In the realm of Indian banking, the Credit-Deposit (CD) ratio stands as a pivotal metric, offering insights into the financial health and risk profiles of banks. Recently, the Reserve Bank of India (RBI) has raised concerns regarding the escalating CD ratio, signaling potential overheating within the banking system. This article delves into the intricacies of the CD ratio, its implications, and the underlying factors contributing to its surge.

Indian Banks Struggle with Deposit Crunch: Insights and Implications

Understanding the Current Banking Landscape

In recent news, Indian banks find themselves grappling with a significant deposit crunch in the financial year 2023-24. According to reports from the Reserve Bank of India (RBI), the credit-deposit ratio has soared to unprecedented levels, reaching 80%. This ratio represents the proportion of a bank’s deposits utilized for lending purposes, and its current surge marks the highest recorded since 2015.

Factors Driving the Deposit Dilemma

Shift Towards High-Yield Investments

One prominent factor contributing to this dilemma is the growing inclination of customers towards high-return, equity-linked products. Bhavik Hathi, managing director of consulting firm Alvarez and Marsal, highlighted this trend, emphasizing how it has led to a reduction in the amount of money being deposited in banks.

Ineffectiveness of Deposit Rate Hikes

Despite efforts by banks in the previous financial year to attract deposits by increasing deposit rates, the data suggests that customers remain reluctant. The pace of growth in bank credit has outstripped that of deposits, indicating a mismatch in supply and demand dynamics.

Analyzing the Data

In FY24, while deposits witnessed a growth of 13.5% to ₹204.8 trillion, non-food credit surged by 20.2% to ₹164.1 trillion as of 22nd March. This significant differential growth between deposits and credit illustrates the intensifying pressure on banks to maintain liquidity levels amidst rising credit demands.

Implications for the Banking Sector

The current deposit crunch poses several challenges and implications for the Indian banking sector:

Liquidity Strain

With credit outpacing deposit growth, banks face liquidity strains, potentially hampering their ability to meet lending demands while maintaining regulatory liquidity requirements.

Risk Management Concerns

An imbalance in the credit-deposit ratio raises concerns about banks’ risk management practices, as an overreliance on borrowed funds could heighten vulnerability to market fluctuations and economic downturns.

Impact on Interest Rates

The sustained pressure on deposit mobilization could lead to upward pressure on interest rates, affecting borrowing costs for consumers and businesses alike.

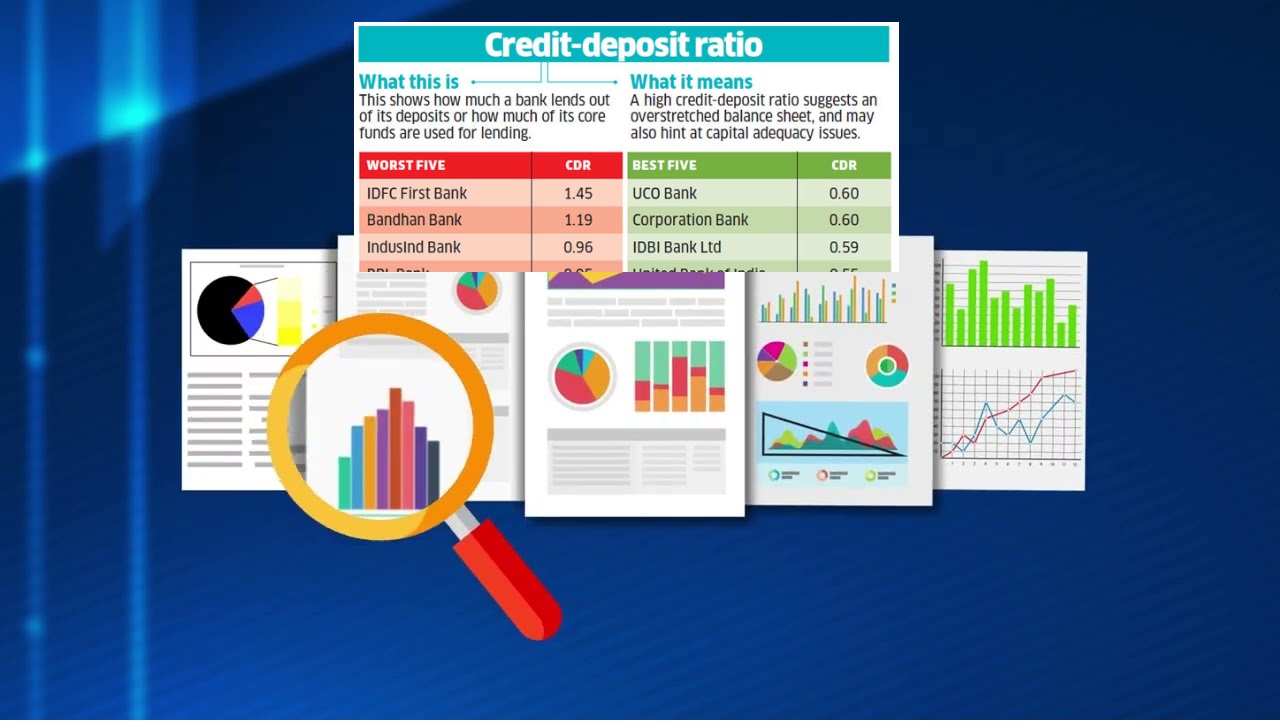

The Importance of CD Ratio

The CD ratio serves as a barometer of liquidity and credit risks for banks. It measures the proportion of money lent out by banks in comparison to the deposits they hold. A higher ratio suggests increased lending activities relative to available deposits, potentially exposing banks to liquidity challenges and credit risks.

Current Scenario: A Red Signal for Bankers

Recent data indicates a concerning trend in India’s banking landscape. Despite a commendable surge in deposits, the pace of deposit growth lags behind the exponential rise in lending activities. This dissonance is exemplified by a notable 13.5% increase in deposits, juxtaposed with a staggering 20.2% surge in lending during a specific fortnight ending March 22, 2024.

Factors Driving the Surge

Several factors contribute to the sluggish growth in deposits and the consequent surge in the CD ratio:

1. Intense Competition

Banks face fierce competition not only from their counterparts but also from alternative investment avenues such as mutual funds, gold, and real estate markets.

2. Changing Saving Patterns

India is undergoing a transition from a nation of savers to one of investors. This shift poses a long-term challenge for banks, especially reliant on Current Account and Savings Account (CASA) deposits.

3. Demand Dynamics

The surge in lending is predominantly driven by the burgeoning demand for personal loans. Conversely, growth in the industrial sector remains subdued.

Regulatory Intervention

To mitigate potential risks associated with the burgeoning CD ratio, the RBI has intervened by increasing the risk weightage for unsecured loans. This measure necessitates higher capital allocation for banks and Non-Banking Financial Companies (NBFCs), aimed at curbing consumer lending and reducing yields.

Future Outlook

While the current economic landscape remains robust, sustained vigilance is imperative to avert any downturns. Banks must recalibrate their credit appraisal mechanisms to shield themselves from non-performing assets (NPAs) in the unsecured lending domain. Furthermore, diversifying into under-penetrated segments such as business loans, MSME loans, and consumer durables loans can unlock new avenues for growth while mitigating risks.

RBI’s Cautionary Move

In an exclusive revelation, it has come to light that the Reserve Bank of India (RBI) is taking proactive measures by advising certain banks to reduce their credit deposit ratio. This strategic maneuver, aimed at fostering financial stability, underscores RBI’s vigilant stance in the current economic landscape.

Insights from Reliable Sources

According to credible sources disclosed to CNBC TV18, the credit deposit ratio has piqued the interest of the RBI. This pivotal ratio, indicative of a bank’s lending capacity in relation to its deposit base, has prompted RBI to urge select banks to maintain their ratio below the 75% threshold.

Impact on Lenders

The rationale behind this directive lies in RBI’s objective to mitigate credit exposure risks among lenders. By lowering the credit to deposit ratio, banks are poised to witness a shift in liquidity dynamics. Specifically, funds may transition from the loan portfolio towards investment avenues, thereby diversifying revenue streams.

Implications on Interest Margins

A noteworthy consequence of reducing the credit deposit ratio is its potential impact on net interest margins (NIMs). Industry experts suggest that such a maneuver could lead to a NIM adjustment of approximately 75 basis points, with a marginal variance of around ±25 basis points.

Sectorial Dynamics

Examining the sectorial landscape reveals a dichotomy among lenders based on their credit deposit ratios. Notably, banks boasting ratios exceeding 75% include idfc Bank, Sury Bank, Equita Small Finance Bank, Utka Small Finance Bank, Axis Bank, and Bundan Bank, among others. Conversely, institutions maintaining ratios below the specified threshold encompass prominent names like Can Bank, State Bank of India, PNB, IDBI Bank, and Bank of India.

Regulatory Prudence

RBI’s discerning approach extends beyond the credit deposit ratio, as evidenced by its recent regulatory interventions. Instances include the curtailment of lending activities in the unsecured segment and the imposition of higher risk weights on assets associated with NBFCs. Such measures underscore RBI’s commitment to maintaining financial stability and safeguarding the banking ecosystem from potential vulnerabilities.

Conclusion

In navigating the intricacies of India’s financial landscape, RBI’s proactive directives serve as a beacon of prudence. By urging banks to recalibrate their credit deposit ratios, RBI endeavors to foster a resilient banking sector capable of withstanding dynamic market forces. As stakeholders navigate these regulatory currents, adherence to RBI’s guidelines becomes paramount, ensuring a robust and sustainable financial ecosystem for all stakeholders.

Frequently Asked Questions

1. What is the Credit-Deposit (CD) ratio?

The CD ratio measures the proportion of money lent out by banks relative to the deposits they hold. It indicates liquidity and credit risks within the banking sector.

2. Why is the surge in the CD ratio concerning?

A surge in the CD ratio implies that banks are extending more loans than they have in deposits, potentially exposing them to liquidity challenges and credit risks.

3. How is regulatory intervention addressing the surge in the CD ratio?

Regulatory bodies like the RBI are increasing the risk weightage for unsecured loans, mandating higher capital allocation for banks and NBFCs. This measure aims to mitigate excessive lending and associated risks.

Conclusion

As India’s banking sector grapples with the implications of an escalating CD ratio, proactive measures are essential to maintain financial stability. Regulatory interventions coupled with prudent lending practices can safeguard banks against potential downturns while fostering sustainable growth in the long term.