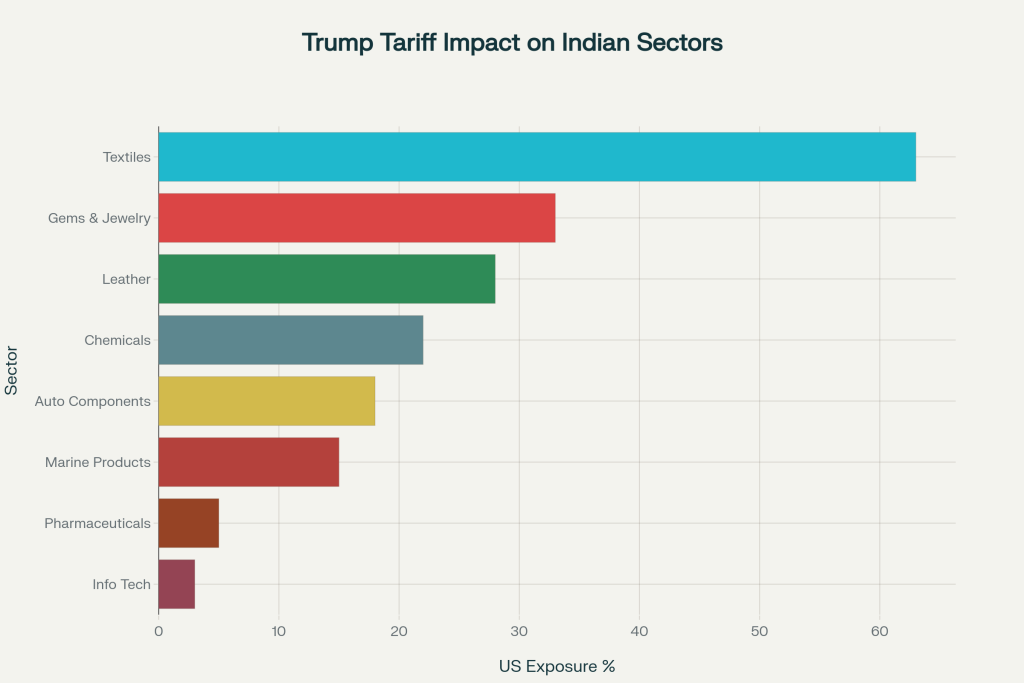

Sector-wise vulnerability to Trump’s 50% tariffs showing textiles and gems & jewelry as the most exposed industries

The tariff escalation represents a dramatic shift in US-India trade relations, with the cumulative 50% duty rate now exceeding levies on Chinese goods by 20 percentage points. This punitive measure, ostensibly targeting India’s continued purchases of Russian crude oil, threatens to fundamentally alter the competitive landscape for Indian exporters across multiple sectors.

Morgan Stanley’s analysis reveals the stark reality facing the Indian economy. Under the most severe scenario, where all goods face the full 50% tariff, India could experience a direct GDP impact of 0.6% and an indirect impact of 0.6%, culminating in a total economic drag of 1.2%. Even under a more moderate scenario targeting only non-exempt goods, the cumulative impact could reach 0.8% of GDP growth.

Sector-Specific Vulnerabilities and Market Disruptions

The tariff impact varies dramatically across sectors, with export-dependent industries bearing the brunt of the policy shift. Textiles emerge as the most vulnerable sector, with approximately 63% of total exports destined for US markets potentially facing the full tariff burden. The gems and jewelry industry, accounting for 33% of exports to the US, faces similar challenges, while leather goods, chemicals, and auto components also confront significant headwinds.

Foreign Institutional Investor (FII) selling has intensified the market pressure, with net outflows reaching ₹4,999 crore on August 6 alone. Month-to-date FII selling has accelerated to ₹10,954 crore, reflecting international investors’ concerns about tariff-related earnings impacts. This capital flight compounds domestic market stress and creates additional pressure on export-oriented companies.

BSE Limited: Navigating Turbulence with Strategic Leadership Changes

Despite the broader market turmoil, BSE Limited demonstrates operational resilience, though its share price reflects the prevailing uncertainty. Trading at ₹2,387 with a modest 0.13% decline, BSE’s relative stability amid the market downturn underscores its position as a critical market infrastructure provider largely insulated from direct export exposure.

The Bombay Stock Exchange building in Mumbai displaying real-time stock ticker and financial news visuals

Strategic Appointment Strengthens Cybersecurity Leadership

BSE announced a significant leadership addition with the appointment of Shri Fal Ghancha as Joint Chief Information Security Officer, effective October 1, 2025. This strategic hire reflects BSE’s commitment to strengthening its technological infrastructure and cybersecurity capabilities during a period of heightened market volatility.

Ghancha brings extensive expertise in technology and cybersecurity leadership, with a robust track record across asset management, insurance, and industrial sectors. His qualifications include certification as a Certified Chief Information Security Officer (CCISO), Certified Ethical Hacker, and expertise in regulatory compliance frameworks including SEBI and ISO 27001 standards. This appointment positions BSE to better manage technological risks and enhance its operational resilience.

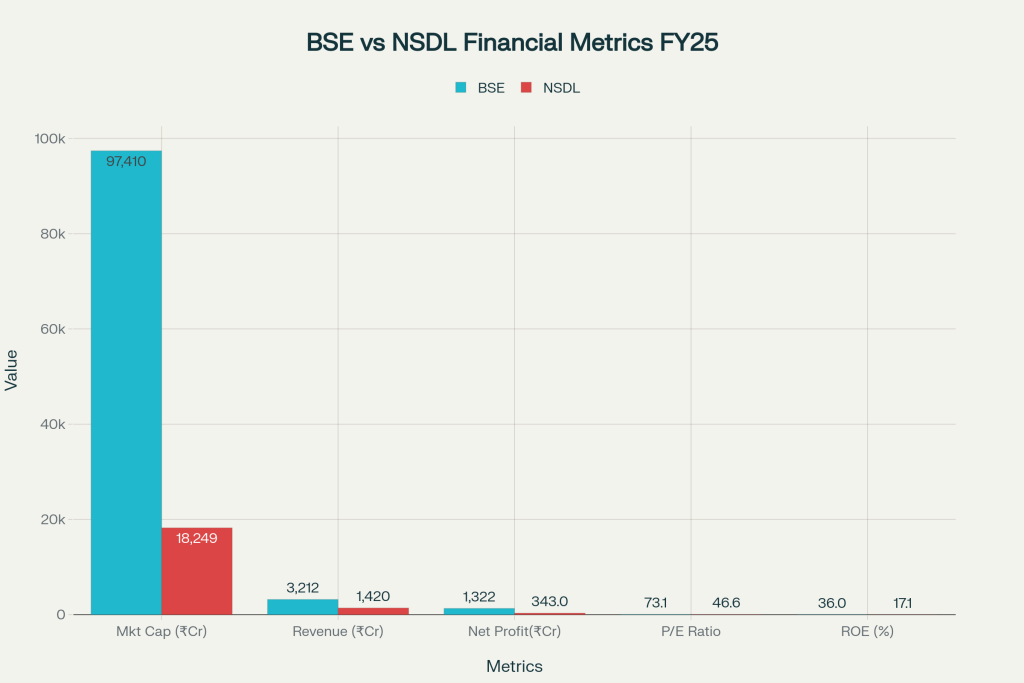

Financial comparison between BSE Limited and NSDL showing BSE’s superior scale and profitability metrics

Financial Performance and Market Position

BSE’s financial metrics demonstrate the exchange’s robust performance despite challenging market conditions. With a market capitalization of ₹97,410 crore and revenue of ₹3,212 crore in FY25, BSE significantly outperforms newer market entrants in terms of scale and profitability. The company’s Return on Equity (ROE) of 36% reflects efficient capital utilization, though investors should note the elevated P/E ratio of 73.13, indicating premium valuations.

The company’s dividend policy remains conservative, with a yield of 0.25%, reflecting management’s focus on reinvestment for growth rather than immediate shareholder returns. This strategy appears prudent given the current market uncertainties and the need for continued technological investments.

CDSL vs NSDL: The Battle for Depository Dominance Intensifies

The recent listing of National Securities Depository Limited (NSDL) on August 6, 2025, has introduced a new competitive dynamic in India’s concentrated depository services market. NSDL’s debut at ₹880 per share, representing a 10% premium over its ₹800 issue price, signals investor confidence in the depository services sector despite broader market headwinds.

Market Share Dynamics and Competitive Positioning

CDSL maintains a commanding position in retail investor accounts, managing 15.3 crore demat accounts compared to NSDL’s 3.95 crore. This four-fold advantage reflects CDSL’s successful penetration of the retail trading boom, particularly through partnerships with fintech brokers and discount trading platforms.

However, NSDL demonstrates strength in institutional custody services, managing ₹464 lakh crore in assets under custody compared to CDSL’s ₹71 lakh crore. This institutional focus provides NSDL with higher-value, stickier revenue streams, though with lower overall profitability margins compared to CDSL’s retail-focused model.

Financial Performance Comparison

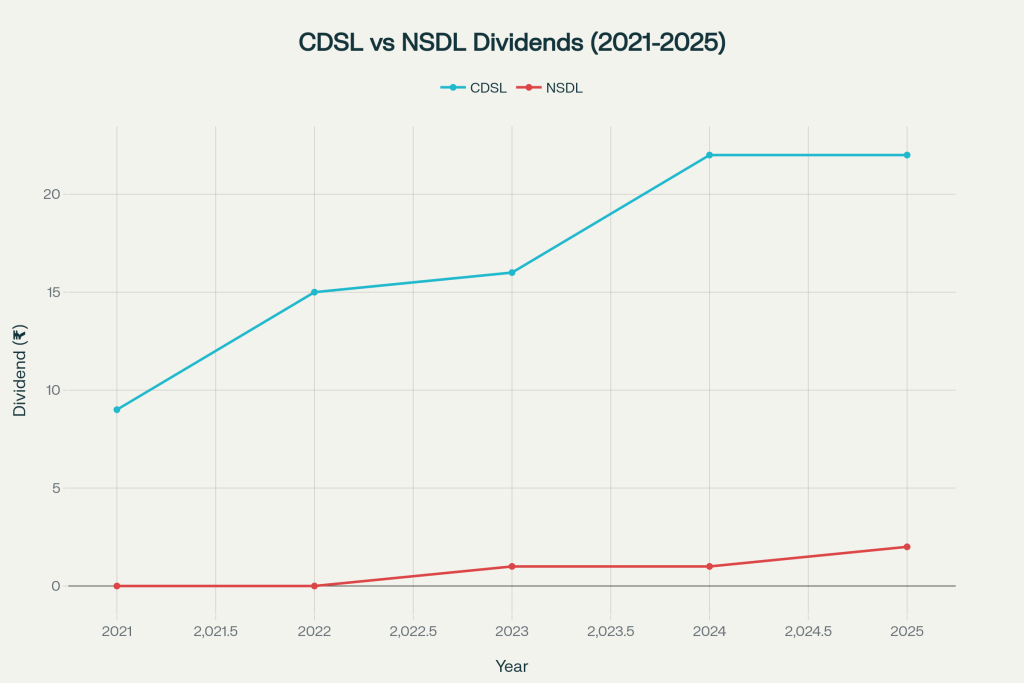

CDSL consistently outperforms NSDL in dividend payouts, demonstrating stronger shareholder returns over the past five years

CDSL’s financial superiority becomes apparent when examining profitability metrics. With a net profit margin of 48.6% compared to NSDL’s 22.35%, CDSL demonstrates superior operational efficiency. This margin advantage reflects the scalability of CDSL’s retail-focused business model, where high-volume, low-value transactions generate substantial cumulative profits.

Revenue growth patterns also favor CDSL, with a three-year compound annual growth rate of 39.5% compared to NSDL’s 17.9%. This growth differential reflects the explosive expansion in retail trading activity post-COVID, which disproportionately benefited CDSL’s business model.

Dividend Track Record Analysis

CDSL’s dividend history showcases consistent shareholder value creation, with progressive increases from ₹9 per share (90%) in 2021 to ₹22 per share (220%) in 2024. This trajectory reflects not only strong cash generation but also management confidence in sustained business growth.

Conversely, NSDL’s dividend history appears more modest, with payments of ₹1 per share in both 2023 and 2024, rising to ₹2 per share in 2025. While NSDL’s dividend policy may evolve post-listing, the current disparity highlights CDSL’s superior cash generation capabilities and more aggressive shareholder return policies.

Economic Implications and Growth Forecasts

Morgan Stanley’s Revised Growth Projections

Despite the tariff headwinds, Morgan Stanley maintains a cautiously optimistic outlook for India’s medium-term growth trajectory. The investment bank has modestly upgraded India’s growth forecast to 6.2% for FY26 and 6.5% for FY27, reflecting confidence in domestic demand resilience and policy support measures.

The upgrade, primarily attributed to easing US-China trade tensions and improved external demand prospects, suggests that India’s growth story extends beyond bilateral trade relationships. Morgan Stanley emphasizes that domestic demand will remain the primary growth engine, supported by government policy initiatives including monetary easing and capital expenditure-focused fiscal policy.

Crude Oil Price Dynamics and Energy Security

The tariff dispute has broader implications for India’s energy security, given Trump’s explicit targeting of Russian oil imports. Crude oil prices have shown volatility, with Brent crude trading around $67-68 per barrel. India’s dependence on oil imports (approximately 85% of consumption) makes the country particularly vulnerable to supply disruptions or price volatility resulting from geopolitical tensions.

The potential for supply chain rerouting and increased energy costs could create inflationary pressures, complicating the Reserve Bank of India’s monetary policy decisions. Any significant disruption to Russian oil supplies could impact India’s current account balance and currency stability.

Sector-Wise Impact Assessment and Investment Implications

Most Vulnerable Sectors

Export-dependent industries face the most immediate challenges from the tariff escalation. Textiles, gems and jewelry, leather goods, and marine products – sectors with significant US market exposure – are likely to experience margin compression and potential market share losses. Companies in these sectors may need to rapidly diversify their export markets or recalibrate their cost structures to maintain competitiveness.

Chemical companies face particular challenges, with organic chemicals exports attracting an additional 54% duty under the new tariff structure. This burden extends beyond direct exporters to companies in the broader chemical value chain, potentially affecting input costs across multiple industries.

Resilient Domestic-Focused Sectors

Conversely, domestically-focused sectors appear relatively insulated from direct tariff impacts. Banking and financial services, including BSE and CDSL, derive revenues primarily from domestic market activities. Similarly, sectors such as cement, consumer goods, healthcare, real estate, and telecommunications should maintain their growth trajectories, supported by India’s robust domestic consumption patterns.

Information technology services and pharmaceuticals currently enjoy exemptions from the additional tariffs, providing some relief for these critical export sectors. However, investors should monitor potential policy changes that could extend tariff coverage to these industries.

Strategic Recommendations and Risk Management

Portfolio Diversification Strategies

Given the heightened uncertainty surrounding trade policy, investors should consider rebalancing portfolios toward domestic consumption themes. Financial services companies, including exchanges like BSE and depository services like CDSL, offer exposure to India’s growing capital market participation without direct export vulnerability.

The infrastructure and market structure companies benefit from India’s long-term financialization trends, regardless of short-term trade disruptions. CDSL’s dominant position in retail demat services positions it to benefit from continued retail investor growth, while BSE’s exchange infrastructure remains essential to market functioning.

Long-Term Growth Catalysts

Despite near-term challenges, India’s structural growth drivers remain intact. The continued expansion of retail investor participation, digital financial services adoption, and corporate governance improvements should support sustained growth in market infrastructure companies.

The recent NSDL listing creates additional investment options in the depository space, though investors should carefully evaluate the competitive dynamics and growth trajectories of both CDSL and NSDL. CDSL’s superior profitability metrics and dividend track record may appeal to income-focused investors, while NSDL’s institutional client base offers potential stability and growth in high-value custody services.

Conclusion: Navigating Uncertainty with Strategic Focus

Trump’s 50% tariff escalation represents a significant challenge for India’s export-dependent economy, with potential GDP impacts ranging from 0.8% to 1.2% depending on the final policy implementation. The immediate market reaction reflects investor concerns about earnings impacts and competitive positioning across multiple sectors.

However, companies with strong domestic market positions, including BSE Limited and CDSL, demonstrate resilience amid the broader market turbulence. BSE’s strategic leadership appointments and CDSL’s superior financial performance metrics suggest these market infrastructure companies remain well-positioned for long-term growth, regardless of short-term trade disruptions.

Growth trends in the Indian stock market: number of issues vs amount raised from 1989-90 to 2021-22

The competitive dynamics in India’s depository services market will intensify following NSDL’s public listing, creating opportunities for improved service offerings and operational efficiencies. Investors should monitor the execution capabilities and strategic initiatives of both CDSL and NSDL as they compete for market share in India’s expanding capital markets ecosystem.

While the tariff situation introduces near-term volatility and uncertainty, India’s underlying economic fundamentals and domestic growth drivers provide a foundation for sustained expansion. Market participants should focus on companies with strong domestic market positions, robust cash generation capabilities, and strategic advantages that transcend bilateral trade relationships. The current market correction may present attractive entry opportunities for long-term investors willing to navigate short-term volatility in pursuit of India’s compelling structural growth story.