Oil and Natural Gas Corporation (ONGC) delivered a mixed but resilient performance in the first quarter of FY2025-26, reporting results that largely met market expectations despite significant headwinds from lower crude oil prices and production challenges. The company’s consolidated net profit rose 18.2% year-over-year to ₹11,554 crores, while standalone operations faced pressure with a 10.2% decline in net profit, reflecting the complex dynamics facing India’s largest oil and gas explorer.

Financial Performance Overview

ONGC’s Q1 FY26 results showcase the company’s ability to navigate challenging market conditions while maintaining operational efficiency. On a standalone basis, the company reported gross revenue of ₹32,003 crores, representing a 9.3% year-over-year decline from ₹35,266 crores in Q1 FY25. This revenue contraction was anticipated by market analysts, who had estimated revenues of approximately ₹31,500 crores, making ONGC’s actual performance marginally better than expectations by 1.6%.

ONGC’s quarterly financial performance trends over the last 5 quarters showing revenue, profit, and earnings per share

The company’s net profit performance on a standalone basis reached ₹8,024 crores, down from ₹8,938 crores in the corresponding quarter of the previous year. However, this result significantly exceeded market estimates of ₹7,500 crores, representing a positive variance of 7.0%. The consolidated performance was notably stronger, with net profit increasing 18.2% year-over-year to ₹11,554 crores, driven by improved performance from subsidiary operations.

ONGC Q1 FY26 market estimates vs actual results comparison showing performance against analyst expectations

Operating Metrics and Margins

ONGC’s operating performance demonstrated remarkable resilience despite revenue pressures. The company achieved an operating margin of 37.1% during the quarter, reflecting efficient cost management and operational optimization. On a quarter-over-quarter basis, the company’s EBITDA increased by 23% to ₹17,185.28 crores, with margins expanding from 39.9% in Q4 FY25 to 53.7% in Q1 FY26.

Earnings per share (EPS) for the quarter stood at ₹6.38, marginally below the market estimate of ₹6.47 but representing a sequential improvement from ₹5.13 in Q4 FY25. This EPS performance reflects the company’s ability to maintain profitability per share despite revenue challenges.

Production Performance and Operational Achievements

Hydrocarbon Production Trends

ONGC’s production performance in Q1 FY26 showed mixed results across different segments. Standalone crude oil production increased by 1.2% year-over-year to 4.683 million metric tonnes (MMT), compared to 4.629 MMT in Q1 FY25. This production growth is particularly noteworthy given the mature nature of many of ONGC’s fields and represents successful reservoir management and enhanced oil recovery techniques.

Natural gas production experienced a slight decline, with standalone production at 4.846 billion cubic meters (BCM) compared to 4.863 BCM in the previous year, representing a marginal 0.3% decrease. The overall production from joint venture operations showed more significant pressure, with crude oil production from JVs declining to 0.306 MMT from 0.353 MMT in the previous year.

Exploration Successes and New Discoveries

Large industrial oil and gas storage tank and pipeline facility representing refinery infrastructure

ONGC made significant strides in exploration during Q1 FY26, declaring two new offshore discoveries that demonstrate the company’s continued exploration capabilities. The Vajramani discovery in the Mumbai offshore basin represents a new prospect discovery in the western part of OALP-III Block MB-OSHP-2018/1. Exploratory well MBS181HNA-1 flowed oil at 2,122 barrels per day and gas at 83,120 cubic meters per day during testing.

The Suryamani discovery in OALP Block MB-OSHP-2020/2 marked the first discovery in Basal Clastics in this block, with the well flowing 413 barrels per day of oil and 15,132 cubic meters per day of gas. These discoveries are particularly significant as they open new areas for exploration and demonstrate ONGC’s technical capabilities in challenging offshore environments.

Pricing Environment and Market Dynamics

Impact of Crude Oil Price Volatility

The primary challenge facing ONGC during Q1 FY26 was the significant decline in crude oil realizations. The company’s net realization from nominated fields averaged $66.13 per barrel, down 20.4% from $83.05 per barrel in Q1 FY25. In rupee terms, realizations declined even more sharply by 18.3% to ₹5,658 per barrel from ₹6,928 per barrel in the previous year.

Joint venture crude oil realizations also faced pressure, declining 15.8% to $67.87 per barrel from $80.64 per barrel year-over-year. This pricing environment reflected broader global oil market dynamics, including concerns about economic growth, OPEC+ production policies, and geopolitical factors affecting supply and demand balances.

Gas Pricing Dynamics and New Well Premium

ONGC benefited from improved gas pricing structures during the quarter. The price for nomination gas increased modestly by 2.2% to $6.64 per MMBtu from $6.50 per MMBtu in the previous year. More significantly, the company capitalized on new well gas premium pricing, with such gas commanding $8.26 per MMBtu compared to the regular APM gas price.

Revenue from new well gas reached ₹1,703 crores during the quarter, delivering an additional ₹333 crores compared to standard APM gas pricing. This premium pricing mechanism incentivizes enhanced production from new wells and supports ONGC’s continued investment in field development and enhanced recovery techniques.nsearchives.nseindia

Industry Context and Competitive Landscape

Upstream Sector Performance

The Indian upstream oil and gas sector faced broad-based challenges during Q1 FY26, with most major producers experiencing similar pressures from lower crude oil prices. Oil India Limited, ONGC’s peer company, reported a marginal 1.5% increase in consolidated net profit to ₹2,046.5 crores despite a 6.4% decline in revenue. The sector’s performance was influenced by a sharp 22% drop in crude price realizations, from $84.89 per barrel to $66.20 per barrel year-over-year.

Industry analysts from Nuvama forecasted that upstream producers including ONGC would witness weaker quarters amid softer crude prices, production declines, and structural gas headwinds. However, ONGC’s performance relative to these expectations demonstrates the company’s operational resilience and cost management capabilities.

Refining and Marketing Sector Strength

In contrast to upstream challenges, India’s oil marketing companies (OMCs) experienced significant margin expansion during Q1 FY26. Companies like HPCL, BPCL, and IOCL reported EBITDA surges of 52-72% due to improved auto fuel marketing margins and better refining spreads. This divergence in performance across the oil and gas value chain reflects the different ways that crude oil price movements affect various segments of the industry.

Strategic Initiatives and Future Outlook

Renewable Energy Transformation

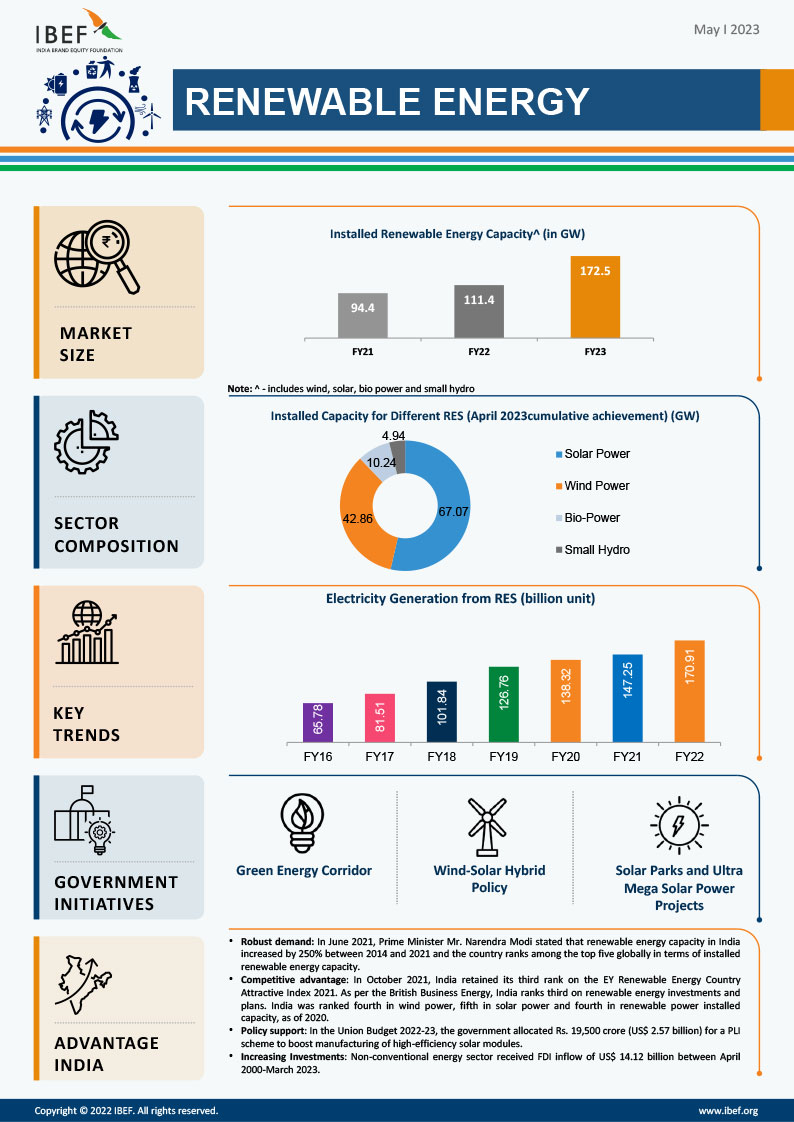

India’s renewable energy sector overview showing installed capacity, sector composition, electricity generation trends, and government initiatives as of May 2023

ONGC is undertaking an ambitious transformation toward renewable energy, planning to invest ₹1 trillion by 2030 to build a renewable portfolio of 10 gigawatts. During Q1 FY26, the company’s board approved a ₹4,963.06 crore investment in a 0.6 GW renewable energy project, comprising equal parts solar and wind power.

The company has already made significant progress in this transition, completing the acquisition of PTC Energy for ₹925 crores, which added 288 MW of operational wind power capacity. Through its joint venture ONGC NTPC Green Private Limited with NTPC Green Energy, the company has also acquired Ayana Renewable Power, which operates solar and wind assets valued at $2.3 billion.

Enhanced Oil Recovery and Technology Deployment

ONGC is implementing advanced technologies to maximize recovery from existing fields. The company commissioned its largest Alkaline Surfactant Polymer (ASP) plant at the Ahmedabad Asset, with a capacity of 2,100 cubic meters per day, designed to enhance oil recovery efficiency through chemical enhanced oil recovery (CEOR) schemes.

The company also commissioned its first onshore Multiphase Pumping (MPP) System at Ahmedabad, representing part of a comprehensive plan to merge installations for cost efficiency, enhanced sales revenue, and operational optimization.

Exploration Strategy and International Partnerships

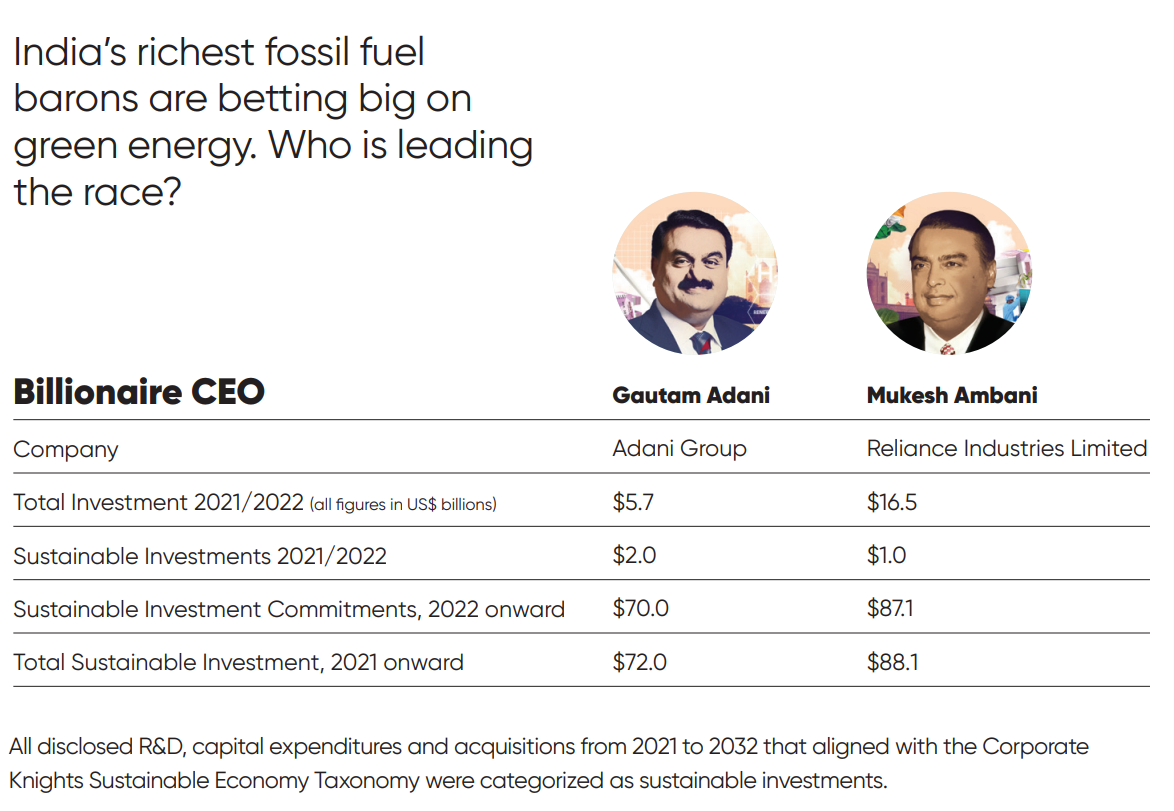

Comparison of green energy investments by Indian fossil fuel leaders Gautam Adani and Mukesh Ambani showing billions invested and committed from 2021 onward

ONGC’s exploration strategy emphasizes both domestic discoveries and international partnerships. The company signed a Joint Operating Agreement with partners for three new exploration blocks and entered strategic partnerships to enhance technical capabilities. Notably, ONGC signed a contract with BP for technical services provision at the Mumbai High field, leveraging global best practices and cutting-edge technologies.

Financial Health and Capital Allocation

Cash Flow Management and Capital Expenditure

ONGC maintained strong cash flow generation despite revenue pressures, with operating cash flows supporting both maintenance capital expenditure and strategic investments. The company’s finance director indicated plans to spend ₹35,000 crores on core exploration and production activities in FY26, with potential increases to ₹45,000 crores by 2028-29 if large discoveries are made and developed.

The company’s balanced approach to capital allocation includes significant investments in renewable energy while maintaining focus on hydrocarbon exploration and production. This dual strategy positions ONGC for both near-term cash generation and long-term energy transition alignment.

Dividend Policy and Shareholder Returns

ONGC maintains a consistent dividend policy, with the board recommending a final dividend of ₹1.25 per equity share for FY25, representing a dividend yield of approximately 5.20%. The company’s dividend payout ratio of 37.9% reflects a balanced approach between rewarding shareholders and retaining capital for growth investments.

Market Reception and Analyst Outlook

Stock Performance and Valuation

ONGC’s stock performance reflects the mixed sentiment surrounding the company’s results and outlook. The stock has declined approximately 31% over the past year, trading at around ₹235 per share as of August 2025. However, the stock trades at attractive valuations with a price-to-earnings ratio of 8.29 and price-to-book ratio of 0.79.

Analyst sentiment remains cautiously optimistic, with 28 analysts providing recommendations including 13 strong buy ratings, 6 buy ratings, 4 hold ratings, 4 sell ratings, and 1 strong sell rating. The average target price of ₹281.38 suggests upside potential of approximately 20% from current levels.

Market Expectations and Forward Guidance

Looking ahead, market expectations for ONGC remain tempered by macro headwinds but supported by the company’s strategic initiatives. The global oil market outlook suggests continued volatility, with Brent crude prices expected to range between $60-80 per barrel through 2025-26, influenced by geopolitical developments, OPEC+ policies, and global demand dynamics.

India’s oil demand is projected to continue growing, with petroleum product consumption expected to reach 252.93 million tonnes in FY26, representing 4.7% growth from FY25 levels. This domestic demand growth provides a supportive backdrop for ONGC’s production and potentially helps offset some global pricing pressures.

Risk Factors and Challenges

Operational and Technical Risks

ONGC faces several operational challenges including the natural decline of mature fields, technical complexities in deepwater exploration, and the need for significant capital investments to maintain production levels. The company’s exploration success rate and ability to develop new discoveries will be critical for long-term production sustainability.

Environmental and regulatory risks also present challenges, particularly as India implements stricter environmental standards and pursues aggressive renewable energy targets. ONGC’s ability to balance traditional hydrocarbon operations with renewable energy investments will be crucial for regulatory compliance and social license to operate.

Financial and Market Risks

Commodity price volatility remains the primary financial risk for ONGC, as demonstrated by the Q1 FY26 results. The company’s revenue and profitability are directly tied to global oil and gas prices, which are influenced by factors largely outside ONGC’s control, including geopolitical events, OPEC+ decisions, and global economic conditions.

Currency fluctuations also present risks, as ONGC’s oil and gas are priced in US dollars while significant costs are incurred in Indian rupees. The company’s international operations through ONGC Videsh add additional currency and country-specific risks.

Conclusion

ONGC’s Q1 FY26 results demonstrate the company’s operational resilience in challenging market conditions while highlighting the ongoing transformation of India’s largest oil and gas company. Despite revenue pressures from lower crude oil prices, the company exceeded profit expectations and maintained strong operational margins through effective cost management and operational optimization.

The company’s strategic pivot toward renewable energy, combined with continued success in exploration and enhanced oil recovery, positions ONGC for the evolving energy landscape. With ₹1 trillion committed to renewable energy investments by 2030 and ongoing success in hydrocarbon exploration, ONGC is balancing immediate cash generation with long-term sustainability.

While near-term challenges from volatile commodity prices and mature field decline persist, ONGC’s strong balance sheet, consistent dividend policy, and strategic investments in both traditional and renewable energy sources provide a foundation for navigating the energy transition. The company’s ability to execute its dual strategy of maximizing returns from existing hydrocarbon assets while building a substantial renewable energy portfolio will be critical for long-term value creation and alignment with India’s energy security and climate objectives.

For investors, ONGC presents a compelling value proposition at current valuations, offering exposure to India’s growing energy demand, dividend income, and participation in the country’s renewable energy transformation. However, investment decisions should carefully consider the inherent volatility of commodity prices and the execution risks associated with the company’s ambitious renewable energy expansion plans.