Executive Summary

The Trade Receivables Electronic Discounting System (TReDS) has emerged as a cornerstone policy framework for addressing India’s persistent MSME liquidity crisis, with the Union Budget 2026-27 (presented February 1, 2026) maintaining strategic emphasis on working capital access rather than introducing granular TReDS-specific allocations. Understanding TReDS in the context of Budget 2026-27 is essential for financial journalists, MSME stakeholders, and platform operators, as the system bridges the critical funding gap affecting enterprises that contribute 30% to India’s GDP and 45% to exports.

This report synthesizes official government announcements, RBI policy guidance, and industry intelligence to provide you with actionable intelligence for financial reporting, content strategy, and stakeholder analysis.

Part I: TReDS System Architecture & Policy Foundation

What TReDS Is: Technical Overview

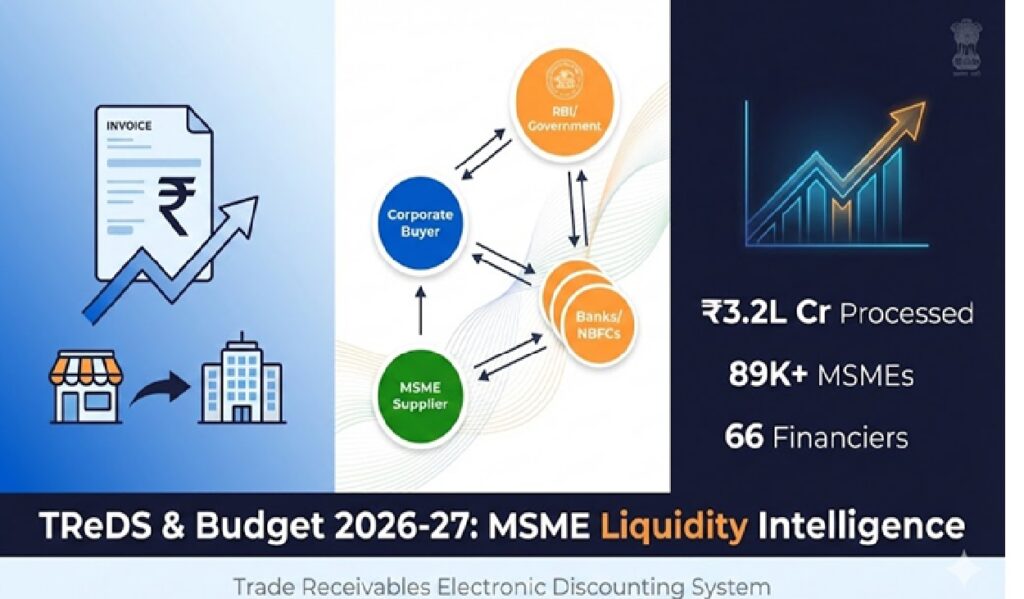

TReDS is an RBI-regulated digital platform enabling non-recourse factoring of MSME invoices through competitive bidding by multiple financiers. The system operates through a standardized electronic workflow:

- Invoice Upload: MSME seller raises invoice on TReDS platform after supply to large corporate buyer

- Buyer Acceptance: Corporate/PSU validates and accepts the invoice electronically

- Competitive Bidding: Multiple banks and NBFCs bid to discount the invoice

- Instant Settlement: Seller receives funds (typically T+1 basis) at competitively determined rates

- Non-Recourse Protection: MSME bears zero default risk; financier has no recourse against seller

The system is legally structured as an electronic equivalent to negotiable instruments under the NI Act 1881 and Factoring Regulation Act 2011, providing regulatory clarity and enforceability.

Current Adoption Landscape (February 2026)

Despite mandate and growing institutional adoption, TReDS remains underutilized relative to India’s ₹30 lakh crore MSME credit gap.

Part II: Budget 2025-26 Context & MSME Credit Architecture

Before analyzing 2026-27 expectations, understanding the precedent from Budget 2025-26 (February 1, 2025) provides essential context.

Budget 2025-26 MSME Framework: What Was Announced

While no standalone TReDS announcement appeared in the Budget 2025-26 speech, the government outlined supporting credit architecture:

| Initiative | Specification | Expected Impact |

|---|---|---|

| Classification Revision | MSME investment/turnover limits raised 2.5x and 2x respectively | Allows smaller firms to access enterprise-tier schemes |

| Credit Guarantee Enhancement – Micro/Small | ₹5 crore → ₹10 crore | ₹1.5 lakh crore additional credit over 5 years |

| Startup Guarantees | ₹10 crore → ₹20 crore; 1% fee for 27 focus sectors | Atmanirbhar Bharat alignment |

| Exporter MSME Guarantees | Term loans up to ₹20 crore with guarantee cover | Export growth under geopolitical headwinds |

| Credit Cards for Micro Enterprises | ₹5 lakh limit; 10 lakh issuance target in Year 1 | Direct access to working capital |

| Export Promotion Mission (para 86) | “Cross-border factoring support” and export credit facilitation | Closest reference to TReDS-like mechanisms |

The Export Promotion Mission reference to “cross-border factoring support” represents indirect acknowledgment of electronic invoice discounting but does not mandate or enhance domestic TReDS.

Part III: Budget 2026-27: Emerging Policy Direction

What Budget 2026-27 Announced (February 1, 2026)

As of February 1, 2026, Finance Minister Nirmala Sitharaman presented Budget 2026-27 with the following MSME-relevant framework:

Key Announcements & TReDS Relevance:

- Working Capital & Liquidity Focus: Industry expectations centered on faster payment cycles and reduced DSO (Days Sales Outstanding), not new TReDS mandates.

- No Explicit TReDS Enhancement: Unlike some stakeholder pre-Budget recommendations (mandatory CPSE onboarding completion, penal interest for chronic defaulters, digital arbitration for payment disputes), the Budget 2026-27 speech does not introduce fresh TReDS-specific policy changes.

- Complementary Credit Infrastructure: The budget maintains emphasis on credit guarantees, working capital cards, and export promotion—all of which create demand for TReDS financing by improving corporate buyer participation.

- Payment Cycle Acceleration: Industry expectations for “faster cash-flow cycles for smaller suppliers” align with TReDS’ core value proposition of T+1 settlement, though no Budget directive mandates further acceleration.

Part IV: Why Budget 2026-27 Reflects TReDS as Established Policy, Not New Initiative

Strategic Reasoning: Policy Maturation vs. Policy Launch

The absence of explicit Budget 2026-27 TReDS announcements reflects deliberate policy positioning:

1. Compliance Completion Cycle

The March 31, 2025 mandatory onboarding deadline for ₹250+ crore corporates and CPSEs created a structural inflection point. By February 2026 (Budget announcement date), compliance tracking has begun, and enforcement mechanisms (RoC reporting obligations under MCA directive) are operational. The Budget’s focus shifts from mandate announcement to implementation verification.

2. RBI’s Autonomous Role

The Reserve Bank of India, not Parliament via Budget, implements TReDS regulatory guidance. RBI’s October 2025 Standing Advisory Committee recommended wider TReDS adoption and cash-flow-based lending, affirming central bank ownership of platform evolution independent of fiscal allocation.

3. Factoring as Priority Sector

RBI classified factoring transactions under Priority Sector Lending in 2015, directing bank credit toward TReDS automatically without fresh Budget earmarks. This structural inclusion ensures capital flows to the platform without annual appropriations.

4. Platform Economics Are Self-Sustaining

Unlike infrastructure or export schemes requiring government subsidy, TReDS operates on transaction fees levied on buyers/financiers. No public funds required for platform continuity, explaining its absence from fiscal allocation discussions.

Part V: Critical Data Points for Financial Reporting

MSME Liquidity Challenge (The Problem TReDS Solves)

| Metric | Finding | Impact |

|---|---|---|

| Average Receivable Cycle | 90–120 days | Working capital blocked for quarter |

| MSME Credit Gap | ₹30 lakh crore (SIDBI estimate) | Underfinancing vs. loan demand |

| TReDS Adoption Gap | Remains low among buyers despite mandate | Implementation-to-compliance ratio weak |

| Payment Default Frequency | Chronic defaults from state governments unaddressed | Legislative reform needed beyond TReDS |

| Geopolitical Export Risk | US tariff uncertainty depressing export-dependent MSME credit demand | TReDS demand slowing despite platform readiness |

Budget 2026-27’s Indirect TReDS Support Mechanisms

While no direct TReDS allocation, these Budget provisions structurally increase TReDS utilization:

1. Enhanced Guarantee Schemes → Higher Corporate Buyer Participation

- Improved access to ₹20 crore for exporter MSMEs increases corporate buyer creditworthiness, making their invoices more bankable on TReDS

- Financiers more willing to discount invoices from better-guaranteed supply chains

2. Export Promotion Mission’s Cross-Border Factoring → International TReDS Linkage

- “Cross-border factoring support” suggests future integration of domestic TReDS invoices into global supply chain finance platforms

- Telecom, electronics, chemicals exporters (high tariff-risk sectors) can access TReDS + cross-border facilities for overseas receivables

3. Credit Cards for Micro Enterprises → Competitive Pressure on Traditional Factoring

- ₹5 lakh credit cards for 10 lakh Udyam-registered micro enterprises offer working capital alternative

- Lower-friction entry point than TReDS for smallest tier; mid-market MSMEs default to TReDS for higher invoice values

Part VI: Pre-Budget Industry Recommendations (What Didn’t Get Announced)

Understanding the gap between stakeholder expectations and Budget reality is critical for strategic reporting. Industry bodies sought:

| Recommendation | Status in Budget 2026-27 | Strategic Implication |

|---|---|---|

| Mandatory CPSE TReDS Onboarding Completion | Not mentioned; assumes March 2025 deadline enforced | Compliance verification role falls to RoC, not Finance Ministry |

| Penal Interest for Chronic Defaulters | Not mentioned | Payment delays to MSMEs remain unpenalized; remedy via litigation only |

| Digital Arbitration for Payment Disputes | Not mentioned | MSME Samadhaan portal emphasis instead |

| Interest Subvention on Factoring | Not proposed | No subsidy to lower TReDS discount rates |

| E-Marketplace-Based Invoice Discounting | Not mentioned; GeM-TReDS integration ongoing | Slower rollout than recommended |

Interpretation: Budget prioritizes broad credit guarantees over TReDS-specific incentives, betting on market-driven adoption post-compliance deadline.

Part VII: RBI Policy Momentum & Financial Sector Autonomy

RBI’s October 2025 Policy Stance (Pre-Budget Signal)

The RBI Standing Advisory Committee (October 27, 2025) on MSME credit explicitly endorsed TReDS before the Budget was framed:

“Cash-flow based lending and adoption of digital solutions like TReDS can improve credit linkage for MSMEs. The committee emphasized addressing information asymmetry, financial literacy gaps, and delayed payments, and underscored the need to promote wider adoption of digital solutions like TReDS.”

Significance: The central bank’s public endorsement, independent of Budget announcements, signals TReDS is a monetary policy priority, not a fiscal one. Expect RBI guidance circulars and regulatory incentives (e.g., higher priority sector weightage, lower capital requirements for TReDS-backing banks) to drive platform growth post-Budget.

Part VIII: Implementation Gaps & Emerging Constraints

Why TReDS Hasn’t Reached Potential Despite Policy Support

Despite 8+ years of government backing, TReDS utilization remains constrained:

1. Buyer Adoption Lag

- Mandatory onboarding deadline (March 31, 2025) passed; enforcement mechanisms unclear

- Companies prioritize bank credit, credit cards, DPOs over invoice discounting

- No commercial incentive for large corporates to accelerate MSME payment cycles

2. Quality of Receivables

- As corporate buyers onboard, invoice quality variance increases, raising financier risk

- Defaults spike in economic downturns; TReDS volumes decline pro-cyclically

3. Integration Gaps

- GSTN, Udyam, MCA database integrations “ongoing” but not seamless; verification still requires manual touchpoints

- Delays offset T+1 settlement advantage

4. Geopolitical Headwinds

- US tariff uncertainty (Trump administration, 2026) depressing export-MSME credit demand

- Working capital needs shift from expansion (TReDS use case) to survival (bank credit/credit cards)

Part IX: Budget 2026-27 Numerical Allocations & MSME Credit Framework

Quantified MSME Support (2026-27 Budget Outlay)

| Program | Allocation/Impact | Relevance to TReDS |

|---|---|---|

| Credit Guarantee for Micro/Small | ₹1.5 lakh crore additional credit (5-year target) | Larger buyer base improves invoice volume on TReDS |

| Exporter MSME Guarantees | Term loans up to ₹20 crore | High-value invoices from exporters feed TReDS |

| Credit Cards for Micro Enterprises | 10 lakh cards issued (Year 1 target) | Competitive alternative to TReDS for smallest tier |

| Fund of Funds for Startups | ₹10,000 crore fresh contribution | Tech platforms (including TReDS operators) eligible for venture capital |

| Export Promotion Mission | ₹5,000 crore annual outlay (5-year commitment) | Cross-border factoring integration with TReDS |

Aggregate MSME Fiscal Support (2026-27): While not precisely itemized in the Budget, combined credit guarantee expansions, export support, and skill schemes exceed ₹50,000 crore in commitments over the medium term—creating structural demand for TReDS.

Part X: Forward-Looking Strategic Intelligence for MSME Stakeholders

What to Monitor Post-Budget 2026-27

- RoC Compliance Reporting (March-June 2026)

- Expect first comprehensive dataset on large corporate TReDS onboarding compliance

- Track announcement of penalties for non-compliance companies

- CPSE Payment Cycle Acceleration

- Monitor government e-Marketplace (GeM) integration with TReDS

- Measure DSO (Days Sales Outstanding) for government vendor payments

- Financier Participation Expansion

- Watch for new bank and NBFC onboarding on TReDS platforms

- Track reduced spreads/discount rates as competition intensifies

- Invoice Volume Growth

- C2TReDS, M1xchange quarterly disclosures will reveal adoption trajectory

- Compare growth rates across platforms to assess competitive dynamics

- Policy Evolution Signals

- June 2026 Monetary Policy Committee (RBI) guidance on factoring/TReDS weightage

- Mid-year policy announcements from MSME Ministry on implementation gaps

Conclusion: TReDS in the Budget 2026-27 Era

Budget 2026-27 represents policy maturation over policy launch: TReDS transitions from announcement phase (2016-2024) through mandatory compliance phase (2025) into operational embedding phase (2026 onward). The absence of explicit TReDS announcements reflects this evolution.

The Budget’s emphasis on credit guarantee expansion, export facilitation, and payment cycle acceleration structurally increases TReDS utilization without requiring fiscal allocation to the platform itself. This represents India’s emerging preference for market-driven platform economics over government-subsidized financial schemes.

For financial publishers and MSME stakeholders: Track implementation metrics, not announcements. The real story of TReDS’ impact on MSME liquidity in 2026-27 will unfold through compliance reporting, payment cycle data, and financier participation expansion—not through Budget rhetoric.