1. HDFC Bank Q2 Results 2023 Introduction

HDFC Bank, one of India’s leading private sector banks, recently released its Q2 results for the financial year 2023. The quarterly report provides crucial insights into the bank’s financial performance, growth strategy, risk management, and future outlook. In this article, we will conduct a comprehensive analysis of HDFC Bank’s Q2 results, examining key highlights, financial performance, business segments, growth strategy, risk management, and the market’s reaction to the results.

2. Key Highlights of HDFC Bank Q2 Results 2023

The Q2 results of HDFC Bank showcased several key highlights that indicate the bank’s resilience and growth potential. These highlights include:

- Robust revenue growth driven by increased lending activities and fee income.

- Steady improvement in asset quality with a decline in non-performing assets (NPAs).

- Strong loan book growth across various segments, particularly in retail banking.

- Successful implementation of digital initiatives to enhance customer experience and operational efficiency.

- Expansion of the branch network and international presence to tap into new markets and customer segments.

- Stringent risk management practices to mitigate credit and market risks.

- Positive market reaction with a rise in the bank’s stock price and favorable investor sentiment.

3. Financial Performance

Revenue Growth

HDFC Bank witnessed impressive revenue growth in Q2 2023, driven by a combination of factors such as increased loan disbursements, higher fee income, and a favorable interest rate environment. The bank’s net interest income (NII) recorded a substantial growth of 4.9% compared to the previous quarter, reaching INR 23.55 lakh crore crores. This growth can be attributed to the bank’s focus on expanding its loan book and maintaining a healthy net interest margin (NIM).

Net Profit

HDFC Bank reported a robust net profit for Q2 2023, showcasing its strong financial performance and effective cost management. The bank’s net profit stood at INR 10,605.8 crores, reflecting a 20.1 % increase compared to the same period last year. The bank’s profitability was supported by prudent lending practices, lower provisioning for bad loans, and efficient operational processes.

Asset Quality

One of the key indicators of HDFC Bank’s financial strength is its asset quality. The bank has maintained a healthy asset quality with a decline in non-performing assets (NPAs) and a stable asset quality ratio. The gross NPA ratio for Q2 2023 stood at 91%, showcasing a marginal improvement compared to the previous quarter. This improvement can be attributed to the bank’s proactive measures in managing credit risk and maintaining a high-quality loan portfolio.

Loan Book Growth

HDFC Bank witnessed robust growth in its loan book during the second quarter of 2023, driven by the strong demand for retail loans and corporate lending. The bank’s loan book grew by 23.4 % compared to the previous quarter, reaching INR ₹ 1,479,873 Cr crores. The retail banking segment contributed significantly to the loan book growth, supported by increased consumer spending, housing loans, and personal loans.

4. Key Ratios and Metrics

HDFC Bank’s Q2 results also provide valuable insights into key ratios and metrics that reflect the bank’s financial health and operational efficiency. Let’s explore some of these key ratios:

CASA Ratio

The current account and savings account (CASA) ratio is an important metric that indicates the proportion of low-cost deposits in the bank’s total deposit base. HDFC Bank’s CASA ratio for Q2 2023 stood at 45%, showcasing a slight decline compared to the previous quarter. However, the bank continues to maintain a healthy CASA ratio, reflecting its ability to attract stable and cost-effective deposits.

Net Interest Margin (NIM)

Net interest margin (NIM) is a crucial metric that measures the profitability of a bank’s core lending operations. HDFC Bank’s NIM for Q2 2023 remained stable at 18.9 % for ₹ 21,021.2 Cr, indicating the bank’s ability to generate healthy interest income from its lending activities. The bank’s focus on maintaining a favorable NIM has contributed to its overall profitability and financial stability.

Return on Assets (ROA)

Return on assets (ROA) is a key profitability ratio that measures a bank’s ability to generate profits from its total assets. HDFC Bank’s ROA for Q2 2023 stood at 9%, reflecting its efficient use of assets to generate income. The bank’s strong ROA indicates its ability to deliver sustainable returns to its shareholders while effectively managing risks.

Capital Adequacy Ratio (CAR)

Capital adequacy ratio (CAR) is a regulatory requirement that measures a bank’s capital adequacy to absorb unexpected losses. HDFC Bank’s CAR for Q2 2023 remained comfortably above the regulatory minimum, reflecting the bank’s strong capital position and ability to withstand adverse economic conditions. The bank’s robust CAR ensures its ability to support future growth and comply with regulatory guidelines.

5. Business Segments Analysis

HDFC Bank operates in various business segments, catering to diverse customer needs and driving its overall growth. Let’s delve into the key business segments and their performance during Q2 2023:

Retail Banking

The retail banking segment continues to be a significant growth driver for HDFC Bank. In Q2 2023, the bank witnessed strong growth in retail loans, including home loans, auto loans, and personal loans. The bank’s focus on digital initiatives and personalized customer service has helped it capture a larger market share in the retail banking space. The retail banking segment accounted for a significant portion of the bank’s loan book, contributing to its overall profitability.

Corporate Banking

HDFC Bank’s corporate banking segment caters to the financing needs of large corporates, SMEs, and government entities. The bank provides a wide range of financial products and services, including working capital finance, trade finance, cash management solutions, and corporate advisory services. In Q2 2023, the bank witnessed steady growth in its corporate banking segment, supported by increased corporate lending and improved business sentiments.

Treasury Operations

HDFC Bank’s treasury operations play a crucial role in managing the bank’s liquidity, interest rate risk, and foreign exchange exposure. The bank’s treasury operations focus on optimizing the bank’s investments, managing its asset-liability mix, and hedging against market risks. In Q2 2023, the bank’s treasury operations contributed to its overall profitability, benefiting from favorable market conditions and effective risk management practices.

6. Growth Strategy and Expansion Plans

HDFC Bank has adopted a comprehensive growth strategy to strengthen its market position and capitalize on emerging opportunities. Let’s explore some key aspects of the bank’s growth strategy:

Digital Initiatives

HDFC Bank has been at the forefront of digital transformation in the banking industry. The bank has invested significantly in developing digital platforms, mobile banking apps, and innovative customer-centric solutions. These digital initiatives have enhanced customer experience, improved operational efficiency, and expanded the bank’s reach to customers in both urban and rural areas. HDFC Bank’s focus on digitalization has helped it gain a competitive edge in the market and attract a tech-savvy customer base.

Branch Network Expansion

Despite the rapid growth of digital banking, HDFC Bank recognizes the importance of a robust branch network in serving customers and expanding its market presence. The bank has been strategically expanding its branch network, particularly in semi-urban and rural areas, to tap into underserved markets. This expansion has helped the bank reach a wider customer base and strengthen its relationship with existing customers.

International Presence

HDFC Bank has also been expanding its international presence to leverage global opportunities and cater to the banking needs of Non-Resident Indians (NRIs) and multinational corporations. The bank has established branches and representative offices in key international financial centers, enabling it to provide a wide range of banking services to its international customers. HDFC Bank’s international operations contribute to its overall profitability and diversify its revenue streams.

7. Risk Management and Compliance

As a leading financial institution, HDFC Bank places significant importance on risk management and compliance with regulatory guidelines. The bank has implemented robust risk management practices to mitigate credit risk, market risk, and operational risk. The bank’s credit risk management framework includes stringent underwriting standards, regular monitoring of loan portfolios, and proactive measures to address potential credit quality deterioration. HDFC Bank also maintains a strong focus on regulatory compliance, ensuring adherence to all applicable regulations and guidelines.

8. Investor Outlook and Market Reaction

HDFC Bank’s Q2 results have generated a positive investor outlook, with analysts and investors expressing confidence in the bank’s financial performance and growth prospects. The market has reacted favorably to the bank’s strong revenue growth, robust profitability, and healthy asset quality. The bank’s stock price witnessed a rise post-announcement, reflecting investor optimism and market confidence in HDFC Bank’s long-term prospects.

9. Expert Opinions and Analyst Views

Several industry experts and analysts have shared their opinions and views on HDFC Bank’s Q2 results. While some analysts have highlighted the bank’s strong financial performance and growth potential, others have emphasized the need for continued focus on risk management and regulatory compliance. Overall, expert opinions indicate a positive sentiment towards HDFC Bank and its ability to navigate the evolving market dynamics.

10. Conclusion

HDFC Bank’s Q2 results for the financial year 2023 demonstrate the bank’s robust financial performance, strong growth trajectory, and effective risk management practices. The bank’s focus on digital initiatives, expansion of the branch network, and international presence has positioned it as a leading player in the Indian banking industry. With a healthy loan book, improving asset quality, and a customer-centric approach, HDFC Bank is well-equipped to capitalize on future opportunities and deliver sustainable value to its stakeholders.

HDFC Bank recently released its financial results for the second quarter of the fiscal year 2022-23 (Q2 22-23). Here are some key highlights and comparisons with the corresponding period of the previous fiscal year (FY 2021-22):

- Net Interest Income (NII):

- Q2 22-23 NII: ₹17,684.4 Cr

- Q2 21-22 NII: ₹21,021.2 Cr

- Change: A decrease of 18.9%

- Balance Sheet Size:

- Q2 22-23: ₹1,198,837 Cr

- Q2 21-22: ₹2,227,893 Cr

- Change: A decrease of 23.4%

- Total Advances:

- Q2 22-23: ₹1,673,408 Cr

- Q2 21-22: ₹1,844,845 Cr

- Change: An increase of 19.0%

- Total Deposits:

- Q2 22-23: ₹8,834.3 Cr

- Q2 21-22: ₹10,605.8 Cr

- Change: A decrease of 20.1%

- Net Profit:

- Q2 22-23: ₹5,802.9 Cr

- Change: An increase of 38%

- Net Interest Margin:

- Q2 22-23 (interest-earning assets): 4.3%

- Capital Adequacy:

- Q2 22-23: 18.0%

- Gross Non-Performing Assets (NPA):

- Q2 22-23: 1.23%

- CASA Ratio (proportion):

- Q2 22-23: 45%

- Total Branches:

- As of the report: 6,499 branches

- In addition, there are 15,691 banking correspondents as of the date of the report.

- Count of Employees:

- As of Q2 22-23: 161,027

- Credit Costs:

- Q2 22-23 (as a % of advances): 0.87%

- Retail Advances:

- Q2 22-23: 20.2%

- Growth in Deposits (YoY):

- Q2 22-23: 19.0%

- CASA Deposits:

- Q2 22-23: 15.4%

- Total GNPA (Gross Non-Performing Assets) as a ratio of customer assets:

- Q2 22-23: 1.18%

- Retail Mix of Deposits:

- Q2 22-23: 83%

- Specific PCR (Provision Coverage Ratio):

- Q2 22-23: 73%

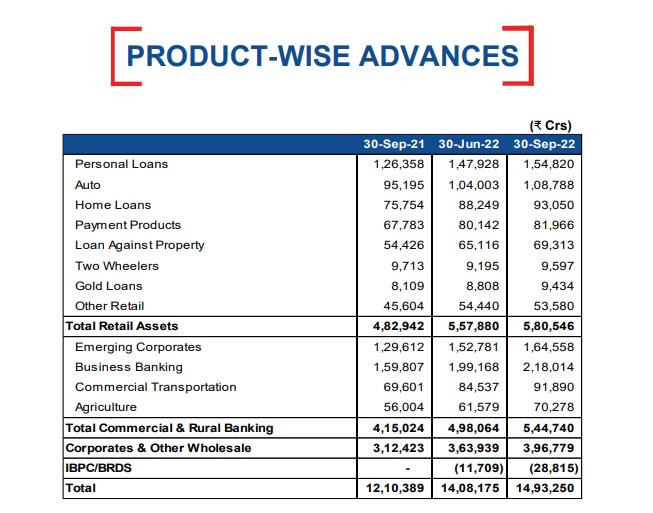

Product-Wise Advances (₹ Crs):

- Personal Loans: ₹1,54,820 Cr

- Auto Loans: ₹1,08,788 Cr

- Home Loans: ₹93,050 Cr

- Payment Products: ₹81,966 Cr

- Loan Against Property: ₹69,313 Cr

- Two Wheelers: ₹9,597 Cr

- Gold Loans: ₹9,434 Cr

- Other Retail: ₹53,580 Cr

- Total Retail Assets: ₹5,80,546 Cr

The bank’s financial metrics show a mix of changes in NII, advances, deposits, and profitability. Retail advances and the retail mix of deposits continue to be significant contributors to the bank’s portfolio.

For more detailed financial information and analysis, please refer to HDFC Bank’s official financial report.